Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Private equity in the 1980s wikipedia , lookup

Investor-state dispute settlement wikipedia , lookup

Special-purpose acquisition company wikipedia , lookup

Private equity in the 2000s wikipedia , lookup

Leveraged buyout wikipedia , lookup

Stock trader wikipedia , lookup

Private equity wikipedia , lookup

International investment agreement wikipedia , lookup

Corporate venture capital wikipedia , lookup

Money market fund wikipedia , lookup

History of investment banking in the United States wikipedia , lookup

Investment banking wikipedia , lookup

Private equity secondary market wikipedia , lookup

Early history of private equity wikipedia , lookup

Environmental, social and corporate governance wikipedia , lookup

Private money investing wikipedia , lookup

Mutual fund wikipedia , lookup

Socially responsible investing wikipedia , lookup

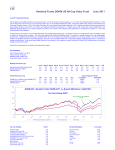

Hereford Funds-IMVA Opportunity Fund November 2014 November 2014 Investment Review November was another disappointment for the Fund. Unfortunately, this trend is not likely to change dramatically in December, given the pressures from tax-loss selling and portfolio managers’ tendency to “window dress” their holdings. The main culprit in November was the collapse in energy sector stocks in the last week of the month. OPEC’s decision to leave production “as is” was obviously not priced into the market, and the resulting drop in WTI prices hurt our energy holdings. All energy stocks have been affected, but many small capitalization energy stocks were decimated. The mix of commodity price uncertainty, tax-loss selling, and end-of-year window dressing has created a downward spiral that feeds upon itself. The small capitalization companies we own generally have financial flexibility next year and can go into survival mode if need be. That attitude does not play well on Wall Street, but it is natural for managers whose net worth is tied to the long-term health of their insider holdings. The energy sector appears toxic right now to most, but the sector’s swings are rarely predicted accurately by the consensus. Looking ahead, I believe that there are good odds this will prove to be a favorable time to maintain our energy exposure. Altisource Portfolio Solutions took another leg down during the quarter. The Company announced it would shut down a portion of its business (about 25% of earnings estimates for next year). This announcement is most likely part of a settlement process with the New York Department of Financial Services. ASPS is still selling at less than 10x earnings projections for next year, and management believes the Company has exciting growth prospects outside of their traditional business with Ocwen. I continue to hold both of these stocks on the assumption that the companies will come to a settlement with the New York DFS and have good capital gains potential after that settlement. Among our other large positions, 3D Systems appears to be doing well, though the stock did not improve much in November. Management was excited about their showing at Euromold last week (the preeminent 3D printing trade show). The Chairman has been buying the stock on the open market, and management seems as confident as ever that their plan to “harvest” this year’s R&D investments over the next five years will be very favorable to equity holders. I believe them, but there are many short sellers who appear not to. We shall see. Healthcare, generally speaking, has been a bright spot for us this year, one of the few. We remain overweight in Luminex based upon our expectation of an eventual sale of the company. Anacor Pharmaceuticals continues to report good news, and its shares are reacting accordingly. As I mentioned above, December is not likely to produce a strong turnaround for the Fund due to a variety of end-of-the-year phenomena. Looking ahead, I am eager to get into 2015 and, hopefully, begin to see a reversal in the trends and issues that have caused our losses this year. Key Information NAV A Shares (30/11/14): $69.16 Total Fund Size: $2.11 mil Strategy Assets: $165.04 mil(a) Fund Launch Date: 31-Jan-14(b) Monthly Performance (%) Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 N/A -0.8 -1.3 -2.1 -1.9 5.3 -6.4 1.7 -8.6 -13.1 -7.7 N/A 4.6 0.8 0.4 2.2 2.3 -1.8 4.1 -1.8 2.7 2.5 N/A 4.6 0.8 0.7 2.4 2.1 -1.4 4.0 -1.4 2.4 2.7 Hereford Funds-IMVA Opportunity Fund S&P 1500 Index(d) (d) S&P 500 Index Period Performance (%) YTD -34.3 13.2 14.0 IMVA Opportunity Portfolio(c) (d) S&P 1500 Index S&P 500 Index(d) 1 yr -30.8 16.0 16.9 2 yr -0.4 23.3 23.4 3 yr 10.6 20.8 20.9 4 yr 9.2 17.3 17.5 5 yr 12.5 16.2 16.0 10 yr 10.0 8.3 8.1 YTD -30.8 17.1 18.1 Since Inception 31/03/99 Cumulative Annualised 150.9 6.1 135.2 5.6 115.5 5.0 IMVA Opportunity Portfolio (c) vs. S&P 1500(d) & S&P 500(d) Ten Years Ending 30/11/14 450 Start of Hereford Funds-IMVA Opportunity Fund 31-Jan-14 350 400 300 350 250 300 200 250 150 200 100 150 50 100 500 IMVA Opportunity Portfolio Fund's TopTen Holdings 3D Systems Corp. Ocwen Financial Corp. Luminex Corp. Anacor Pharmaceuticals, Inc. Advanced Energy Industries Intrepid Potash, Inc. Altisource Ptfl. Solns. Reg. Shs. Freeport-McMoran KVH Industries Stone Energy % NAV 8.71 6.89 6.81 5.63 5.22 5.02 4.90 4.64 4.59 4.56 S&P 1500 S&P 500 Fund's GICS Sectoral Breakdown Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Utilities [Cash] % of assets 1.6 -21.1 16.5 18.9 4.3 25.4 9.7 --2.5 Total 100.0 Investment Objective The investment objective of the Hereford Funds-IMVA Opportunity Fund is to provide capital appreciation over a multi-year investment horizon by investing primarily in a diversified portfolio of publicly traded equity securities of US-based companies, which hold unique opportunities in the opinion of the Investment Manager. Potential investments comprise small, mid, and large capitalization companies; growth and value companies; and special situations, including non US-based companies, which are listed on a US exchange. The strategy is highly concentrated and appropriate only for risk-tolerant, long-term investors who can accept the potential for materially greater volatility than the broad market indices. The indicative benchmarks are the S&P 1500 and the S&P 500 Indices. Risk Profile(e) Fund Codes Bloomberg: ISIN: Reuters: Sedol: Valoren: WKN: HFIMVOALX* LU1022309220 N/A BJ625V8 23467814 A1XCJ3 Since Inception (31/03/99) - 30/09/14 Volatility Sharpe Ratio Information Ratio Tracking Error Beta Alpha Reference Strategy 27.99 0.25 (listed below benchmark) (listed below benchmark) (listed below benchmark) (listed below benchmark) S&P 500 17.24 0.14 0.26 17.49 1.30 4.87 S&P 1500 17.43 0.17 0.22 17.29 1.30 4.11 * Share Class A Fund Details Investors Dealing day Dividends Investment Manager Management Company Custodian Legal Advisers Auditor Open to Non-U.S. investors only Daily None: income accumulated within the fund Investment Management of Virginia, LLC, 919 E. Main Street, Suite 1600, Richmond, VA 23219, USA BSI Fund Management S.A., 44F, rue de la Vallée, L-2661 Luxembourg BSI Europe S.A., 122, rue Adolphe Fischer, L-1521 Luxembourg Elvinger, Hoss & Prussen, 2 Place Winston Churchill, L-1340 Luxembourg Deloitte Audit S.à.r.l., 560, rue de Neudorf, L-2220 Luxembourg Annual Management Charge Share Class A(f) 1.25% Minimum Investment Share Class A $100,000 initial; $10,000 subsequent Order Transmission / Information Original Applications To: UBS Fund Services (Luxembourg) S.A. attn: Transfer Agent 33A, avenue J.F. Kennedy L-1855 Luxembourg Subsequent Applications Only Via Facsimile: UBS Fund Services (Luxembourg) S.A. attn: Transfer Agent Fax : (+352) 441010 6417 Tel: (+352) 441010 6404 e-mail: [email protected] (a) This figure refers to the approximate total assets invested in the reference strategy as of 30/11/14. The figure includes $2.11 million in assets (Hereford Funds-IMVA Opportunity Fund), $148.70 million in assets managed directly by Investment Management of Virginia, LLC ("IMVA" or "the Investment Manager"), and $14.23 million in assets managed by other firms based upon models provided by the Investment Manager. The $148.70 million managed directly by IMVA comprise those accounts in the Opportunity Portfolio composite (see www.imva.net), as well as “Special” Opportunity Portfolio accounts, which are excluded from the composite for reasons/variances, including but not limited to these: they have different weightings; client restrictions have been imposed; they are wrap accounts; they do not own all Opportunity Portfolio positions, or they own additional positions. Model assets have been excluded from the definition of the firm for GIPS purposes. (b) The Hereford Funds-IMVA Opportunity Fund was funded on 31/1/14. The first trades were executed on 3/2/14. (c) Data and graph depict IMVA Opportunity Portfolio composite returns through January of 2014 and Hereford Funds-IMVA Opportunity Fund Class A thereafter (net basis). Historical net performance of the IMVA Opportunity Portfolio composite (the Reference Strategy) reflects modeled fees and expenses typical of Hereford Funds-IMVA Opportunity Fund Class A (1.25% fee + 0.25% expense). Fund follows substantially the same parameters as the Reference Strategy, although the Fund has a 10% constraint for individual positions and a 40% limit for the top five names (IMVA's Opportunity Portfolio has no such constraints). Performance presentation is incomplete without accompanying footnotes as shown at www.imva.net. (d) Total return including dividends. (e) Source: eVestment Analytics – All numbers are presented gross of fees and expenses. (f) Share Class A is tax transparent in Germany and has been granted Reporting Status by HMRC as of 31 January 2014. This document is for information purposes and internal use only. It is neither an advice nor a recommendation to enter into any investment. Investment suitability must be determined individually for each investor, and the financial instruments described above may not be suitable for all investors. This information does not provide any accounting, legal, regulatory or tax advice. Please consult your own professional advisers in order to evaluate and judge the matters referred to herein. An investment should be made only on the basis of the prospectus, the annual and any subsequent semi-annual-reports of HEREFORD FUNDS (the "Fund"), a société d'investissement à capital variable, established in Luxembourg and registered under Part I of Luxembourg law of 20 December, approved by the Commission de Surveillance du Secteur Financier (CSSF). These can be obtained from [the Fund, 26, avenue de la Liberté, L-1930 Luxembourg or from BSI Fund Management S.A., 44F, rue de la Vallée, L-2661 Luxembourg and any distributor or intermediary appointed by the Fund]. No warranty is given, in whole or in part, regarding performance of the Fund. There is no guarantee that its investment objectives will be achieved. Potential investors shall be aware that the value of investments can fall as well as rise and that they may not get back the full amount invested. Past performance is no guide to future performance. The information provided in this document may be subject to change without any warning or prior notice and should be read in conjunction with the most recent publication of the prospectus of the Fund. Whilst great care is taken to ensure that information contained herein is accurate, no responsibility can be accepted for any errors, mistakes or omission or for future returns. This document is intended for the use of the addressee or recipient only and may not be reproduced, redistributed, passed on or published, in whole or in part, for any purpose, without the prior written consent of HEREFORD FUNDS. Neither the CSSF nor any other regulator has approved this document.