Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Private equity wikipedia , lookup

Special-purpose acquisition company wikipedia , lookup

International investment agreement wikipedia , lookup

Stock trader wikipedia , lookup

Early history of private equity wikipedia , lookup

Money market fund wikipedia , lookup

History of investment banking in the United States wikipedia , lookup

Private equity secondary market wikipedia , lookup

Investment banking wikipedia , lookup

Environmental, social and corporate governance wikipedia , lookup

Private money investing wikipedia , lookup

Socially responsible investing wikipedia , lookup

Mutual fund wikipedia , lookup

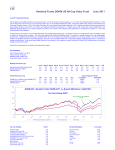

Hereford Funds – Firth Asian Value Fund September 2014 September 2014 Investment Review In September 2014 the total return of the Fund after deducting all fees and expenses was -3.0%. By comparison the total return of the MSCI AC Asia ex Japan Small Cap index was -3.6% and the total return of the MSCI AC Asia ex Japan index was -5.9%. Key Information Hereford Funds – Firth Asian Value Fund NAV A Shares (30/9/2014): Total Fund Size: Strategy Assets: Fund Launch Date: $113.73 $75 million $175 million (a) 31/05/11 Performance (%) (net of fees and expenses) Jan Feb Mar HFFAVF1 2 Small Cap Asia ex Japan3 HFFAVF1 Small Cap2 Asia ex Japan3 HFFAVF1 Small Cap2 Asia ex Japan HFFAVF 3 1 Small Cap2 Asia ex Japan HFFAVF1 3 Apr May Jun Jul Aug Sep Oct Nov Dec 2011 - -1.2 -2.4 -2.3 0.6 2.8 1.1 -8.5 -11.4 -9.9 -12.6 -16.3 -13.2 6.4 10.1 12.0 -5.9 -8.7 -8.3 0.8 -1.2 0.6 -19.7 -26.1 -20.2 - - - - Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2012 6.1 10.0 10.8 12.1 9.0 6.0 -1.4 -3.8 -3.1 -0.9 -1.7 0.0 -5.9 -7.8 -9.6 0.9 1.8 3.0 3.9 0.0 2.6 4.2 2.2 -0.5 3.1 6.7 7.0 2.2 -1.1 -0.3 -0.2 2.9 2.8 3.3 3.5 3.1 29.6 22.4 22.4 Jan Feb Mar* Apr May Jun Jul Aug Sep Oct Nov Dec 2013 3.8 3.5 1.7 1.9 1.6 -0.1 2.0 0.5 -2.2 1.0 2.6 1.8 0.4 1.2 -1.3 -4.8 -8.7 -5.7 0.9 0.8 1.8 -1.9 -2.5 -1.5 2.9 6.2 5.4 1.0 2.7 4.4 0.7 -0.9 0.2 0.7 0.2 -1.1 8.7 6.9 3.1 Jan# Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2014 -2.1 -1.7 -4.7 0.9 3.8 3.5 -0.9 1.2 1.0 1.1 0.2 0.7 1.3 3.0 4.0 0.0 1.8 2.3 0.9 1.4 3.8 2.3 1.7 0.7 -3.0 -3.6 -5.9 0.5 7.7 4.7 Since Launch 2 Small Cap Asia ex Japan 3 Source: Bloomberg, Firth Investment Management 1. Hereford Funds – Firth Asian Value Fund 2. MSCI AC Asia ex Japan Small Cap USD Net Index * Month end date used is March 28, 2013. # Month end date used is January 29, 2014. 13.7 4.2 5.4 3. MSCI AC Asia ex Japan USD Net Index (large and mid cap) The performance of the fund was resilient in a rapidly falling market as our defensive characteristics would imply. Combined with the more “stock specific” gains made in August the fund has outperformed both benchmarks in the third quarter of the year. Unusually, small capitalisation stocks outperformed large cap this month. Amongst the small cap country indices Indonesia was the worst performing market, down 9%, followed by Hong Kong which fell 7%, and currencies were weak across the region. China’s famous “Special Administrative Region” has consumed most of the headlines recently and for investors it has been the likely impact of democracy demonstrations and continued political difficulties on its economy which is of most interest. While stocks listed in Hong Kong are a large proportion of the portfolio, Hong Kong domestic demand, as measured by sales, probably accounts only for about 7% of our fund. The Hong Kong economy is enduring lower retail sales mostly as a result of the slowing China economy and property cooling measures in Hong Kong itself. The city has similar structural issues to many developed economies: overheated asset prices (and unaffordable private housing); a perception of growing inequality and capture of most of the growth in wealth by “elites”. Furthermore, the currency peg ensures that the equity market in Hong Kong typically suffers at times of a strengthening US Dollar and tightening US monetary policy. During the month we completed the sale of three stocks. Of these Esprit began as a large company, a good example of our “fallen angel” investments and the holding that has stimulated the most questions from observers of our portfolio. Our timing of the initial buying in the summer of 2011 was not ideal, but the purchases made subsequently to get to a full weighting were made at good prices. We began to sell in 2013 and, so far, the exit appears to have been satisfactorily timed. Our original investment case was based on new management taking measures to stabilise the business and reinvigorate a tired brand. While this did begin to happen and they appeared to be taking sensible decisions with the business model, it remains a fashion company with most of its sales in Germany. They have failed to make progress in Asia/China, having originally identified the region as an alternative source of growth to Europe. They now expect sales to contract further in 2015. This investment has been a reminder that fashion is by its nature a competitive, difficult and unpredictable business. Turning around clothing brands is possible (there are many recent examples) but much harder if underlying macro-economic growth is anemic. Finally, Esprit is not a small business and has a substantial following among analysts, so it is more likely to be efficiently priced except at extremes of sentiment such as in late 2011. We will send a more detailed report on the third quarter to all clients later in October. Source: Bloomberg, Firth Investment Management *Both MSCI benchmark indices (Bloomberg: MSLUAAJN and NDUECAXJ) are net total return indices in USD. MSCI calculates net total return by reinvesting any dividend income after deducting withholding taxes. Country breakdown Hong Kong/China Indonesia India Korea Malaysia Philippines Singapore Taiwan Thailand Others Cash % of assets 36 0 5 13 2 2 13 10 1 9 9 Sectoral breakdown Consumer Discretionary Consumer Staples Financials Health Care Industrials Information Technology Materials Others Cash % of assets 40 12 2 0 11 16 2 9 9 Investment Objective Hereford Funds - Firth Asian Value Fund is to generate long term capital growth from a portfolio of listed company securities in Asia (ex-Japan). The Compartment will follow a value-based investing approach and will have a bias towards smaller capitalisation stocks. The Compartment will directly invest primarily in shares of companies located in, incorporated in, headquartered in, listed on exchanges in or with significant operations in or significant income derived from Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, the PRC, Singapore, Taiwan and Thailand. The Compartment may also directly invest in smaller or developing economies in Asia such as Bangladesh, Cambodia, Laos, Pakistan, Sri Lanka or Vietnam. The Compartment will not invest in China A Shares when investing in the PRC. The Compartment will directly invest actively in a diversified portfolio of listed equity securities. The Compartment will generally only invest in securities admitted to official listing on a recognized stock exchange, or dealt in on another regulated market. Although the Compartment intends to invest in a portfolio of not less than 40 stocks and not more than 100 stocks, it is not restricted in or subject to any material concentration or diversification restrictions, and may hold a more limited number of investment positions. The Compartment will typically be near fully invested but may hold liquid assets on an ancillary basis. Under normal market conditions, investment in liquid assets and debt instruments of any kind will not exceed 15% of the Compartment's net assets. In exceptional market circumstances and on a temporary basis only, this limit may be increased to 100% with due regard to the principle of risk spreading. The Investment Manager intends to meet the Fund’s objective primarily through stock selection and country allocation. Typically stocks will be bought and held. This is not a trading strategy and it is not intended to attempt to time general market movements. While portfolio returns will be measured against the Benchmark Index, portfolio management will not be constrained by reference to the index. Fund Codes Bloomberg ISIN Reuters Sedol Valoren WKN HFIRASA LX * LU0618975774 NA B64KS81 12853411 A1H9V4 * Share Class A Fund Details Dealing Day Dividends Investment Manager Promoter Fund Administrator Custodian Legal Advisers Auditor Daily None - income accumulated within the fund Firth Investment Management Pte. Ltd. 180 Cecil Street, #13-03 Bangkok Bank Building, Singapore VP Bank (Luxembourg) S.A., 26 Avenue de la Liberté, L-1930 Luxembourg VPB Finance S.A., 26 Avenue de la Liberté, L-1930 Luxembourg VP Bank (Luxembourg) S.A., 26 Avenue de la Liberté, L-1930 Luxembourg Elvinger, Hoss & Prussen, 2 Place Winston Churchill, L-1340 Luxembourg Deloitte, 560 Rue de Neudorf, L-2220 Luxembourg Annual Management Charge Share Class A Share Class D (b) 1.5% 2.0% Annual Management Charge Performance fee: High water mark?: Hurdle rate: 10% Yes MSCI AC Asia ex Japan Small Cap USD Net Minimum Investment Share Class A (b) Share Class D $100,000 initial / $10,000 subsequent $10,000 initial / $1,000 subsequent Order Transmission Information Original Applications To: VPB Finance S.A. attn. Fund Operations / TA-HFF P.O. Box 923 L-2019 Luxembourg or, for transmissions via courier service, 26, avenue de la Liberté, L-1930 Luxembourg Subsequent Applications Only Via Facsimile: VPB Finance S.A. attn. Fund Operations / TA-HFF Fax: (+352) 404 770 283 Tel: (+352) 404 770 260 e-mail: [email protected] (a) This refers to the total assets to which the Investment Adviser applies the reference strategy. (b) Share Class A: these shares have UK reporting since launch and are registered with the BaFin for public distribution in Germany from 17/10/12. Germany – Paying Agent as defined by German Regulation: Marcard, Stein & Co – Ballindamm 36, 20095 Hamburg; Phone: +49/40.32.099.556, Fax: +49/40.32.099.206 (c) Share Class D: these shares have not yet been launched. This document is for information purposes and internal use only. It is neither an advice nor a recommendation to enter into any investment. Investment suitability must be determined individually for each investor, and the financial instruments described above may not be suitable for all investors. This information does not provide any accounting, legal, regulatory or tax advice. Please consult your own professional advisers in order to evaluate and judge the matters referred to herein. An investment should be made only on the basis of the prospectus, the annual and any subsequent semi-annual-reports of HEREFORD FUNDS (the "Fund"), a société d'investissement à capital variable, established in Luxembourg and registered under Part I of Luxembourg law of 20 December, approved by the Commission de Surveillance du Secteur Financier (CSSF). These can be obtained from [the Fund, 26, avenue de la Liberté, L-1930 Luxembourg or from VPB Finance S.A., 26, avenue de la Liberté, L-1930 Luxembourg and any distributor or intermediary appointed by the Fund]. No warranty is given, in whole or in part, regarding performance of the Fund. There is no guarantee that its investment objectives will be achieved. Potential investors shall be aware that the value of investments can fall as well as rise and that they may not get back the full amount invested. Past performance is no guide to future performance. The information provided in this document may be subject to change without any warning or prior notice and should be read in conjunction with the most recent publication of the prospectus of the Fund. Whilst great care is taken to ensure that information contained herein is accurate, no responsibility can be accepted for any errors, mistakes or omission or for future returns. This document is intended for the use of the addressee or recipient only and may not be reproduced, redistributed, passed on or published, in whole or in part, for any purpose, without the prior written consent of HEREFORD FUNDS. Neither the CSSF nor any other regulator has approved this document.