The Behavior of US Interest Rate Swap Spreads in Global Financial

... ratings (AAA and A). The AAA offer rates are significantly higher than the A offer rates, and the AAA bid rates are significantly lower than the A bid rates. They also document the relation between swap rates and par bond yields estimated from London interbank offered rate (LIBOR) and bid rate (LIBI ...

... ratings (AAA and A). The AAA offer rates are significantly higher than the A offer rates, and the AAA bid rates are significantly lower than the A bid rates. They also document the relation between swap rates and par bond yields estimated from London interbank offered rate (LIBOR) and bid rate (LIBI ...

Credit default swaps around the world: Investment and

... Our results indicate that CDS are more likely to be introduced on firms that are headquartered in countries with weaker creditor rights, a stronger orientation toward bank financing, and lower levels of ownership concentration. These results suggest that interest in CDS, and their ability to strengt ...

... Our results indicate that CDS are more likely to be introduced on firms that are headquartered in countries with weaker creditor rights, a stronger orientation toward bank financing, and lower levels of ownership concentration. These results suggest that interest in CDS, and their ability to strengt ...

Sovereign CDS Spreads in Europe—The Role of Global

... the role of global risk aversion, specific macroeconomic fundamentals, liquidity conditions in the CDS market, and spillovers from other countries in explaining the divergent movements in CDS of different countries witnessed during this period? Has the role of these factors changed between the two m ...

... the role of global risk aversion, specific macroeconomic fundamentals, liquidity conditions in the CDS market, and spillovers from other countries in explaining the divergent movements in CDS of different countries witnessed during this period? Has the role of these factors changed between the two m ...

Do Credit Derivatives Lower the Value of Creditor Control Rights

... to be looser than bank loan covenants to begin with (because renegotiation is more costly), one might expect the availability of CDS contracts to have less effect on bonds than on loans.5 Examining a large sample of bond offerings, we find that the average number of bond covenants per issue decrease ...

... to be looser than bank loan covenants to begin with (because renegotiation is more costly), one might expect the availability of CDS contracts to have less effect on bonds than on loans.5 Examining a large sample of bond offerings, we find that the average number of bond covenants per issue decrease ...

Essays on government debt financing costs

... In the recent years, more and more countries had to face the problem that their government debt / gross domestic product quotients dynamics were not sustainable. The most important factors in this process were smaller growth, bad structural balance of the budget, and high financing costs of the gove ...

... In the recent years, more and more countries had to face the problem that their government debt / gross domestic product quotients dynamics were not sustainable. The most important factors in this process were smaller growth, bad structural balance of the budget, and high financing costs of the gove ...

Information Risk and Credit Default Swap Markets

... A CDS as a derivative instrument offers advantages over corporate bonds and secondary loan markets, which have contributed to its growth over time, especially since the standardization of CDS contracts by the International Swaps and Derivatives Association (Callen et al., 2009). In particular, a CDS ...

... A CDS as a derivative instrument offers advantages over corporate bonds and secondary loan markets, which have contributed to its growth over time, especially since the standardization of CDS contracts by the International Swaps and Derivatives Association (Callen et al., 2009). In particular, a CDS ...

Unresolved Issues in Modeling Credit Risky Assets

... Apart from the issue of pricing individual instruments, it is necessary to describe the probability distribution of a portfolio as it evolves over time. In the original CreditMetrics framework, it is assumed that the credit quality of an obligor could have one of n possible credit ratings including ...

... Apart from the issue of pricing individual instruments, it is necessary to describe the probability distribution of a portfolio as it evolves over time. In the original CreditMetrics framework, it is assumed that the credit quality of an obligor could have one of n possible credit ratings including ...

Valuation of a CDO and an n to Default CDS Without Monte Carlo

... pays a specified rate (known as the CDS spread) on a specified notional principal until the nth default occurs among a specified set of reference entities or until the end of the contract’s life. The payments are usually made quarterly. If the nth default occurs before the contract maturity, the bu ...

... pays a specified rate (known as the CDS spread) on a specified notional principal until the nth default occurs among a specified set of reference entities or until the end of the contract’s life. The payments are usually made quarterly. If the nth default occurs before the contract maturity, the bu ...

Volatility patterns of CDS, bond and stock markets before and during

... eventually affected other financial markets and countries. Stock prices declined, borrowing costs rose and CDS spreads widened in a phase of high volatility and uncertainty. In particular, the bankruptcy of Lehman Brothers in September 2008 unfolded the consequences if the credit risk of large glob ...

... eventually affected other financial markets and countries. Stock prices declined, borrowing costs rose and CDS spreads widened in a phase of high volatility and uncertainty. In particular, the bankruptcy of Lehman Brothers in September 2008 unfolded the consequences if the credit risk of large glob ...

Download Dissertation

... if the payment dates on the CDS and bond coincide, and recovery on default is a constant fraction of face value. ...

... if the payment dates on the CDS and bond coincide, and recovery on default is a constant fraction of face value. ...

Sovereign and corporate credit risk

... transactions. Following such restrictions, Austria, Greece, and Ireland are excluded because they do not have sufficient numbers of companies that meet our data quality thresholds. The final sample includes 118 companies headquartered in eight countries. Table 1 reports the sample breakdown by count ...

... transactions. Following such restrictions, Austria, Greece, and Ireland are excluded because they do not have sufficient numbers of companies that meet our data quality thresholds. The final sample includes 118 companies headquartered in eight countries. Table 1 reports the sample breakdown by count ...

Certificates of Deposit Linked to the J.P. Morgan Efficiente Plus DS 5

... The J.P. Morgan Efficiente Plus DS 5 Index (Net ER) (the “Index”) was developed and is maintained and calculated by J.P. Morgan Securities plc (“JPMS plc”), one of our affiliates. JPMS plc acts as the calculation agent for the Index (the “index calculation agent”). The Index is a notional dynamic ba ...

... The J.P. Morgan Efficiente Plus DS 5 Index (Net ER) (the “Index”) was developed and is maintained and calculated by J.P. Morgan Securities plc (“JPMS plc”), one of our affiliates. JPMS plc acts as the calculation agent for the Index (the “index calculation agent”). The Index is a notional dynamic ba ...

Negotiable Certificates of Deposit

... National City Bank of New York to introduce negotiable CDs, which were offered first to the bank’s foreign customers in August 1960. Investor response to this move was only modest, however, due in part to the lack of a secondary market for the certificates. In February 1961 First National City Bank ...

... National City Bank of New York to introduce negotiable CDs, which were offered first to the bank’s foreign customers in August 1960. Investor response to this move was only modest, however, due in part to the lack of a secondary market for the certificates. In February 1961 First National City Bank ...

Futurization of Swaps

... the New York Stock Exchange) had tried and failed to merge with Germany’s largest exchange, Deutsche Boerse. The venerable Big Board, which has been around since the late 18th century, is now willing to turn over its keys to the Atlanta-based ICE, a relative upstart launched in 2000. With the merger ...

... the New York Stock Exchange) had tried and failed to merge with Germany’s largest exchange, Deutsche Boerse. The venerable Big Board, which has been around since the late 18th century, is now willing to turn over its keys to the Atlanta-based ICE, a relative upstart launched in 2000. With the merger ...

Credit default swaps. Contract characteristics and

... The use of CDS contracts can, therefore, meet the demand for speculation on credit risk (this is the case, for example, when buying a naked CDS – i.e. without holding a credit exposure towards the reference entity - or when selling protection without holding positions of the opposite sign) or for he ...

... The use of CDS contracts can, therefore, meet the demand for speculation on credit risk (this is the case, for example, when buying a naked CDS – i.e. without holding a credit exposure towards the reference entity - or when selling protection without holding positions of the opposite sign) or for he ...

Credit Default Swaps -new regulations and conversion

... monitor. One of the major changes was the introduction of fixed coupon payments, instead of running spreads, with an upfront payment when the contract is entered. Along with the regulatory introduction a conversion method was proposed for conversion of traditionally CDS spreads, or running spreads, ...

... monitor. One of the major changes was the introduction of fixed coupon payments, instead of running spreads, with an upfront payment when the contract is entered. Along with the regulatory introduction a conversion method was proposed for conversion of traditionally CDS spreads, or running spreads, ...

Comments on “Risk Allocation, Debt Fueled Expansion and Financial Crisis,” Beaudry

... SF-Conference ...

... SF-Conference ...

THE RELATIONSHIP BETWEEN CREDIT

... S&P AAA categories are not subdivided. Ratings below Baa3 (Moody’s) and BBB– (S&P) are referred to as “below investment grade”. Analysts and commentators often use ratings as descriptors of the creditworthiness of bond issuers rather than descriptors of the quality of the bonds themselves. This is ...

... S&P AAA categories are not subdivided. Ratings below Baa3 (Moody’s) and BBB– (S&P) are referred to as “below investment grade”. Analysts and commentators often use ratings as descriptors of the creditworthiness of bond issuers rather than descriptors of the quality of the bonds themselves. This is ...

Sovereign CDS and Bond Pricing Dynamics in the Euro-area

... that the protection seller might be unable to make payment in case of default event. The intrinsic di culty of quantifying repo costs and counterparty risk would seem to justify the choice of this simpli ed approach. This method is the most used by market practitioners to determine theoretical price ...

... that the protection seller might be unable to make payment in case of default event. The intrinsic di culty of quantifying repo costs and counterparty risk would seem to justify the choice of this simpli ed approach. This method is the most used by market practitioners to determine theoretical price ...

Total Return Swap

... Money-market funds regulated by the Central Bank (FIF funds) are considered financial institutions. ...

... Money-market funds regulated by the Central Bank (FIF funds) are considered financial institutions. ...

Chapter 1: An Introduction to Corporate Finance

... • A total return swap exchanges an interest rate return for the total return on an equity index plus or minus a spread. For example, first an investor could enter into an interest rate swap to convert fixed rate bond payments into payments that vary with a float rate, such as LIBOR. Then, the invest ...

... • A total return swap exchanges an interest rate return for the total return on an equity index plus or minus a spread. For example, first an investor could enter into an interest rate swap to convert fixed rate bond payments into payments that vary with a float rate, such as LIBOR. Then, the invest ...

Constant proportion debt obligations: what went

... notes and it uses the proceeds to buy high-quality collateral or to enter into repo agreements on eligible securities. These sit in the structure to fund protection payments in case the investment strategy, as outlined below, suffers losses. Through a total return swap with the arranging bank, the ...

... notes and it uses the proceeds to buy high-quality collateral or to enter into repo agreements on eligible securities. These sit in the structure to fund protection payments in case the investment strategy, as outlined below, suffers losses. Through a total return swap with the arranging bank, the ...

Credit default swap and bond markets: which leads the other?

... the opposite direction, which is of course not possible for bonds. Second, CDS contracts are not in limited supply like bonds, so they can be sold in arbitrarily large amounts. Third, the CDS market on a given borrower is not fragmented as the bond market is, being made up of all its successive issu ...

... the opposite direction, which is of course not possible for bonds. Second, CDS contracts are not in limited supply like bonds, so they can be sold in arbitrarily large amounts. Third, the CDS market on a given borrower is not fragmented as the bond market is, being made up of all its successive issu ...

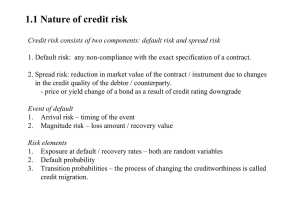

Default risk and spread risk

... The correlation between default risks of different borrowers is generally low (that is, low joint default frequency), though it can be significant for related companies, and smaller companies within the same domestic industry sector. ...

... The correlation between default risks of different borrowers is generally low (that is, low joint default frequency), though it can be significant for related companies, and smaller companies within the same domestic industry sector. ...

Credit default swap

A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer (usually the creditor of the reference loan) in the event of a loan default (by the debtor) or other credit event. This is to say that the seller of the CDS insures the buyer against some reference loan defaulting.The buyer of the CDS makes a series of payments (the CDS ""fee"" or ""spread"") to the seller and, in exchange, receives a payoff if the loan defaults. It was invented by Blythe Masters from JP Morgan in 1994.In the event of default the buyer of the CDS receives compensation (usually the face value of the loan), and the seller of the CDS takes possession of the defaulted loan. However, anyone can purchase a CDS, even buyers who do not hold the loan instrument and who have no direct insurable interest in the loan (these are called ""naked"" CDSs). If there are more CDS contracts outstanding than bonds in existence, a protocol exists to hold a credit event auction; the payment received is usually substantially less than the face value of the loan.Credit default swaps have existed since 1994, and increased in use after 2003. By the end of 2007, the outstanding CDS amount was $62.2 trillion, falling to $26.3 trillion by mid-year 2010 and reportedly $25.5 trillion in early 2012. CDSs are not traded on an exchange and there is no required reporting of transactions to a government agency. During the 2007-2010 financial crisis the lack of transparency in this large market became a concern to regulators as it could pose a systemic risk. In March 2010, the [DTCC] Trade Information Warehouse (see Sources of Market Data) announced it would give regulators greater access to its credit default swaps database.CDS data can be used by financial professionals, regulators, and the media to monitor how the market views credit risk of any entity on which a CDS is available, which can be compared to that provided by the Credit Rating Agencies. U.S. Courts may soon be following suit.Most CDSs are documented using standard forms drafted by the International Swaps and Derivatives Association (ISDA), although there are many variants. In addition to the basic, single-name swaps, there are basket default swaps (BDSs), index CDSs, funded CDSs (also called credit-linked notes), as well as loan-only credit default swaps (LCDS). In addition to corporations and governments, the reference entity can include a special purpose vehicle issuing asset-backed securities.Some claim that derivatives such as CDS are potentially dangerous in that they combine priority in bankruptcy with a lack of transparency. A CDS can be unsecured (without collateral) and be at higher risk for a default.