Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Pensions crisis wikipedia , lookup

Fear of floating wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Exchange rate wikipedia , lookup

Fractional-reserve banking wikipedia , lookup

Monetary policy wikipedia , lookup

Real bills doctrine wikipedia , lookup

Modern Monetary Theory wikipedia , lookup

Helicopter money wikipedia , lookup

Quantitative easing wikipedia , lookup

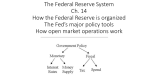

Frank & Bernanke 4th edition, 2009 Ch. 12: Stabilizing the Economy: The Role of the Federal Reserve 1 2 Origins of the Federal Reserve System Resistance to establishment of a central bank Fear of centralized power Distrust of moneyed interests No lender of last resort Nationwide bank panics on a regular basis Panic of 1907 so severe that the public was convinced a central bank was needed Federal Reserve Act of 1913 Elaborate system of checks and balances Decentralized 3 Board of Governors of the Federal Reserve System Seven members headquartered in Washington, D.C. Appointed by the president and confirmed by the Senate 14-year non-renewable term Required to come from different districts Chairman is chosen from the governors and serves four-year term 4 Federal Open Market Committee (FOMC) Meets eight times a year Consists of seven members of the Board of Governors, the president of the Federal Reserve Bank of New York and the presidents of four other Federal Reserve banks Chairman of the Board of Governors is also chair of FOMC Issues directives to the trading desk at the Federal Reserve Bank of New York 5 Federal Reserve System Source: Federal Reserve Bulletin. 6 The Federal Reserve System The Fed’s Role in Stabilizing Financial Markets: Banking Panics Suppose: Depositors lose confidence in their bank. They attempt to withdraw their funds. Bank may not have enough reserves (fractional) to meet the depositors demand. The bank fails and further erodes depositor confidence which triggers additional failures. 7 The Federal Reserve System The Fed’s Role in Stabilizing Financial Markets: Banking Panics The Fed to the rescue: Instill confidence Discount lending Open Market Operations 8 The Great Depression The Fed did not prevent the Great Depression. Both currency held by the public and reservedeposit ratio rose, reducing money supply. The Fed increased the reserves but not enough. Lack of enough reserves forced bank bankruptcies. One-third of U.S. banks closed 9 Policy Tools in the Federal Reserve System 10 MONETARY STATISTICS DURING GREAT DEPRESSION Currency Res/Dep Reserves M1 Dec-29 3.85 0.075 3.15 45.9 Dec-30 3.79 0.082 3.31 44.1 Dec-31 4.59 0.095 3.11 37.3 Dec-32 4.82 0.109 3.18 34.0 Dec-33 4.85 0.133 3.45 30.8 Why did money supply fell during the Great Depression even though the Fed kept reserves up? What would M value be in 1932 if reserve ratio did not change? 11 Fed’s Control of Nominal Interest Rate By buying or selling bonds, the Fed increases or decreases the RESERVES in the system. If the Fed buys securities, reserves increase, then banks can easily find required funds => lower federal funds rate of interest. 12 The Federal Funds Rate, 1970-2004 13 http://research.stlouisfed.org/publications/mt/page9.pdf 14 Fed Funds Rate vs. Prime If Fed can affect the federal funds rate, why should we care? We might be interested in the interest rates on CDs, mortgage rates, credit card interest rates. Usually, interest rates all go hand in hand. When the Fed increases the federal funds rate, banks increase their prime rates, too. 15 Real and Nominal Interest Rates If the amount of savings and investments in an economy determine the real interest rate, and real interest rate is more important for the decisions that will affect the wealth of the society, why should we care what the Fed does? Because in the short run, prices are constant, so inflation does not increase: any change in nominal interest rates is reflected in the real interest rate. 16 Real and Nominal Interest Rates Remember the Fisher Effect: i=r+p If the expected inflation hasn’t changed (short-run: prices constant) but the Fed has increased i, then r is also increased. In the long run p adjusts and it is the savings and investments that determine the real rate of interest. 17 Federal Funds Rate and the Economy PAE responds to C, I, G, NX changes. Only real interest rate impacts INVESTMENTS and SAVINGS Real interest up => S up => C down Real interest up => I down Real interest up => USD appreciates => Imports cheaper; exports more expensive => NX down r up => C, I, NX down => PAE shifts down 18 Real Interest Rates and Aggregate Demand Y = C + I + G + NX C = 400 + 0.8(Y-T) - 200r I = 300 - 600r G = 250; T = 200; NX = 10 Explain in words how this economy operates. 19 Solving for the Unknowns If the real interest rate is 3%, find the values of C, I, and Y for the previous economy and draw the Keynesian cross to show the Y. If the Fed has increased the real interest rate to 5%, find the values of C, I, and Y and show the new AD curve on your graph. 20 Fighting Recession The Fed reduced the fed funds rate 11 times in 2001-2002 from a high of 6.5%. On Nov. 6, 2002, it was 1.75% and the Fed decided to lower it further. What was the effect of Fed’s lowering of interest rates on AD? What was the Fed policy between 20072010 (look at slide #13)? 21 Fighting Recession Fed lowers r => I, C, NX increase => PAE shifts up => For every $1 increase (shift) in PAE, Y increases by the value of the multiplier => Equilibrium Y is no longer at recession value => Y-Y*=0. 22 The Fed Fights A Recession Expenditure line (r = 1%) Planned aggregate expenditure PAE • Multiplier = 5 • Output gap = 200 • Fed wants to increase PAE by 200/5 = 40 • C = 1,010 – 1,000r • 1% change in r will change C by 10 • Reduce r to 0.01 Y = PAE Expenditure line (r = 5%) F A reduction in r shifts the expenditure line upward E Recessionary gap 4,800 5,000 Y* Output Y 23 Fighting Inflation From the middle of 1999 to the middle of 2000, the Fed raised the fed funds rate from 4.75% to 6.50%. At the beginning of 1977 the fed funds rate was 4.5%. By the end of 1978 it was 10%. A year later it was 13.75%. By April 1980, it reached 17.6%. What happens to PAE? 24 Raising Interest Rates Real GDP growth of nearly 6% in late 2003 and 4.4% in 2004 and a falling unemployment rate to 5.6% in June 2004 indicated the possible emergence of an expansionary gap. From June 2004 to June 2005 the Fed Funds Rate rose from 1.0% to 3.25%. 25 The Fed Fights Inflation Planned aggregate expenditure PAE Y = PAE Expenditure line (r = 5%) E G Expenditure line (r = 9%) An increase in r shifts the expenditure line downward Expansionary gap 4,600 4,800 Y* Output Y 26 Inflation and the Stock Market Inflation is watched very closely by the Fed. Any sign of inflation makes Fed increase interest rates. Higher real interest rates slow down the economy and lower future profits. Higher real interest rates lower the price of bonds and shift the demand away from stocks to bonds, lowering stock prices. If there is no inflation but there is an asset bubble, should the Fed increase the interest rate? 27 Policy Reaction Function If there is a pattern of policies adopted under the same economic circumstances, then we have a policy reaction function. For example, if there is a correlation between low unemployment rates and lax immigration policies and high unemployment rates and strict immigration policies, this can be shown with an equation. 28 A Monetary Policy Reaction Function for the Fed Rate of inflation, p Real interest rate set by Fed, r 0.00 (= 0%) 0.02 (= 2%) 0.01 0.03 0.02 0.04 0.03 0.05 0.04 0.06 29 An Example of a Fed Policy Reaction Function Real interest rate set by Fed, r 0.06 Fed’s monetary policy rule 0.05 0.04 If the Fed sets the target inflation as 2%, what interest rate will it set? 0.03 0.02 0.01 0.02 0.03 Inflation p 0.04 30 What is Demand for Money? Demand for Money (Liquidity Preference) The amount of wealth an individual chooses to hold in the form of money. The portfolio allocation decision is made by comparing return relative to risk. Risk can be reduced by diversifying the portfolio. Most people choose to hold some wealth as money. 31 The Demand for Money Money (currency + checking deposits) is one of the assets a person, a household, a business holds. The benefit of money is its acceptability in paying debts (liquidity). The cost of money is the opportunity cost of losing a return on other assets one could hold. 32 The Demand for Money If the opportunity cost of holding money increases, less money will be held in portfolio. The higher the nominal interest rate, the lower is the demand for money. The more the income, the more will be the amount kept in money form: the higher will be the demand for money. The higher the price level, the higher will be the demand for money. 33 Nominal interest rate i The Money Demand Curve Shifts in MD • Changes in Y & P • MD will increase if Y or P increase • Technological changes • Foreign demand MD’ MD Money M 34 Shifts in Money Demand Businesses hold more than half of the total money stock. Changes in real income (real GDP). Changes in price level. Technological change and sophisticated financial markets have reduced the demand for money in the U.S. Changes in foreign holdings of USD. Between 1960 and 2004 M1 as a percent of GDP fell from 28% to 12%. Psychological changes. Seasonal changes. 35 Foreign Holdings of USD More than $300 billion in currency circulating outside the U.S. Foreign citizens will hold dollars to avoid the impact of high inflation. Foreign citizens will hold dollars to protect against political instability. 36 Money Supply By engaging in open market operations, the Fed increases (buy bonds) or decreases (sell bonds) the amount of money in the system. If the demand for money remains the same, the action of the Fed affects the federal funds rate. S up; D same => P down 37 Nominal interest rate Equilibrium in the Market for Money Money Explain how and why the market reaches equilibrium. 38 Equilibrium in the Market for Money If at the existing interest rate, supply exceeds demand, that means people would like to hold less money than there is. How do people adjust their portfolios? They buy other assets with the excess money in their checking accounts. The price of bonds (non-money assets) goes up: interest rate goes down. 39 The Fed Wants to Raise i Fed sells bonds The money supply falls Creates a shortage of money People sell non-money assets Non-money asset prices fall and the interest rate increases 40 http://www.federalreserve. gov/newsevents/press/mo netary/20110315a.htm 41 Interest Rates and Money Supply The Fed cannot set the interest rate and the money supply independently. The Fed controls the money supply by controlling bank reserves. Bank reserves influence the federal funds rate. Therefore, the federal funds rate reflects the impact of open market operations. 42 The Fed and Money Supply Second Way : Discount Window Lending The lending of reserves by the Federal Reserve to commercial banks Discount Rate (primary credit rate): The interest rate that the Fed charges commercial banks to borrow reserves. 43 The Fed and Money Supply Third Way: Changing Reserve Requirements Set by the Fed The minimum values of the ratio of bank deposits that commercial banks are allowed to maintain Lowering the reserve ratio increases the ability of banks to make loans and therefore expand the money supply. Increasing the reserve ratio reduces the ability of banks to make loans and create money. 44 The New Tools http://www.federalreserve.gov/monetarypolicy/default.htm 45