Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Research Report · Industry Research · Nonferrous

Nonferrous Industry Monthly · May 2010

Base metals: NEUTRAL (Reiterate)

Gold: OUTPERFORM (Reiterate)

Industrial Metals: Confined by Uncertainties

Gold: A Continual Upbeat Trend

15 Jun 10

Investment Highlights

CSI Research Department

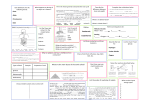

Performance Relative to

Indices

Nonferrous

中标300

有色金属

H股指数

S&P/

H-share

Metals

CITIC300

Index

50

40

30

20

10

0

-10

090601 090806 091021 091228 100312 100521

Source: CSI

Prices of industrial metals declined, while gold outperformed. (i) Events such as

the sovereign debt crisis in Europe and Greek strike escalated market risk aversion,

with the USD index rising 5.6% MoM in May 10; (ii) gold demand due to risk aversion

was highlighted, with the international spot price for gold hitting a new high of

US$1,249.62/ounce and posting an average MoM growth of 4.9%; (iii) in terms of

industrial metals, apart from tin, the LME price index of other metals fell 10%-plus, and

domestic metal prices also dropped successively, albeit at a slower pace; and (iv)

prices for some minor metals rose and those for some dropped worldwide, and

domestic prices for rare earths began to pull back.

Benefiting from share prices for minor metals and gold counters, the nonferrous

sector dropped at a slower pace than the broad market. Expectations regarding the

tightening of China’s real estate policies, as well as concerns over uncertainties on rate

hikes and RMB appreciation resulted in a generally weakening A-share market, as

exemplified by the SSE Composite Index’ 7.54% decline (to 2,656 points). All in all, the

nonferrous sector dropped at a slower pace than the broad market in May 10. During

the month, (i) the top 10 in gainers were rare earth, minor metals and gold counters,

with only Zhongfu Industry among the major metals; and (ii) counters of major metals

such as copper, aluminium and lead-zinc were among the top 10 losers.

Industrial metals: Strong demand and sufficient supply. Jan-Apr 10 statistics

showed that: (i) various metals posted meaningful growth in cumulative output; (ii) as

for semi-finished products, copper and aluminium output hit monthly new highs

repeatedly; and (iii) although downstream automobile, electrical utility and household

appliance industries retained a stable growth in output, aluminium, copper and zinc

inventories at the Shanghai Futures Exchange (SHFE) increased. Inventories for the

respective products rose 66.28%, 65.45% and 71.75% compared with those logged at

end-09 due to continuous increases in metal output and large scale imports in previous

months.

Gold: A continual upbeat trend. (i) The sovereign debt crisis in European countries

(such as Greece and Portugal) continued to overhang the market, leading to high

uncertainties in the international monetary system and rising risk aversion; (ii) the

expansionary monetary policy of countries following the economic crisis continued to

lend support to inflation expectations, both of which resulted in a continual upbeat

trend of gold price.

Reiterate NEUTRAL rating for base metals and OUTPERFORM rating for gold. (i)

Despite China’s thriving demand for metal and continually rising metal consumption in

Western countries, soaring inventories and rising output constrained price hikes; and

(ii) the market is still affected by uncertainties from domestic housing policies and the

sovereign debt crisis in European countries. Therefore, we reiterate our NEUTRAL

rating for base metals. Gold prices keep hovering high with an optimistic medium to

long-term outlook. In particular, given rising safe haven demand and expectations for

asset injections of domestic listed companies, we reiterate our OUTPERFORM rating

for gold.

Risks associated with investing in the sector. (i) Launch of additional policies in the

Mainland to curb real estate prices; (ii) deterioration of sovereign debt crisis in Europe;

(iii) increased inflation expectations; (iv) exit of easy monetary policy by various

countries; and (v) further credit crunch.

Peers’ Comparison – China Nonferrous Sector

PER (x)

Price

Company

(HK$)

Hong Kong - average

PEG (x)

P/B (x)

Yield (%)

RoE (%)

09

10E

11E

09-11E

10E

10E

10E

24

16

12

0.8

1.9

3.9

14

CHALCO (02600.HK)

6.27

NA

16

12

NA

1.3

1.3

8

Zijin Mining (02899.HK)

5.72

21

14

12

0.7

3.3

2.9

28

17

Jiangxi Copper (00358.HK)

14.88

17

10

8

0.4

1.5

1.9

Hunan Non-ferrous Metals (02626.HK)

2.65

NA

32

18

NA

1.8

0.6

6

Zhaojin Mining (01818.HK)

16.72

28

21

19

1.4

4.0

2.1

21

13

CMOC (03993.HK)

4.59

40

12

10

0.4

1.5

3.2

Xinxin Mining (03833.HK)

3.70

31

15

11

0.5

1.3

2.4

9

Lingbao Gold (03330.HK)

2.77

8

7

7

1.3

0.8

16.5

14

Source: Respective companies, Bloomberg, CSI

*Based on closing as of 14 Jun 2010

Please read the disclaimer at the end of the report

Disclaimer

This research report is for information purposes only and should not be construed as an offer to sell or the solicitation of an offer to buy or sell any

securities in any jurisdiction. The securities referred to in this report may not be eligible for sale in some jurisdictions. The information contained in this

report has been compiled by CITIC Securities Brokerage (HK) Limited (formerly known as CITIC Capital Securities Limited) ("CSBHK") from sources that

it believes to be reliable and (subject to the next paragraph) the opinions, analysis, forecasts, projections and expectations contained in this report are

based on such information and are expressions of belief only and no representation, warranty or guarantee is made or given by CSBHK or any other

person as to its accuracy or completeness. All opinions and estimates expressed in this report are (unless otherwise indicated) entirely those of CSBHK

as of the date of this report only and are subject to change without notice. Neither CSBHK nor its parent and affiliates accept any liability whatsoever for

any direct or consequential loss arising from any use of material contained in this report or otherwise arising in connection therewith.

The research analyst(s) primarily responsible for the preparation of this research report confirms that (i) all of the views expressed in this research

report accurately reflect his or her personal views about any and all of the subject securities or issuers; and (ii) that no part of his or her recommendation

was, is or will be, directly or indirectly, related to the specific recommendations or views he or she expressed in this report.

Any investment referred to herein may involve significant risk, may be illiquid and may not be suitable for all investor. The value of or income from any

investment referred to herein may fluctuate and be affected by changes in exchange rate. Past performance is not indicative of futures results. This report

does not take into account the investment objectives, financial situation or particular needs of any particular person. Investors are expected to make their

own investment decision without relying on this publication. Before acting on any advice or recommendation in this report, clients are recommended to

consider seeking professional advice.

CSBHK, its parent and/or affiliates and their respective officers, directors and employees, including persons involved in the preparation or issuance of

this report, may from time to time (1) have a consulting, investment banking or broking relationship with any company referred to in this report; and (2)

have provided significant advice or investment services to the companies referred to in this report. One or more directors, officers and/or employees of

CSBHK, its parent and/or its affiliates may be a director of the issuers of the securities mentioned in this report.

If this report is being distributed by a financial institution other than CSBHK or its affiliates, that financial institution is solely responsible for distribution.

Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This

report does not constitute investment advice by CSBHK to the clients of the distributing financial institution, and neither CSBHK, its parent, its affiliates,

and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this

report or its content.

This research report is strictly confidential to the recipient and is not intended for persons in places where the distribution or publication of this report

is not permitted under the applicable laws or regulations of such places.

This research report may not be reproduced, distributed or published by any person for any purpose without the prior consent of CSBHK. All rights

are reserved.

Regulatory disclosures

No part of the analyst compensation was, is or will be directly related to the specific recommendations or views contained in this research report.

CSBHK and each of its group companies that carry on a business in Hong Kong in investment banking, proprietary trading or agency broking in

relation to securities have no disclosable financial interests in the stocks reviewed in this research report.

CSBHK and each of its group companies that carry on a business in Hong Kong in investment banking, proprietary trading or agency broking in

relation to securities have not received compensation from or mandated for investment banking services in the past 12 months to listed

corporations whose stocks are being reviewed by CSBHK in this research report

CSBHK and each its group companies that carry on a business in Hong Kong in investment banking, proprietary trading or agency broking in

relation to securities do not have an individual employed by or associated with them serving as an officer of the listed corporation whose stocks

are being reviewed by CSBHK in this research report

CSBHK and each of its group companies that carry on a business in Hong Kong in investment banking, proprietary trading or agency broking in

relation to securities are not market makers in the stocks reviewed by CSBHK in this research report.

Further information on the securities discussed in this report is available upon request.

Investment rating system

Performance of stock or sector relative to MSCI-China Index over next 6 months after research publications

Rating

Stock rating

Sector rating

地址:

Remark

Buy

Relative performance over MSCI-China Index >20%

Overweight

Relative performance over MSCI-China Index 5% ~ 20%

Hold

Relative performance over MSCI-China Index -10% ~ 5%

Sell

Relative performance over MSCI-China Index > -10%

NR

Not rated

Outperform

Relative performance over MSCI-China Index >10%

Neutral

Relative performance over MSCI-China Index -10% ~10%

Underperform

Relative performance over MSCI-China Index > -10%

香港中环

Address:

26/F CITIC Tower

添美道 1 号

1 Tim Mei Avenue

中信大厦 26 楼

Central, Hong Kong

电话:

(852) 2237 9250

Tel:

传真:

(852) 2104 6580

Fax:

(852) 2104 6580

电邮:

[email protected]

Email:

[email protected]

网址:

http://www.citics.com.hk

Web:

http://www.citics.com.hk

(852) 2237 9250