5 ACCOUNTING FOR

... entity for use by managers and also persons outside the organization. c The personnel, procedures, devices, and records used by an entity to develop accounting information and communicate this information to decision makers. d The concepts, principles, and standards specifying the information which ...

... entity for use by managers and also persons outside the organization. c The personnel, procedures, devices, and records used by an entity to develop accounting information and communicate this information to decision makers. d The concepts, principles, and standards specifying the information which ...

Essential Keys to Nonprofit Finance

... Board members should have a general understanding of the types of revenue sources an organization receives and how those transactions are recorded for financial statement purposes. The most common revenue sources for a nonprofit are typically revenues and support from contributions, grants, special ...

... Board members should have a general understanding of the types of revenue sources an organization receives and how those transactions are recorded for financial statement purposes. The most common revenue sources for a nonprofit are typically revenues and support from contributions, grants, special ...

CCL Industries Appoints New President For Checkpoint

... geopolitical conditions; currency exchange rates; interest rates and credit availability; technological change; changes in government regulations; risks associated with operating and product hazards; and CCL’s ability to attract and retain qualified employees. Do not unduly rely on forward-looking s ...

... geopolitical conditions; currency exchange rates; interest rates and credit availability; technological change; changes in government regulations; risks associated with operating and product hazards; and CCL’s ability to attract and retain qualified employees. Do not unduly rely on forward-looking s ...

2001 accounting i

... in a higher cost of goods sold and therefore helps reduce the tax liability. 16) Overstating ending inventory in the current period will understate the following year’s net income. 17) The endorsement on the check represents a promise to pay. 18) The matching concept requires that the income stateme ...

... in a higher cost of goods sold and therefore helps reduce the tax liability. 16) Overstating ending inventory in the current period will understate the following year’s net income. 17) The endorsement on the check represents a promise to pay. 18) The matching concept requires that the income stateme ...

the relevance of auditing in a computerized accounting system

... perform other operations. Every company adopt the accounting system method of recording of transaction, because it is generally required that companies have to reveal certain financial and management information to the government and public users; and also because accounting is an indispensable tool ...

... perform other operations. Every company adopt the accounting system method of recording of transaction, because it is generally required that companies have to reveal certain financial and management information to the government and public users; and also because accounting is an indispensable tool ...

Accounting Answers

... capital comprises 1 000 000 ordinary shares of R2 par value. Authorised shares = 1 000 000 Issued shares = 1 525 000 / 2 = 762 500 ü Available shares = 1 000 000 – 762 500 = 237 500 ü Capital to be raised by the is sue of unissued shares ...

... capital comprises 1 000 000 ordinary shares of R2 par value. Authorised shares = 1 000 000 Issued shares = 1 525 000 / 2 = 762 500 ü Available shares = 1 000 000 – 762 500 = 237 500 ü Capital to be raised by the is sue of unissued shares ...

Financial Instruments with Characteristics of Equity The ABI`s

... mean that the capital committed by the preference shareholders is any less a part of total shareholders’ capital which represents the residual. Q3. The Board has not yet concluded how liability instruments without settlement requirements should be measured. What potential operational concerns, if an ...

... mean that the capital committed by the preference shareholders is any less a part of total shareholders’ capital which represents the residual. Q3. The Board has not yet concluded how liability instruments without settlement requirements should be measured. What potential operational concerns, if an ...

Chapter 12

... Statement of activities should separately include gains and losses on investments and other assets. Revenues should be reported as increases in one of the 3 categories of net assets. Non-profits make 2 entries when spending restricted resources: 1) in restricted fund 2) unrestricted fund. Ex ...

... Statement of activities should separately include gains and losses on investments and other assets. Revenues should be reported as increases in one of the 3 categories of net assets. Non-profits make 2 entries when spending restricted resources: 1) in restricted fund 2) unrestricted fund. Ex ...

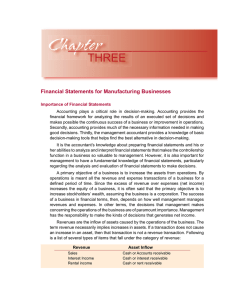

Financial Statements for Manufacturing Businesses

... In addition to understanding and utilizing financial statements and financial accounting tools, it is important that both accountants and management have a good understanding of management accounting concepts and tools. One of the most effective tools is comprehensive business budgeting. The objecti ...

... In addition to understanding and utilizing financial statements and financial accounting tools, it is important that both accountants and management have a good understanding of management accounting concepts and tools. One of the most effective tools is comprehensive business budgeting. The objecti ...

2016 Audit Report - Houston Public Library Foundation

... Accounting principles generally accepted in the United States of America require that management's discussion and analysis on pages 3 through 7 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, ...

... Accounting principles generally accepted in the United States of America require that management's discussion and analysis on pages 3 through 7 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, ...

Accounting Processes

... 4. Once all journal entries are posted, Accounting processes monthly the benefit rate and facilities and administrative cost rate allocations. a. Once all processes are complete and journal entries are posted to the general ledger, Accounting closes the period. At this point, no further transactions ...

... 4. Once all journal entries are posted, Accounting processes monthly the benefit rate and facilities and administrative cost rate allocations. a. Once all processes are complete and journal entries are posted to the general ledger, Accounting closes the period. At this point, no further transactions ...

Auditors` Reports

... three-year period ended December 31, 2012. These financial statements are the responsibility of DUNDERMIFFLIN, INC.'s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with the standards of the Public Comp ...

... three-year period ended December 31, 2012. These financial statements are the responsibility of DUNDERMIFFLIN, INC.'s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with the standards of the Public Comp ...

Chapter 4 Instructor

... Note: Accumulated Depreciation is a contra asset account, and is presented as an offset to Equipment on the balance sheet (more in Chapter 9). ...

... Note: Accumulated Depreciation is a contra asset account, and is presented as an offset to Equipment on the balance sheet (more in Chapter 9). ...

REFERENCES:

... 1996, p. xvii). Quantification has doubtlessly been the trend in business and economics for the past 50 years, but in Drucker’s opinion we still do not have the measurements we need – the measurements to give us business control ...

... 1996, p. xvii). Quantification has doubtlessly been the trend in business and economics for the past 50 years, but in Drucker’s opinion we still do not have the measurements we need – the measurements to give us business control ...

Key Accounting Issues for Nonprofits

... independent of the reporting entity (observable inputs), and (2) the reporting entity’s own assumptions about market participant assumptions developed based on the best information available in the circumstances (unobservable inputs). The notion of unobservable inputs is intended to allow for situat ...

... independent of the reporting entity (observable inputs), and (2) the reporting entity’s own assumptions about market participant assumptions developed based on the best information available in the circumstances (unobservable inputs). The notion of unobservable inputs is intended to allow for situat ...

LMC CAPITAL CORP (Form: 10KSB, Received: 03

... Capital Corp. On September 2, 1999 the Registrant increased its authorized capital to 100,000 common shares at no par value per share from its original authorized capital of 25,000 common shares at no par value. On October 13, 2000 the Registrant increased its authorized capital to 100,000,000 commo ...

... Capital Corp. On September 2, 1999 the Registrant increased its authorized capital to 100,000 common shares at no par value per share from its original authorized capital of 25,000 common shares at no par value. On October 13, 2000 the Registrant increased its authorized capital to 100,000,000 commo ...

Document

... Name of course-unit (subject): Accounting I. Language of instruction (from sample unit): English Name of course-unit in Hungarian (from sample unit): Számvitel I. ETR (USRS) course-unit code (subject unit): Validity of course-unit (from subject): ...

... Name of course-unit (subject): Accounting I. Language of instruction (from sample unit): English Name of course-unit in Hungarian (from sample unit): Számvitel I. ETR (USRS) course-unit code (subject unit): Validity of course-unit (from subject): ...

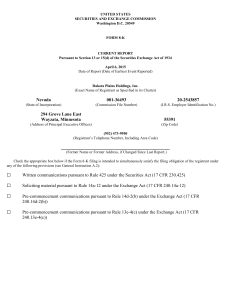

DAKOTA PLAINS HOLDINGS, INC. (Form: 8

... (a) On April 6, 2015, BDO USA, LLP (“BDO”) informed Dakota Plains Holdings, Inc. (the “Company”) of its intention to decline to stand for re-election as the Company’s independent registered accounting firm for the fiscal year ending December 31, 2015. BDO’s reports on the Company’s consolidated fina ...

... (a) On April 6, 2015, BDO USA, LLP (“BDO”) informed Dakota Plains Holdings, Inc. (the “Company”) of its intention to decline to stand for re-election as the Company’s independent registered accounting firm for the fiscal year ending December 31, 2015. BDO’s reports on the Company’s consolidated fina ...

Auditor`s Responsibility

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

Preview Sample File

... Feedback: Learning objective 1.2 – Explain the characteristics of the main forms of business organisation. Under the sole trader business structure the owner of the business has no separate legal existence from the business. The owner of the business is therefore personally liable for the debts of t ...

... Feedback: Learning objective 1.2 – Explain the characteristics of the main forms of business organisation. Under the sole trader business structure the owner of the business has no separate legal existence from the business. The owner of the business is therefore personally liable for the debts of t ...

IMPLICATIONS OF GOING CONCERN PRINCIPLE ON COMPANY

... related to it is at low enough levels not to warrant abnormal consideration by preparers, auditors or users of financial statements. Only as the level of uncertainty rises well above normal levels is it an issue relevant to a company‘s financial statements‖. (Martin, 2000) Let us now point out short ...

... related to it is at low enough levels not to warrant abnormal consideration by preparers, auditors or users of financial statements. Only as the level of uncertainty rises well above normal levels is it an issue relevant to a company‘s financial statements‖. (Martin, 2000) Let us now point out short ...