Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

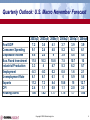

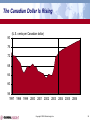

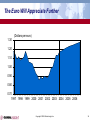

Global Insight City Travel & Tourism Teleconference U.S. Regional Economic Outlook Prospects for International Travel to the United States Quantifying Tourism for Cities November 12, 2003 Copyright © 2003 Global Insight, Inc. U.S. Regional Economic Outlook Presented to: Global Insight Teleconference Forum Presented by: Phil Hopkins Principal U.S. Regional [email protected] Copyright © 2003 Global Insight, Inc. Purpose: Provide U.S. to MSA-level Economic Context for Travel & Tourism Demand U.S. macro near-term overview Five-year forecasts by Census region Describe near-term (2003-05) outlook for states Describe near-term (2003-05) outlook for large MSAs Identify high income growth MSAs that are major tourist markets Focus on key demand indicators—income growth Copyright © 2003 Global Insight, Inc. 3 Recent U.S. Macro Indicators Favorable Unfavorable Sales Employment Orders Bond yields, mortgages Stock market Exports House values Balance of payments Industry data Profits Income growth Copyright © 2003 Global Insight, Inc. 4 Exiting the Growth Recession: Unemployment Lags, Better Sentiment Needed 12 40 10 60 8 80 6 100 4 2 60 65 70 75 80 85 Unemployment rate, percent (left scale) Consumer sentiment, 1996=100 (right scale) Copyright © 2003 Global Insight, Inc. 90 95 00 120 5 Household Debt Loads—High But Acceptable Copyright © 2003 Global Insight, Inc. 6 Consumption Boosted by Tax Cuts: Not “Tapped Out” 10 8 Real Consumption Spending, % Change vs. Year Ago Real Disposable Income, % Change vs. Year Ago Nominal Savings Rate Percent 6 4 2 0 -2 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 Copyright © 2003 Global Insight, Inc. 7 Quarterly Outlook: U.S. Macro November Forecast Real GDP Consumer Spending Disposable Income Bus. Fixed Investment Industrial Production Employment Unemployment Rate Exports CPI Housing Starts 2003q3 2003q4 2004q1 2004q2 2004q3 2004q4 7.2 3.6 4.1 3.7 3.9 3.9 9.1 2.4 4.5 5.2 6.3 6.1 9.8 2.0 9 3.9 5.8 5.5 11.5 10.3 10.8 7.5 10.7 10 3.3 4 4.7 5.3 6.2 5.7 -0.3 -0.3 0.2 0.8 1.6 2.1 6.1 6.1 6.1 6 5.9 5.8 11.2 7.3 8.4 10.8 15 12.7 2.4 1.1 0.9 1.1 2.0 2.0 1.86 1.82 1.77 1.75 1.7 1.66 Copyright © 2003 Global Insight, Inc. 8 Forecasts for Census Regions: Annual Growth Rates, 2003–08 New England Middle Atlantic South Atlantic East North Central East South Central West North Central West South Central Mountain Pacific Personal Household Income Income 4.30 4.90 4.90 5.30 4.30 5.80 3.80 4.40 4.00 4.90 4.50 5.40 4.20 5.70 4.00 5.90 3.70 5.20 Copyright © 2003 Global Insight, Inc. Total Employ. 1.10 1.10 1.90 1.10 1.40 1.40 1.30 2.20 1.60 Leisure & Hospitality Employ. 1.10 0.90 1.60 1.20 1.20 1.30 2.00 2.20 1.30 9 Growth Rate in Disposable Income, 2003–05 5.5 5.2 4.5 3.1 Copyright © 2003 Global Insight, Inc. to to to to 6.5 5.4 5.1 4.4 10 Growth Rate in Total Employment, 2003–05 1.4 1.1 0.8 0.0 Copyright © 2003 Global Insight, Inc. to to to to 3.3 1.3 1.0 0.7 11 Service Sectors Provide Job Growth State Employment Growth Rates 2003–05 Professional and business services: 3.9% Other services: 2.5% Construction: 2.3% Leisure and hospitality services: 1.5% Arts, entertainment, and recreation: 2.1% Accommodation and food services: 1.4% Education and health services: 2.3% Trade, transportation, and utilities: 1.1% Retail trade: 0.5% Wholesale trade: 1.5% Copyright © 2003 Global Insight, Inc. 12 Personal Income/Hhhld (thousands $) Large MSA Household Income Levels, 2003 $160.0 San Jose $150.0 San Francisco $140.0 $130.0 New Haven $120.0 New York City Honolulu $110.0 $100.0 New Orleans $90.0 Las Vegas $80.0 Orlando $70.0 $60.0 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 Tourism Employment Index Copyright © 2003 Global Insight, Inc. 13 Disposable Income/Household in Large MSAs in 2003: Top 20 San Jose: $131,900 Seattle: $97,800 San Francisco: $131,700 Wet Palm Beach: - $97,700 New Haven: $115,000 Anchorage: $97,500 Bergen/Passaic: $112,000 New York: $96,400 Nassau/Suffolk: $110,400 Houston: $93,600 Middlesex: $110,200 Chicago: $93,100 Newark, NJ: $109,400 Boston: $92,400 Washington, DC: $102,200 Honolulu: $92,000 Orange Co.: $101,900 Minneapolis: $90,200 Oakland: $100,900 Ventura, CA: $89,200 Large MSAs: $83,200 United States: $77,500 Copyright © 2003 Global Insight, Inc. 14 Annual Growth Rates in Total Disposable Income in Large MSAs 2003–05: Top 20 Austin: 6.7% Orlando: 5.6% Phoenix: 6.3% Houston: 5.6% Atlanta: 6.2% Tucson: 5.6% Washington, DC: 6.0% Richmond: 5.6% Las Vegas: 6.0% Riverside: 5.5% Wilmington, DE: 5.9% Middlesex: 5.5% Raleigh: 5.8% Seattle: 5.5% Dallas: 5.7% Baltimore: 5.5% Fargo: 5.7% San Antonio: 5.4% Charlotte: 5.7% Charleston, SC: 5.4% Copyright © 2003 Global Insight, Inc. 15 Final Thoughts Income Growth: disposable and per household is strongest in Sunbelt, Pacific, Mountain, and South Atlantic States. High levels of household disposable income are still in the Northeast, Great Lakes, and Pacific MSAs. Major domestic destinations/convention centers are important drivers for MSAs. Job growth would help—confidence leads to willingness to spend disposable income. Travelers are still price sensitive, but leisure travel has been sustained over the past several years. Business travel is expected back (at different price points) next year. Copyright © 2003 Global Insight, Inc. 16 Prospects for International Travel to the United States Presented to: Global Insight Teleconference Forum Presented by: Adam Sacks Managing Director Travel & Tourism 610.490.2784 [email protected] Copyright © 2003 Global Insight, Inc. U.S. Inbound: Cities Hold Greatest Stake Distribution of Overseas Inbound Travel, Top 10 Cities, 2002 Chicago 6% Metro DC 6% Boston 5% New York City 23% • Las Vegas 7% Honolulu 9% San Francisco 9% Los Angeles 13% Orlando 10% • Overseas international inbound to cities registered approximately 27 million in 2002 Over 90% of international trips Miami 12% Source: Office of Travel & Tourism Industries, International Trade Administration Copyright © 2003 Global Insight, Inc. 18 U.S. Inbound: The Big Picture Apocalypse now: 9/11, security tightening, SARS, and Iraq. The “big question” ($23 billion): Are we in the midst of a cyclical or structural shock? Copyright © 2003 Global Insight, Inc. 2006 2004 2002 2000 1998 1996 55,000,000 50,000,000 45,000,000 40,000,000 35,000,000 30,000,000 1994 Total International Inbound to US 1992 • • International inbound travel to the United States is currently at 1990 levels. 1990 • 19 Cycle versus Structure? • Arguments in favor of cyclical recovery – All other shocks have experienced a recovery to trend (Gulf War I, Asian economic crisis) – Pent-up demand • – Economy Arguments in favor of structural shift – Ongoing security fears – Ongoing security-related restrictions – Shift in preferences Copyright © 2003 Global Insight, Inc. 20 International Travel in 2003 (Growth rates 03/02) -1.0% -5.0% -2.1% -6.5% -3.3% -3.4% 3.1% 2.8% 5.5% -3.8% 4.2% -7.9% World -2.0% Copyright © 2003 Global Insight, Inc. 21 The Balance of Things To what extent is suppressed U.S. outbound making up the difference for U.S. inbound? • • • Inbound will register 10.8 million fewer trips in 2003 than in 2000, while outbound will register 6.8 fewer trips. On a balance of trade basis, that equates to a net loss of 4 million trips—and $8.9 billion. This is dependent on wouldbe outbound trips being converted into domestic travel. There is good evidence of this, as domestic leisure travel has held up relatively well in the United States throughout the recession and slow economic recovery. Copyright © 2003 Global Insight, Inc. 22 World Economy Overview and Issues • • • • • • The world economy’s performance in this cycle—marked by subpar, stop-and-go growth—has been disappointing. The U.S. rebound should lift the rest of the world, but the pace of recovery will be uneven across regions. World real GDP growth will pick up from 2.4% this year to 3.3% in 2004. Global output will remain below potential. Beginnings of modest recoveries in Western Europe and Japan. Asia’s expansion, disrupted by SARS, is regaining strength. Take-home point: Economic fundamentals are aligning to produce the beginnings of a recovery of travel to the United States. Copyright © 2003 Global Insight, Inc. 23 Sluggish Growth in the World Economy The world economy is in recession when real GDP growth is below 2% 6 5 4 3 2 1 0 -1 -2 -3 (Percent change) 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 Real GDP Industrial Production Copyright © 2003 Global Insight, Inc. 24 Fiscal and Monetary Policy Will Boost Growth Later This Year Net Cumulative Cut in Policy Fiscal Balance Rates Since January 2001 (Percentage of GDP, 2003) (Basis points) Australia -1.0 150 United Kingdom -2.7 250 0.5 275 -6.8 25 1.3 125 Switzerland -2.2 325 United States -4.0 550 Eurozone -2.5 275 Canada Japan Sweden Copyright © 2003 Global Insight, Inc. 25 Canada’s Economic Growth Has Slowed • • • • • Consumer spending, home-building, and public investment are leading Canada’s expansion. Exports have declined in 2003, however, in response to currency appreciation, Toronto’s outbreak of SARS, and beef and lumber trade restrictions. The Canadian dollar has appreciated in response to a trade surplus and attractive interest rates spreads. Yet, it remains below its PPP value of 81 U.S. cents. Travel to the United States is down 13% from its 2000 peak. Stronger Canadian dollar presents significant opportunities to attract the Canadian traveler. Copyright © 2003 Global Insight, Inc. 26 Exchange Rate Remains Effective at Predicting Canada to United States Travel 15% 8% 6% 10% 4% 5% 2% 0% 0% -2% -5% -4% -6% -10% -8% -15% -10% Canada to US Real exchange rate Copyright © 2003 Global Insight, Inc. 27 The Widening U.S. Current Account Deficit 200 (Billions of dollars) (Percent of GDP) 2 0 0 -200 -2 -400 -4 -600 -6 -800 -8 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 Current Account Deficit Deficit as % of GDP Copyright © 2003 Global Insight, Inc. 28 The Canadian Dollar Is Rising 80 (U.S. cents per Canadian dollar) 76 72 68 64 60 56 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Copyright © 2003 Global Insight, Inc. 29 Mexico: Stability Under NAFTA • • • • • Mexico has achieved remarkable macroeconomic stability under NAFTA. Cautious monetary policies have lowered inflation from 35% in the mid-1990s to 4% today. Mexico’s sluggish recovery is led by consumer spending and government-funded construction. Manufacturing remains weak, awaiting a recovery in exports. Capital inflows and an overvalued peso have hurt competitiveness against emerging markets, notably China. 2003 travel will be only 6% below the 2000 peak. Full recovery by 2005 based on economic cycle. Copyright © 2003 Global Insight, Inc. 30 Mexico’s Real GDP Growth Will Resume 8 (Percent change, real GDP) 6 4 2 0 -2 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 Mexico United States Copyright © 2003 Global Insight, Inc. 31 South America Recovers, But Risks Are High • • • Argentina’s economy is turning around as exports respond to a 65% peso depreciation. However, full recovery will take a decade and risks remain high under the current government. Brazil faces conflicting challenges: revive growth, subdue inflation, meet debt payments, and improve social conditions. High interest rates are undermining the domestic economy. In Venezuela, recovery from a deep recession will not arrive until President Chavez leaves office, perhaps in 2004. • Chile’s economy will accelerate sharply in 2004 as a free trade agreement with the United States takes effect and exports strengthen. • • Peru’s strong economic growth is threatened by social unrest. Overall, South American travel to the United States is down 50% from the 2000 peak, with the slow recovery beginning next year. Copyright © 2003 Global Insight, Inc. 32 Real GDP Growth in South America 6 (Percent change) 3 0 -3 -6 -9 -12 Brazil Argentina 2001 Venezuela 2002 2003 Copyright © 2003 Global Insight, Inc. Colombia 2004 Chile 2005 33 A Delayed Upturn in Western Europe • • • • Europe’s recovery is lagging. Unemployment is near 9%, and confidence remains depressed. A strong euro, uncompetitive labor costs, and cautious policies have undermined growth. Once inflation falls below 2%, the European Central Bank is expected cut its key rate by early 2004. An aging population, inflexible labor markets, costly pension systems, and anti-immigrant sentiments will limit long-term economic growth to 2.0-2.5%. Western European travel has begun to slowly recover. It will continue through the next two years given a strong euro and economic rejuvenation. Still, the forecast reflects a structural shift. Copyright © 2003 Global Insight, Inc. 34 Real GDP Growth Rates in European Countries (Percent change) 4 3 2 1 0 France Germany 2001 Italy 2002 2003 Spain 2004 Copyright © 2003 Global Insight, Inc. U.K. 2005 35 The Euro Will Appreciate Further (Dollars per euro) 1.30 1.20 1.10 1.00 0.90 0.80 0.70 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Copyright © 2003 Global Insight, Inc. 36 Slow Progress in Japan • The economy’s acceleration in 2003 reflects broad gains in real exports, consumer spending, and business investment. • Japan’s economy suffers from several long-term problems: asset deflation, bad bank loans, rising government debt, ineffective monetary policies, and structural inefficiencies. • • • A more expansionary monetary policy has emerged, easing the pain of restructuring in the banking and industrial sectors. The Bank of Japan will intervene in currency markets to keep the yen from appreciating much beyond 110 per dollar. Despite a decline of 44% from its 1997 peak, Japan is our #2 overseas market and must be fostered. However, a shift to closer destinations is structural. Full recovery is not expected in the next five years. Copyright © 2003 Global Insight, Inc. 37 Japan’s Economy Has Limited Growth Potential Japan’s long-term real GDP growth trend is only 1.8%; the country’s population will peak in 2007 (Percent change, real GDP) 7 6 5 4 3 2 1 0 -1 1987 1990 1993 1996 1999 Copyright © 2003 Global Insight, Inc. 2002 2005 2008 38 Other Asia/Pacific: A Bright Spot • • Asia’s rapid growth is led by a boom in exports and high-tech industries. Monetary and fiscal policies are accommodating. In South Korea, consumer spending and home-building have retrenched after the borrowing binge of recent years. • China’s strong expansion is driven by foreign direct investment, exports, and public infrastructure spending. • China, Hong Kong, and Malaysia will benefit from the dollar’s depreciation. By 2006, China will be forced to revalue. • • Certain key markets have declined only slightly since 2000 (India, Philippines, and South Korea). Australia is on the mend. Beginning in 2004, there’s a full-swing turnaround for Asian travel to the United States, but it is still 10% below the 2000 peak in 2007. Copyright © 2003 Global Insight, Inc. 39 Asian Outbound Travel: Rebound to Come (Compound Annual Growth, 2003-2008) (Compound annual growth, 2004-08) Copyright © 2003 Global Insight, Inc. 40 U.S. Inbound: At a Turning Point Annual Percentage Change 10.0% 5.0% Ea st si a M id d le A ce an ia O er ic a So u th A m Eu ro pe W es te rn -10.0% M ex ic o C -5.0% an ad a 0.0% -15.0% -20.0% -25.0% -30.0% 2002 2003 2004 Copyright © 2003 Global Insight, Inc. 2005 41 Conclusions • • • • • U.S. and global economic expansions are underway; economic growth will strengthen in the months ahead. South America, Japan, and Europe are experiencing systemic challenges, slowing their economic recoveries. Widening current account imbalances will lead to more dollar depreciation. This will help Canadian and European recovery in particular. Declines in many markets represent a structural shift in demand for travel to the United States—not a typical cycle. Best opportunities for recovery lie with Canada, the United Kingdom, Germany, and selected Asian markets. Copyright © 2003 Global Insight, Inc. 42 Quantifying Tourism for Cities Presented to: Global Insight Teleconference Forum Presented by: Adam Sacks Managing Director Travel & Tourism 1.610.490.2784 [email protected] Copyright © 2003 Global Insight, Inc. Outline • • • • Challenges to measuring tourism at the city level Data sources for measuring city tourism Techniques for measuring city tourism A solution: City Tourism Impact Copyright © 2003 Global Insight, Inc. 44 Challenges to Measuring City Tourism • Geographic distinctions • • Limited samples on syndicated data • • MSA, counties, and partial counties After top 40-50 cities, data breaks down Determining economic linkages • Determining the value of travel to a city’s economy, employment, payroll, and tax base is not straightforward Copyright © 2003 Global Insight, Inc. 45 Data Sources for City Tourism • Demand side • • • OTTI in-flight survey Supply side • • • • Syndicated national surveys (DK Shifflet) 4-5 digit sales and employment BLS, BEA, and Global Insight Hotel data (Smith Travel) Economic Model • IMPLAN Mijk = APMijk * Mijk / ^Yi * Y Copyright © 2003 Global Insight, Inc. 46 Data Sources for City Tourism, DEMAND • DK Shifflet PERFORMANCE/MonitorSM • • • • • • Largest sample of domestic travelers in the industry allows deeper measurement Comparable survey results across the United States with representative stratified sample Provides city-level traveler volume and profile information to approximately 30 cities 135,000 households contacted for each month of the year (ask about past 3 months travel behavior) Census-balanced, projectable to U.S. population Travel to every U.S. destination tracked at the city and county level since 1992—over ten years of trends analysis Copyright © 2003 Global Insight, Inc. 47 Data Sources for City Tourism, DEMAND • OTTI Data • • • Volumes: Immigration and Naturalization Service (INS) partnership (all U.S. non-citizens must complete INS I-94 to enter the United States) Details: OTTI In-flight survey provides activities, traveler profile, and destinations Challenges with in-flight survey: limited sample, some issues with coverage, and excludes Canada and Mexico Copyright © 2003 Global Insight, Inc. 48 Data Sources for City Tourism, SUPPLY • • Supply Side Data • • • Provides information on identifiable sectors (accommodation, recreation, transportation) NAICS vs. SIC NAICS provides new opportunities! • • • • Sales and employment 350 new industries Transportation, entertainment, recreation, and lodging all have new industry definitions and categories By early next year, Global Insight will have completed complete historical conversion of its county-level databases at the four-digit level Remaining challenge – How to determine tourism’s share of food and beverage and retail, esp. when related to day trips. Copyright © 2003 Global Insight, Inc. 49 Techniques for Measuring City Tourism Bottom line: Combination of demand, supply, and economic modeling Demand Side Supply Side Copyright © 2003 Global Insight, Inc. Expenditures Output: volumes, spending, jobs, wages, taxes, economic impact Estimation Techniques • Economic Model 50 Techniques for Measuring City Tourism • Sample of Estimation Techniques • Option 1: Reconcile discrepancies between demand and supply side – Use this reconciliation to estimate non-identifiable tourism expenditures • • • – Day trips and international are particularly important Option 2: Use destination-specific information wherever possible Option 3: For smaller cities, need to rely more on supply side and local information/educated assumptions Option 4: Determine ratio of day trips to overnight trips using multiple-year aggregation of demand data. Can apply this to supply side data on lodging to estimate day trip component. Copyright © 2003 Global Insight, Inc. 51 City Tourism Impact Study • • A partnership product between Global Insight and DK Shifflet and Associates. Objective: Provide affordable and comparable visitor and economic impact results for top U.S. cities. • • • • • • Benchmarking of top 100 cities Consistent approach using all available data (includes both domestic and international) Industry rankings for each city Composition of tourism impact Provides total visitor volume, expenditures, and economic impact (production, wages, employment ,and taxes) Official launch in spring 2004 Copyright © 2003 Global Insight, Inc. 52 Thank you! Adam Sacks Managing Director Travel & Tourism 1.610.490.2784 [email protected] Copyright © 2003 Global Insight, Inc. 53