Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Currency War of 2009–11 wikipedia , lookup

Reserve currency wikipedia , lookup

Competition (companies) wikipedia , lookup

International monetary systems wikipedia , lookup

Currency war wikipedia , lookup

Bretton Woods system wikipedia , lookup

Foreign exchange market wikipedia , lookup

Fixed exchange-rate system wikipedia , lookup

Purchasing power parity wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Balance of Payments

and

Exchange Rates

Ch1/BP&ER

1

Introduction:

Open vs closed economy

Three kinds of openness:

• Free trade in goods and services

Restrictions:

,

etc.

• Free movements of capital (financial)

Restrictions:

• Free movements of factors: plants,

labor

Restrictions:

Ch1/BP&ER

2

Various Measurements of openness

• EXPORTS/GDP or IMPORTS/GDP

• (EXPORTS + IMPORTS)/GDP

• TRADABLES/GDP

Tradables are goods that compete with foreign goods

on either domestic or foreign markets e.g.

This last ratio (high for the US) reflects the fact that

if a country is competitive it does not need to

import much.

Ch1/BP&ER

3

X/GDP (in 2000)

US

UK

Belgium

Japan

China

11%

27%

84%

10%

23%

Some determinants of openness:

Geographical: how far a country is from specific

markets

Size: the extent of the range and choice of goods

produced domestically

Ch1/BP&ER

4

Differences between international

trade and international macro

International trade

•

•

•

•

Based on micro

Full employment of

factors

Total C = total Y each

year

Value of imports =

values of exports

Relative prices (T/T)

Ch1/BP&ER

International macro

•

•

•

•

Based on macro

Economy can be

_____ PPF

S

and b

at country level

Trade can be -balanced

Price ________

5

A

The Balance of Payments

• The national income accounts

revisited (econ 301)

• The balance of payments accounts

Ch1/BP&ER

6

National Income Accounts - Review

In principle

However

Because

Value of Production = Value of income

GNP ≠ National Income

•

GNP does not subtract economic depreciation

•

Income includes gifts from abroad

•

National income is based on prices producers receive

while GNP is based on prices purchasers pay

difference = indirect taxes

Ch1/BP&ER

7

GNP - Deprec + Net unilateral transfer - indirect taxes

= Natl Y

with: net unilateral transfer = gifts to us - gifts from us

Ch1/BP&ER

8

Gross domestic product vs

gross national product

• GDP is the value added ________ - ignoring who owns the

factors of production - i.e. income generated by activity

within the border

• GNP is the value added by __________ owned factors of

production - i.e. total income received by domestic

residents

GDP

less income on assets owned by foreigners in the country

plus income on assets owned by US residents abroad

equal GNP

If a country invests heavily abroad:

GNP

If a country uses a lot of foreign labor: GDP

Ch1/BP&ER

GDP

GNP

9

GNP = GDP + Net receipts of factor income from ROW

GDP

US Res

+

Non US Res

in country

Includes income

generated by foreign

owned wealth and

foreign labor.

Res stands for residents

Ch1/BP&ER

GNP

US Res

Income

US Res

only

generated

abroad

US owned factor income

so includes income on

US wealth invested

abroad and

income to US workers

abroad

10

The Balance of Payments

• Definition: Record of the transactions

between residents and

residents

a year.

• Double entry accounting:

– Credit entry: any transaction that gives rise to a

payments

(by the foreigners) and that is a

payment

+

– Debit entry: any transaction that gives rise to a

payments

(to the foreigners) and that is a

payment

Ch1/BP&ER

11

Characteristics of B/P

• 2 types of international transactions:

– Exports (sales) and imports (purchases) of goods & services

accounts CA

– Sales and purchases of assets

accounts FA

– Balance = sales - purchases

Note:

A section called the capital account was created recently to complement the shift from GNP to GDP

•

book keeping

–

–

–

2 sides to all transactions

one

entry (+) and one

entry (-)

so Sum of credits (+) + Sum of debits (-) = 0

i.e. BP = 0

Ch1/BP&ER

12

I Current Account

• Affects income ( as

)

• Measures direction and size of

CA > 0 S

- country is a

CA < 0 D

- country is a

So CA = ∆ in a country’s foreign assets (or debt)

C + I + G is absorption or

demand for

goods (produced at home or imported)

Y - (C + I + G) =

i.e. if a country consumes more than it produces, it

must

from abroad as it runs a CA

Ch1/BP&ER

13

Intertemporal interpretation

• Borrowers must repay their debt in the future

• A country with a CA deficit imports present

consumption and exports future consumption

Other interpretations

• Chronic CA deficits result in large foreign debt

and high interest payments on the debt which

further erode the CA

• Chronic surpluses could have inflationary effects

Ch1/BP&ER

14

National saving and the CA

By definition

Sn Y - C - G

• Closed economy

as Y = C + I + G

in equil: Sn =

• Open economy

as Y = C + I + G + CA

in equil: Sn =

Open economy saves by building capital stock (I)

by investing abroad (if CA >0)

(A country can invest more than its saving by borrowing from abroad thus

running a CA deficit)

Ch1/BP&ER

15

Private and government saving: The twin deficit

• Sp

and Sg

by definition

and national saving Sn Sp + Sg = Y - C - G

• In equilibrium

Sn = I + CA

Sp + Sg = I + CA

Sp = I + CA - Sg = I + (EX - IM) + (G - T)

So private saving can

1. Finance private investment

2. Allow the country to invest abroad

3. Finance the budget deficit

Ch1/BP&ER

16

Current Accounts Breakdown

• Exports and imports of goods and services

– Exports are

– Imports are

entries ( )

entries ( )

• Services are sometimes called

» Insurance - banking services - shipping

• Investment income received ( ) and paid ( )

– Interest etc.

– Net = investment income received less inv. inc. paid

• Unilateral Transfers (net)

– One sided transaction: Gifts to us ( ) and gifts from us ( )

– Net = Gifts to us - gifts from us

Ch1/BP&ER

17

Various balances

• Exports of goods less imports of goods:

the balance on goods

so-called the

trade balance

• Exports of services less imports of services:

the balance on services

• Exports of goods and services less imports of

goods and services:

the balance of

( or net exports)

• Balance of trade + net investment income +

net unilateral transfer:

the balance on

or

Ch1/BP&ER

18

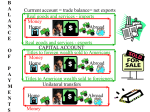

II Capital and Financial Account

A Capital Account

•

capital transfers (migrant labor financial

transfers and debt forgiveness)

•

transactions in non-produced and nonfinancial assets (transfer of ownership in

natural resources, intellectual property

rights, franchises and leases)

Total amount is not very large.

Ch1/BP&ER

19

B Financial account

• Correspond to

in stock of assets - so they

are

(thus consistent with current accts).

• Some are

and other are

accounts.

• Some are

term and some are

term type of

assets.

• Some are

and some are government

transactions;

– the government transactions can be broken down

further into Central Bank and non Central Bank .

Ch1/BP&ER

20

Financial Account summary

• US owned assets abroad (net changes)

– Increase is a US

– So a financial

– So a

(-)

of foreign stocks/bonds

• Foreign owned assets in the US (net changes)

– Increase is a

of US assets to foreigners

– So a financial

– So a

(+)

Ch1/BP&ER

21

Financial Account detail

• US owned assets abroad (increase is (-))

– US official reserves assets (net)

• Gold - SDR - foreign currencies

– US government assets

– US private assets

• Direct investment (FDI)

• Foreign securities

• Credit balance in foreign bank and non-bank

institutions

Ch1/BP&ER

22

• Foreign owned assets in the US (increase is

(+))

– Foreign official assets in the US (net)

• US Treasury Securities - bank balances

– Other foreign assets in the US (as above)

• FDI

• US Treasury securities (gov’t bonds)

• Other stocks and bonds

• US currency

• Bank balances in US bank and non-bank

institutions

Ch1/BP&ER

23

• Net capital account transactions

+ {net increase in foreign owned assets in the US

less abs. value1 of net increase in US owned

assets abroad}

= Capital and financial account balance FA

1.

Because they are entered as a minus in BoP

• Statistical discrepancy

{ - [Current account balance + Capital and financial account

balance]}

If there was no mistakes or underreporting, the sum of the 2

balances should be equal to zero.

Ch1/BP&ER

24

Overall Interpretation

• CA balance measures

in country’s net

foreign assets (e.g. a surplus - CA > 0 corresponds to lending to ROW)

• So this will be reflected in the FA balance

where purchases of foreign assets will be

________ than sales of foreign assets.

• In sum a positive CA balance will be

matched by a

FA balance of same

absolute value

Ch1/BP&ER

25

Examples of US balance of payments

entries

Alitalia buys a Boeing 747 and pays with a

check from Banco di Lavoro

– Credit:

of Boeing (3)

accounts

– Debit:

in US owned private asset

abroad or in US claims reported by US

banks (54)

accounts

Ch1/BP&ER

26

The US government sends food as relief

to famine stricken Mali

– Credit:

– Debit:

Ch1/BP&ER

of food (3)

accounts

(gift from us) (36)

accounts

27

A French citizen buys shares of

Microsoft and pays by drawing his

account at the Key Bank

– Credit:

in foreign owned private

assets in the US (64)

accounts

– Debit:

in US liabilities reported

by US banks (69)

accounts

Ch1/BP&ER

28

B

Exchange Rates

Ch1/BP&ER

29

Various Exchange Rates

Nominal exchange rate - E

• Definition: the price of the foreign currency in

terms of the domestic currency so it is quoted as

________ of units of domestic currency

in ____ unit of foreign currency

• It fluctuates overtime

– Appreciation of the domestic currency:

units

are needed to buy 1 unit of the foreign currency

– Depreciation of the domestic currency:

units

are needed to buy 1 unit of the foreign currency

Ch1/BP&ER

30

Examples of ER fluctuation

•

•

•

•

•

January 1999

$1.17/€

September 2000

$0.85/ €

May 2002

$0.91/ €

May 2003

$1.14/ €

September 2007

$1.41/€

The euro depreciated by some 27%

against the dollar in its first 18 months and

appreciated by some 25% from 2002 to

2003. The euro has continued to appreciate

steadily since.

Ch1/BP&ER

31

Law of One Price

2 countries - each produces one good

– Switzerland produces calculator - price: 100SF

– US

produces book

- price: $25

– Nominal exchange rate: E = $.50/SF

• So price of Swiss calculator in $ is 100 * .50 = $50

– The real exchange rate RER is:

Pr iceofSwissgoodin $ 50

RER

2

Pr iceofUSgood ($)

25

PSinSF * E $ /SF 100SF * .50$ /SF

RER

2

PUSin$

$25

Ch1/BP&ER

32

Real Exchange Rate

• The real exchange rate is a relative price of 2

goods (calculator and book) indicating that

Swiss calculator =

US books

i.e.

US books can be exchanged for (or buy)

Swiss calculator

• With more than one good, the meaning will be

slightly different. We will need to use the

aggregate price of a basket of goods (the price

level or CPI) in each country and the RER will

become the relative price of the 2 baskets.

Ch1/BP&ER

33

RER cont.

• We now have

PS * E $ /SF

EP *

RER =

or

PUS

P

• The meaning is similar: the RER indicates how

many (units of a) US basket(s) can be

exchanged for 1 foreign basket (P* is the

foreign price level).

• If either E or P or P* change, we will have a

real appreciation or a real depreciation.

Ch1/BP&ER

34

Real appreciation and depreciation

• When the RER drops, we have a real

i.e. the US needs to give up

US baskets to

acquire

foreign basket. This is a real

depreciation from the point of view of the other

country.

*

• Since

EP

=

P

A real appreciation can be caused by:

a nominal

(E drops)

or/and an

in the domestic price level (P incr)

or/and a

in the foreign price level (P* drops)

Ch1/BP&ER

35

Effect of the real appreciation on trade

• Swiss goods become

expensive for Americans

(less than 2 US baskets to buy one Swiss basket)

– So demand for Swiss good

- US Imports

• US goods become

expensive for the Swiss

(one Swiss basket buy fewer US baskets)

– So demand for US goods

- US Exports

• So the US the balance of trade (exports less

imports)

but the Swiss balance of

trade

because they experience a real

depreciation).

Ch1/BP&ER

36

In Sum:

Effect of the real appreciation on trade:

• imports are ________ and exports ___________

• the balance of trade will __________

• this results in a _______ in the country’s

international competitiveness

A real depreciation has the opposite effect as

more domestic baskets are needed to buy one

foreign basket and the balance of trade improves:

• this results in an _______ in the country’s

Ch1/BP&ER

international competitiveness

37

Illustration

• Between 1959 and 1985, inflation in

Switzerland or Germany has not been as high as

in France, so France (the French Franc)

experienced a real appreciation with respect to

these 2 currencies. However in the long run

(over the years), the nominal exchange rate

(F/DM or F/SF) also depreciated to account for

these relative price changes.

Ch1/BP&ER

38

Multilateral or trade weighted ER

Up to now we only considered bilateral exchange

rate i.e. the relative price of 2 currencies.

However one specific currency may appreciate

with respect to another currency and depreciate

with respect to a third currency: in one instance

there will be a deterioration in its international

competitiveness and in the other an

improvement.

We need to develop a way to get the whole picture.

Ch1/BP&ER

39

Construction of a trade weighted ER

• The are constructed by the IMF - but there is

more than one way to do it.

• The basic approach is

– To transform each bilateral ER into an

(indeed you can’t add ER as they are expressed in

different units)

– Decide on a

year set as 100 and calculate an

index series over time for each bilateral ER.

– Use a

scheme to aggregate the various

indices - usually the importance of trade with a

specific country as a ratio of total trade.

Ch1/BP&ER

40

Calculation of a trade weighted index

for the $ using pound and euro

Yr 0 index wght

Yr 1

.70

100

.30

.75

107

.30

€/$ 1.15

100

.70

1.10

95

.70

£/$

index wght

TW

index

The dollar appreciates w/ respect to the pound and depreciates w/

respect to the euro, but overall the dollar depreciates. Note that w/

T-W exchange rates, an increase is an appreciation.

Ch1/BP&ER

41

Real multilateral or trade weighted ER

Evidently, it is also possible to calculate a real

multilateral or trade weighted exchange rate.

It suffices to calculate the original bilateral indices

with the real bilateral exchange rates.

Ch1/BP&ER

42