An Application on Merton Model in the Non

... the put option, but both are unobservable. However, it is possible to use prices of traded securities issued by the firm to estimate these variables. The first step in this procedure is to deduce functional relations between a firm’s underlying assets and its equity. To this end, we can state the pa ...

... the put option, but both are unobservable. However, it is possible to use prices of traded securities issued by the firm to estimate these variables. The first step in this procedure is to deduce functional relations between a firm’s underlying assets and its equity. To this end, we can state the pa ...

Value Stocks: Poised to Outperform?

... doing well. Still, even if energy continues to struggle, this company is well situated. Not only can it boast of broadly integrated operations, what with its legendary upstream operations, coupled with its pipelines and downstream refining, but it’s well diversified across the planet, plus has one o ...

... doing well. Still, even if energy continues to struggle, this company is well situated. Not only can it boast of broadly integrated operations, what with its legendary upstream operations, coupled with its pipelines and downstream refining, but it’s well diversified across the planet, plus has one o ...

EXAM FM FINANCIAL MATHEMATICS

... If the 10% interest rate was continuously compounded instead of annual effective, then it would be more beneficial to invest in the stock, rather than the forward contract. ...

... If the 10% interest rate was continuously compounded instead of annual effective, then it would be more beneficial to invest in the stock, rather than the forward contract. ...

Means and Measures to Giving Greater

... • Not directly related to price spikes, but AS value correlates with flexible and fast response demand and supply – which can reduce materiality of price spikes over time • Fuel cycles are very long, but El Nino / La Nina’s are arguably more predictable in nature – to the extent that price spikes co ...

... • Not directly related to price spikes, but AS value correlates with flexible and fast response demand and supply – which can reduce materiality of price spikes over time • Fuel cycles are very long, but El Nino / La Nina’s are arguably more predictable in nature – to the extent that price spikes co ...

Trade Alert - (SPY) - Mad Hedge Fund Trader

... *Muni bonds rocket on fiscal cliff *$40 billion a month in MBS buying is still on the menu *QE3 will work eventually, will be felt in the 30 year fixed rate home loan the most, now at 3.25% ...

... *Muni bonds rocket on fiscal cliff *$40 billion a month in MBS buying is still on the menu *QE3 will work eventually, will be felt in the 30 year fixed rate home loan the most, now at 3.25% ...

Towards a Theory of Volatility Trading

... If the futures price process is a continuous semi-martingale, then Itô’s lemma implies that E0 ln FFT0 ...

... If the futures price process is a continuous semi-martingale, then Itô’s lemma implies that E0 ln FFT0 ...

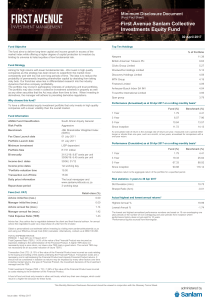

First Avenue Sanlam Collective Investments Equity Fund

... profits increases, the market price of the share will increase and this translates into a capital gain for the shareholder. Similarly, negative sentiment about the company will result in the share price falling. Shares/equities are usually considered to have the potential for the highest return of a ...

... profits increases, the market price of the share will increase and this translates into a capital gain for the shareholder. Similarly, negative sentiment about the company will result in the share price falling. Shares/equities are usually considered to have the potential for the highest return of a ...

Positive Alpha and Negative Beta (A Strategy for Counteracting

... options on the S&P 500 ETF (ticker: SPY) hedged against call options in the VIX, or VXX (which is a ETN that closely follows the movement of the VIX, as it holds positions in front and back month VIX futures). The VIX (commonly referred to as the fear index) and the S&P 500 are known to have a stron ...

... options on the S&P 500 ETF (ticker: SPY) hedged against call options in the VIX, or VXX (which is a ETN that closely follows the movement of the VIX, as it holds positions in front and back month VIX futures). The VIX (commonly referred to as the fear index) and the S&P 500 are known to have a stron ...

Course 2 Sample Exam Questions

... Carol and John shared equally in an inheritance. Using his inheritance, John immediately bought a 10-year annuity-due with an annual payment of 2500 each. Carol put her inheritance in an investment fund earning an annual effective interest rate of 9%. Two years later, Carol bought a 15-year annuity- ...

... Carol and John shared equally in an inheritance. Using his inheritance, John immediately bought a 10-year annuity-due with an annual payment of 2500 each. Carol put her inheritance in an investment fund earning an annual effective interest rate of 9%. Two years later, Carol bought a 15-year annuity- ...

1 Solutions to End-of-Chapter Problems in

... seems very unlikely to happen in the real world). A negative real rate would occur if the expected rate of price inflation were greater than the nominal rate of interest. For example, suppose ðet = 10% and it = 8%. Then rt = -2.0% (approximately). In this case lenders are effectively paying borrower ...

... seems very unlikely to happen in the real world). A negative real rate would occur if the expected rate of price inflation were greater than the nominal rate of interest. For example, suppose ðet = 10% and it = 8%. Then rt = -2.0% (approximately). In this case lenders are effectively paying borrower ...

Unconstrained Fitting of Non-Central Risk-Neutral

... One of the most important problems in calibrating option models (eg, stochasticvolatility, local-volatility, jump-di¤usion, etc) is obtaining a reliable smile surface from the (often noisy and non-contemporaneous) market prices of plainvanilla options. For some models it can be debated whether using ...

... One of the most important problems in calibrating option models (eg, stochasticvolatility, local-volatility, jump-di¤usion, etc) is obtaining a reliable smile surface from the (often noisy and non-contemporaneous) market prices of plainvanilla options. For some models it can be debated whether using ...

Scalping Option Gammas - Dean Mouscher`s masteroptions.com

... $7,850, a bit less than you made on the way up. The delta of the 112 call would now be 0.33 and the delta of the 112 put would be -0.67, for a total position delta of -17. As before, you can lock in your profit with a futures transaction, this time by buying 17 contracts. If the futures go right bac ...

... $7,850, a bit less than you made on the way up. The delta of the 112 call would now be 0.33 and the delta of the 112 put would be -0.67, for a total position delta of -17. As before, you can lock in your profit with a futures transaction, this time by buying 17 contracts. If the futures go right bac ...

IFRS 9 Financial Instruments

... IAS 32/39 Financial Instruments Part 5: EXPLANATIONS OF TERMINOLOGY An option* whose strike price* is equal to the current, prevailing price in the underlying cash spot*market. At-the-money forward An option* whose strike price* is equal to the current, prevailing price in the underlying forward ma ...

... IAS 32/39 Financial Instruments Part 5: EXPLANATIONS OF TERMINOLOGY An option* whose strike price* is equal to the current, prevailing price in the underlying cash spot*market. At-the-money forward An option* whose strike price* is equal to the current, prevailing price in the underlying forward ma ...

Chapter 3 Accounting and Finance - McGraw-Hill

... markets exist, the market value of a company does not depend on its capital structure ◦ In other words, managers cannot increase firm value by changing the mix of securities used to finance the company ...

... markets exist, the market value of a company does not depend on its capital structure ◦ In other words, managers cannot increase firm value by changing the mix of securities used to finance the company ...