Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Federal takeover of Fannie Mae and Freddie Mac wikipedia , lookup

Credit default swap wikipedia , lookup

Financial crisis of 2007–2008 wikipedia , lookup

Hedge (finance) wikipedia , lookup

CAMELS rating system wikipedia , lookup

Efficient-market hypothesis wikipedia , lookup

Leveraged buyout wikipedia , lookup

Derivative (finance) wikipedia , lookup

Synthetic CDO wikipedia , lookup

Financial Crisis Inquiry Commission wikipedia , lookup

Securitization wikipedia , lookup

Asset-backed security wikipedia , lookup

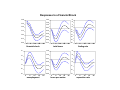

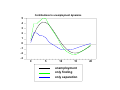

Comments on “Risk Allocation, Debt Fueled Expansion and Financial Crisis,” Beaudry and Lahiri Discussion by David López-Salido Federal Reserve Board March 5, 2010 Comments BL SF-Conference The views expressed in this discussion are solely my responsibility, and should not be interpreted as reflecting the views of the Board of Governors of the Federal Reserve System or of any other person associated with the Federal Reserve System. Comments BL SF-Conference Outline This is a nice model. It goes to the heart of the recent situation. Review Specific comments Policy implications The model emphasized the effects of credit default risk on employment. Yet, what do we know about the effects of credit shocks on the labor market dynamics? Comments BL SF-Conference Asymmetric Information and Adverse Selection Some years ago, many MBS where rated AAA –with minimal risk of default. Buyers did not worry about the quality of the exact composition of assets of the bundle, because the stream of payments was (perceived) as safe. House prices decline, the owners of MBS had strong incentive to estimate how much those securities were worth. This was the crux of the problem. At this point, everyone who considers purchasing a MBS fears Akerlof’s classic lemons problem. The buyer hopes that the seller is selling the security because, say, it needs cash, but the buyer worries that the seller may simple be trying to unload its worst-performing assets. This asymmetric information problem takes the market illiquid. Comments BL SF-Conference The great recession in a nutshell (cont.) In these circumstances, the market price of MBS reflect’s buyers’ belief that most securities that are offered for sale are low quality (fire-sale price). The true value of the average MBS may in fact be much higher. This is the hold-to-maturity price. The adverse selection problem then aggregates from individual securities to financial services institutions. Because of losses on their real estate investments, these firms are undercapitalized. Investors fear that any firm that would like to issue new equity or debt is currently overvalued. Hence, firms that attempt to recapitalize push down their market price (increasing their equity premium). Lending freezed (lemon problem again). Comments BL SF-Conference The model a detour Baseline model Risk premium, debt, and employment Dynamic Distorted economy: Default risk, asymmetric information, and adverse selection Multiple equilibria Comments BL SF-Conference Timing Trade in labor and assets markets Credit market t t+1 Production Consumption dt=φ(dt-1At) Shock: A q Workers (y) 1-q 1 θ New cohort Financiers (pdd=f+F) Existing cohort Financiers (F) Comments BL SF-Conference Risk premium, employment, and debt A d d d Comments BL d d SF-Conference d d d Dynamics Case #1 d < d dt d d t d d > Case #2 t d dt d d t0 tk tk+1 t A=θ Comments BL t0 tk A=θ SF-Conference t Comment: Frictionless model No income effect in labor supply Comments BL SF-Conference Comment: Frictionless model No income effect in labor supply Analysis of the debt thresholds (e d and d). Comments BL SF-Conference Default risk Trade in labor and assets markets Credit market t t+1 Production Consumption dt=φ(dt-1At) Shock: A q Workers (y) 1-q 1 θ New cohort Financiers (pdd=f+F) Existing cohort Financiers (F) Comments BL SF-Conference Default risk ψtψ Trade in labor and assets markets Credit market t t+1 Production Intermediaries Consumption Eψ kt=dt-1 Shock: A q Workers (y) 1-q 1 θ dt=φ(dt-1At,ψ) New cohort Financiers (pdd=f+F) Existing cohort Heterogeneity: Default Risk 1-ψ Financiers (F) Comments BL SF-Conference Default risk: Asymmetric information Workers Financiers Ψ1 Ψ2 Ψ3 Ψ4 F1 A S Y M M E ΨK ΨK+1 T R Y ΨK+2 Intermediaries C I N F O S E F2 F2 F4 I O FK Selection F2 Asymmetric Information Limited Participation by F I Z FK+1 FK+2 Fn Adverse R T N Ψn U I M T (No information) C F3 R A Symmetric Information A Fn T I O N Leverage Comments BL SF-Conference Marginal Financier Marginal financier 1 ψ Probability of default (i.e. productivity equal to zero at the beginning of t+1) Symmetric information pdt = E( ψ )E u0 (cot+1 ) y u 0 ( ct ) E( ψ ) = pkt i.e. pkt = E(ψ)pbt b pt Asymmetric information. Limited participation in credit markets. This requires to pin-down the marginal participant in the credit market (i.e. the marginal financier offering debt). pkt b = ψ pbt , b= ψ R ψm 0 ψf (ψ)dψ F( ψ ) ψi > ψm The financier holds on to her debt ψi < ψm The financier will offer debt holdings Comments BL SF-Conference Multiple equilibria: An illustration At least two equilibrium ψm = 0. Pessimistic (no insurance is providing to undertake employment/production decisions). Distorted economy (employment below autarky) ψm = 1. Symmetric information case Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Necessary and sufficient conditions for the existence. Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Necessary and sufficient conditions for the existence. Conditions for coexistence of equilibrium: Crisis as switching-mechanism Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Necessary and sufficient conditions for the existence. Conditions for coexistence of equilibrium: Crisis as switching-mechanism Distribution of credit default in the economy Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Necessary and sufficient conditions for the existence. Conditions for coexistence of equilibrium: Crisis as switching-mechanism Distribution of credit default in the economy How does affect the marginal financier? Comments BL SF-Conference Comments There is not an endogenous asset-price collapse in the model. Necessary and sufficient conditions for the existence. Conditions for coexistence of equilibrium: Crisis as switching-mechanism Distribution of credit default in the economy How does affect the marginal financier? The transmission mechanism to the real economy of credit default risk. Comments BL SF-Conference Policy implications Does the government have a clear advantage over the private sector to solve the ‘lemon-problem’? The ability to force agents to participate in mechanisms that cross-subsidize other participants. Comments BL SF-Conference Policy implications Does the government have a clear advantage over the private sector to solve the ‘lemon-problem’? The ability to force agents to participate in mechanisms that cross-subsidize other participants. Raising capital, yet this is absent in the current framework (self-insurance). Comments BL SF-Conference Policy implications Does the government have a clear advantage over the private sector to solve the ‘lemon-problem’? The ability to force agents to participate in mechanisms that cross-subsidize other participants. Raising capital, yet this is absent in the current framework (self-insurance). Optimal degree of provision of insurance to prevent panics. Comments BL SF-Conference Policy implications Does the government have a clear advantage over the private sector to solve the ‘lemon-problem’? The ability to force agents to participate in mechanisms that cross-subsidize other participants. Raising capital, yet this is absent in the current framework (self-insurance). Optimal degree of provision of insurance to prevent panics. Preventing ‘high-valuation episodes’ Comments BL SF-Conference Policy implications Does the government have a clear advantage over the private sector to solve the ‘lemon-problem’? The ability to force agents to participate in mechanisms that cross-subsidize other participants. Raising capital, yet this is absent in the current framework (self-insurance). Optimal degree of provision of insurance to prevent panics. Preventing ‘high-valuation episodes’ The responsibility fee or the Volcker rule Comments BL SF-Conference Financial shocks and labor market dynamics Credit spread decomposition (Gilchirst-Zakrajsek (2010)): Component attributable to expected default risk (M-DD). Excess bond premium: price of default risk. Analysis: Implications of shocks to the excess bond premium for labor market dynamics. Comments BL SF-Conference Finding and Separation Rates (Shimer-Updated) BLS (black) vs. CPS (blue) -20 -60 -40 -80 -100 -60 -120 -80 -140 -100 -160 1975 1980 1985 1990 1995 Job Finding 2000 2005 -350 -300 -370 -320 -390 -340 -360 -410 -380 -430 1975 1980 1985 1990 1995 Job Separation 2000 2005 Responses to a Financial Shock 0.4 0.3 0.2 0.6 3 0.4 2 0.2 1 0 -0.0 0.1 -1 -0.2 -2 -0.4 0.0 -0.1 -0.2 -3 -0.6 -4 -0.8 -5 -1.0 0 5 10 15 20 -6 0 financial shock 5 10 15 20 0 total hours 6 4 5 10 15 20 15 20 finding rate 0.4 3 0.2 2 -0.0 1 -0.2 0 -0.4 -1 -0.6 -2 2 0 -2 -4 -0.8 0 5 10 15 unemployment 20 -3 0 5 10 15 hours per worker 20 0 5 10 separation rate Contributions to unemployment dynamics 5 4 3 2 1 0 -1 -2 -3 0 5 10 15 20 unemployment only finding only separation