Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

International status and usage of the euro wikipedia , lookup

Reserve currency wikipedia , lookup

Currency War of 2009–11 wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Foreign exchange market wikipedia , lookup

Purchasing power parity wikipedia , lookup

Currency war wikipedia , lookup

Bretton Woods system wikipedia , lookup

International monetary systems wikipedia , lookup

Fixed exchange-rate system wikipedia , lookup

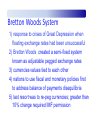

Exchange-Rate Systems and Currency Crises Chapter 15 Copyright © 2009 South-Western, a division of Cengage Learning. All rights reserved. Exchange Rate Systems 1) fixed rate a) also known as pegged exchange rate b) anchored to the value of one other currency or a group of currencies 2) floating rate a) determined by market forces b) float independently or with a group of other currencies IMF Principles 1) Member nations must avoid manipulating exchange rates in order to impact balance of payments 2) Members should intervene to counteract disruptive short term exchange rate movements 3) Members should take into account the impact of intervention policies on other members Impossible Trinity It is not possible for a country to maintain all three of the following: 1) free capital flows 2) a fixed exchange rate 3) independent monetary authority Impossible Trinity (continued) A country can choose any two of the three: Impossible Trinity (examples) 1) U.S. allows free flow of capital & maintains monetary authority but does not have a fixed exchange rate 2) Hong Kong has a fixed exchange rate & allows free flow of capital but does not have independent monetary authority 3) In the past, China had a fixed and maintained monetary authority but did not allow the free flow of capital Fixed Exchange Rates Fixed exchange rates are the norm for developing economies. By tying their currencies to a key currency – that of a larger, more developed nation they promote 1) a means of international settlement 2) stabile prices for imports/exports 3) limits on inflationary pressure Fixed Exchange Rates (continued) Under a fixed exchange rate system governments maintain o par value for their currencies o an official exchange rate determined by comparing par values o an exchange rate stabilization fund to buy and sell foreign currencies in order to preserve the official exchange rate Preventing Depreciation If the demand for the euro increased, the value of the euro would rise and the value of the dollar would fall. In order to maintain the fixed exchange rate, the U.S. would use its reserve of euros to buy dollars. P Market for Euros S1 S2 $1.70 $1.50 D2 D1 Q Preventing Appreciation If the supply of the euro increased, the value of the euro would fall and the value of the dollar would rise. In order to maintain the fixed exchange rate, the U.S. would use dollars to buy euros. P Market for Euros S1 S2 $1.50 $1.25 D2 D1 Q Devaluation & Revaluation Devaluation o legal reduction of a currency’s par value o market impact termed depreciation o counters a balance of payment deficit by making exports less expensive Revaluation o legal increase of a currency’s par value o market impact termed appreciation o counters a balance of payment surplus by making imports less expensive Bretton Woods System 1) response to crises of Great Depression when floating exchange rates had been unsuccessful 2) Bretton Woods created a semi-fixed system known as adjustable pegged exchange rates 3) currencies values tied to each other 4) nations to use fiscal and monetary policies first to address balance of payments disequilibria 5) last resort was to re-peg currencies; greater than 10% change required IMF permission Floating Exchange Rates o also known as flexible exchange rates o equilibrium exchange rate determined by demand for and supply of home currency o changes in exchange rate correct payments imbalance by changing the effective cost of imports and exports o will not fluctuate erratically unless there is significant instability in financial markets Depreciation & Exports If real income in the U.S. increased, then demand for imports and demand for the euro would increase. The value of the euro would rise and the value of the dollar would fall. P Market for Euros S1 $1.70 $1.50 D2 D1 Q Depreciation & Exports (cont.) Since more dollars are required to purchase a euro, the dollar has depreciated. 1) As a result, U.S. goods will become less expensive to European citizens leading to more exports from the U.S. 2) European goods will become more expensive to U.S. citizens leading to fewer imports to the U.S. $150 U.S. auto part before $150 = 100 € after $150 = 88.2 € (150÷170) 100€ French wine before 100 € = $150 after 100 € = $170 Appreciation & Imports If real income in the U.S. declined, then demand for imports and demand for the euro would also decrease. The value of the euro would fall and the value of the dollar would rise. P Market for Euros S1 $1.50 $1.25 D1 D2 Q Appreciation & Imports (cont.) Since fewer dollars are required to purchase a euro, the dollar has appreciated. 1) As a result, U.S. goods will become more expensive to European citizens leading to fewer exports from the U.S. 2) European goods will become less expensive to U.S. citizens leading to more imports to the U.S. $150 U.S. auto part before $150 = 100 € after $150 = 120 € (150/125) 100€ French wine before 100 € = $150 after 100 € = $125 Arguments on Floating Exchange Advantages Fixed • simplicity and clarity of exchange-rate target • automatic rule for monetary policy • controls inflation Floating • continuous adjustment in balance of payments • simplified institutional arrangements Disadvantages • loss of independent monetary policy • vulnerable to speculative attacks • conducive to inflation • disorderly markets can disrupt trade and investment patterns • independent monetary • reckless financial and fiscal policies policies by government Managed Floating System o intervention to stabilize rates in short run with market forces determining rates in long run o informal guidelines established by IMF o clean float – free-market forces of supply and demand determine equilibrium o dirty float – central banks intervene to promote depreciation of their currencies o leaning against the wind – intervention to reduce fluctuations in the short run only Managed Float Example permanent change in demand temporary increase in demand to D1 – exchange rate allowed central bank sells francs while demand is D1 until return to D0 to increase Monetary Policy if demand for pounds decreases if demand for pounds increases Fed increase MS lowering rates Fed decrease MS raising rates increasing demand for dollars decreasing demand for dollars Crawling Peg o uses small, frequent changes in par value to correct balance of payments disequilibria o primarily nations with high inflation o differs from adjustable pegged rates under which par values change infrequently o crawling peg is appropriate for developing nations but not for industrialized nations whose currencies provide international liquidity Currency Crises o also known as speculative attacks o weak currency depreciates significantly as a result of selling o can substantially reduce economic growth o usually ended by official devaluation or adoption of a floating rate o extreme cases => currency crashes Causes of Currency Crises 1) 2) 3) 4) 5) 6) 7) 8) speculation deficit financed by inflation weak financial systems recent deregulation of financial markets weak economic performance political factors external factors such as interest rates choice of exchange rate system Capital Controls 1) also known as exchange controls 2) barriers to foreign savers investing in domestic assets 3) pro: government can control its balance of payments position and possibly prevent speculative attacks 4) con: weakened confidence in the government may actually cause an increase in capital outflows Question of Foreign Exchange Tax 1) volatile capital movements lead to severe repercussions across economies 2) a tax on inflows or outflows would reduce the number of transaction based on short term speculation 3) such a tax would still allow market forces to influence investment and exchange rates over the long term 4) how much volatility is acceptable Currency Board 1) monetary authority that issues notes convertible into a foreign anchor currency at a fixed rate 2) anchor currency chosen for stability and acceptability 3) government finance only by taxation and borrowing – not by printing money 4) implies elimination of discretionary monetary policy by domestic government Case Study – Hong Kong 1) Hong Kong adopted a currency board system in 1983 2) U.S.$ = 7.75 to 7.85 HK$ 3) reversed lack of confidence in the economy despite anticipation of control shifting from the U.K. to China 4) contributed to significant economic growth in Hong Kong; per capita real GDP of $37,300 ranks 13th of 216 nations Case Study – Argentina 1) adopted currency board in 1991 to limit inflation 2) 1 U.S.$ = 1 Argentine Peso 3) issues: dollar appreciated, U.S. interest rates rose, domestic commodity prices fell, and Brazil’s currency depreciated 4) U.S. fiscal & monetary policy ill suited to conditions in Argentina 5) results: deficits, borrowing, default and economic chaos Dollarization 1) partial dollarization indicates use of the U.S. dollar alongside domestic currency 2) full dollarization indicates use of the dollar and elimination of domestic currency 3) benefits: a) lower inflation b) decreased transactions costs c) greater openness Effects of Dollarization o U.S. monetary policy would not necessarily be appropriate for a foreign economy o Federal Reserve is not the lender of last resort for that economy o loss of seigniorage which is the income that would have been derived from interest bearing foreign reserves