Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Internal rate of return wikipedia , lookup

Investment management wikipedia , lookup

Trading room wikipedia , lookup

Financialization wikipedia , lookup

Credit rationing wikipedia , lookup

Financial economics wikipedia , lookup

Algorithmic trading wikipedia , lookup

Land banking wikipedia , lookup

Stock trader wikipedia , lookup

Investment fund wikipedia , lookup

Global saving glut wikipedia , lookup

Investment banking wikipedia , lookup

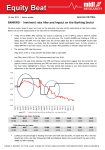

19 June 2017 | Visit note Panasonic Manufacturing Malaysia Berhad Striving to maintain its profit margins Maintain NEUTRAL Unchanged Target Price (TP): RM32.40 INVESTMENT HIGHLIGHTS RETURN STATS • Underperforming home appliance segment • Fixed dividend payout despite higher cash balance Price (16 June 2017) RM35.20 • Some products will see a stronger performance in FY17 Target Price RM32.40 • Maintain NEUTRAL with a unchanged TP of RM32.40 Underperforming home appliance segment. To recall, the home appliance segment’s FY17 earnings were impacted by lower PBT margin as operating costs increased at a faster pace which resulted in FY17 performance coming in lower than expectation. The poor result of the segment is due the underperformance of its products such as: (i) rice cookers segment which is struggling to reach breakeven level due to the higher cost of production as a result from the transfer of manufacturing activities from Thailand to Malaysia and; (ii) vacuum cleaner and iron segment recorded a lower sales as its main market i.e. the middle east sales (accounted for 80% of total sales) which has not fully recovered in FY16. Dividend payout will remain fixed despite higher cash balance. As at 4QFY17, the cash and cash equivalents stands at RM602.43m (+0.1%yoy) which is a significant 60% of total assets. In addition, all of its subsidiaries are in net cash positions, hence intercompany lending is unnecessary at this juncture. Approximately 80% or RM500m of the cash is placed in fixed deposit instruments at local financial institutions (FIs) yielding average interest income of 3.5% annually. The reason for such high cash hoarding is due to: (i) the expansion project where RM100m is needed in the next two years and; (ii) as part of the group strategy in hedging activities as well negotiating better interest rates from FIs. Therefore, despite the cash pile build-up, the company’s dividend payout ratio will still be fixed at 60% of PAT. Future outlook. Despite the lacklustre FY17 results, we opine that there will be an improvement in FY18 financial performance as rice cookers segment is targeted to breakeven from losses incured in FY17 while vacuum cleaner could see some recovery as of 1QFY18. In contrast, the sales from Fans segment might slow down this year due to lower project sales from the government for the installation of fans. In addition, given that 60% of sales is to the overseas market, a stronger Ringgit this year will reduce the FOREX gain albeit lowering the cost of purchasing raw materials. Nonetheless, recent rise in prices of aluminium and copper reduce the benefit of having a stronger Ringgit. Hence, we remain neutral on the company’s future prospects. Expected Share Price Return -7.9% Expected Dividend Yield +4.0% Expected Total Return -3.9% STOCK INFO KLCI 1791.31 Bursa / Bloomberg 3719/PMM MK Board / Sector Main/Consumer Syariah Compliant Yes Issued shares (mil) 60.75 Market cap. (RM’m) 2138.25 Price over NA 2.60x 52-wk price Range RM29-RM39.9 Beta (against KLCI) 0.41 3-mth Avg Daily Vol 0.01m 3-mth Avg Daily Value RM0.54m Major Shareholders (%) Panasonic Mgmt M’sia 47.45 Aberdeen Asset Mgmt 10.20 EPF 7.15 MIDF RESEARCH is a unit of MIDF AMANAH INVESTMENT BANK Kindly refer to the last page of this publication for important disclosures MIDF EQUITY BEAT Monday, 19 June 2017 Maintain NEUTRAL with an unchanged TP of RM32.40. Maintain NEUTRAL with unchanged Target Price of RM32.40. Post-meeting, we are making no changes to our earnings forecast and TP, which is based on pegging forward PER of 13.5x against FY18 EPS pf 240sen per share. The assigned PER multiple is the group’s three year average historical PER. INVESTMENT STATISTICS FYE 31st March (RM'm) 2015 2016 2017 2018F 2019F 931 1,086.7 1,123.0 1,179.5 1,217.9 Profit before tax 129.8 185.2 158.1 186.6 199.2 Net Profit 99.5 146.9 127.1 145.6 157.4 - 137.4 134.0 145.6 157.4 Pre-tax Profit margin (%) 13.9 17 14.1 15.8 16.4 Net Profit margin (%) 10.7 12.6 11.9 12.3 12.9 Normalised EPS (sen) 164 226 221 240 259 EPS Growth (%) 23.3 47.6 -2.5 8.6 8.1 PER (x) 22.2 16.1 16.5 15.2 14.0 Net Dividend (sen) 142 139 123.3 143.8 155.4 Dividend yield (%) 3.9 3.8 3.4 4.0 4.3 Revenue Normalised Net Profit Source: Company, Forecasts by MIDFR DAILY PRICE CHART Nabil Zainoodin, CA [email protected] 03-2772 1663 2 MIDF EQUITY BEAT Monday, 19 June 2017 MIDF RESEARCH is part of MIDF Amanah Investment Bank Berhad (23878 - X). (Bank Pelaburan) (A Participating Organisation of Bursa Malaysia Securities Berhad) DISCLOSURES AND DISCLAIMER This report has been prepared by MIDF AMANAH INVESTMENT BANK BERHAD (23878-X). It is for distribution only under such circumstances as may be permitted by applicable law. Readers should be fully aware that this report is for information purposes only. The opinions contained in this report are based on information obtained or derived from sources that we believe are reliable. MIDF AMANAH INVESTMENT BANK BERHAD makes no representation or warranty, expressed or implied, as to the accuracy, completeness or reliability of the information contained therein and it should not be relied upon as such. This report is not, and should not be construed as, an offer to buy or sell any securities or other financial instruments. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially different results. All opinions and estimates are subject to change without notice. The research analysts will initiate, update and cease coverage solely at the discretion of MIDF AMANAH INVESTMENT BANK BERHAD. The directors, employees and representatives of MIDF AMANAH INVESTMENT BANK BERHAD may have interest in any of the securities mentioned and may benefit from the information herein. Members of the MIDF Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein This document may not be reproduced, distributed or published in any form or for any purpose. MIDF AMANAH INVESTMENT BANK : GUIDE TO RECOMMENDATIONS STOCK RECOMMENDATIONS BUY TRADING BUY NEUTRAL SELL TRADING SELL Total return is expected to be >15% over the next 12 months. Stock price is expected to rise by >15% within 3-months after a Trading Buy rating has been assigned due to positive newsflow. Total return is expected to be between -15% and +15% over the next 12 months. Total return is expected to be <15% over the next 12 months. Stock price is expected to fall by >15% within 3-months after a Trading Sell rating has been assigned due to negative newsflow. SECTOR RECOMMENDATIONS POSITIVE The sector is expected to outperform the overall market over the next 12 months. NEUTRAL The sector is to perform in line with the overall market over the next 12 months. NEGATIVE The sector is expected to underperform the overall market over the next 12 months. 3