Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

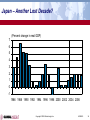

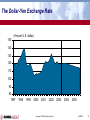

Post-War Economic Scenarios: The Long-Awaited Boom or More Stagnation? Nariman Behravesh Chief Economist Copyright © 2003 Global Insight, Inc. Outline of the Presentation Uncertainty about the outcome of the war in Iraq did inhibit consumer and business spending Consumer and business fundamentals are stronger in North America and non-Japan Asia than in Europe and Japan The risks to the outlook are still predominantly on the downside Post-war risk How big of a threat is a falling dollar to the rest of the world economy? Copyright © 2003 Global Insight, Inc. 4/29/2003 2 Economic Implications of the Iraq War Copyright © 2003 Global Insight, Inc. Economic Implications of the War – So Far Coalition forces now control about 100% of Iraqi oil supplies – the worst-case oil-disruption scenario is now very unlikely, but sabotage is still possible The “war premium” has fallen despite some residual volatility Oil prices U.S. dollar A messier than anticipated post-war picture could produce more market volatility Copyright © 2003 Global Insight, Inc. 4/29/2003 4 War and the Global Recovery The impact of war-related uncertainty may be overstated; however, it did have an effect, especially on capital spending Consumer confidence has begun to rebound, but what will be the impact on spending? Because of policy stimulus already in place, the post-war rebound in the U.S. is likely to be stronger than in Europe or Japan It will take a couple of months after the end of the war for the recovery to pick up steam Hardest hit have been the conflict-sensitive sectors (trade, tourism, luxury goods, etc.) Longer-run damage to trade and the global economy from the pre-war diplomatic fallout is likely to be limited Copyright © 2003 Global Insight, Inc. 4/29/2003 5 U.S. Consumer Confidence Fell Sharply, But is Beginning to Rebound (University of Michigan Consumer Sentiment Survey) 110 100 90 April = 83 80 70 60 1978 Low point of Gulf War = 65 1981 1984 1987 1990 1993 Copyright © 2003 Global Insight, Inc. 1996 1999 2002 4/29/2003 6 European Union Consumer Confidence Continues to Decline from Highs in 2000 (European Commission Consumer Confidence Survey) 5 0 -5 -10 -15 -20 March = -20 -25 -30 1984 1986 1988 1990 1992 1994 Copyright © 2003 Global Insight, Inc. 1996 1998 2000 2002 4/29/2003 7 Japanese Consumer Confidence at Near-Record Lows (Current Consumption Survey, Japanese Cabinet Office) 48 46 44 42 40 38 36 1984 1986 1988 1990 1992 1994 Copyright © 2003 Global Insight, Inc. 1996 1998 2000 2002 4/29/2003 8 U.S. Consumers Support Global Growth While Japanese and German Spending Lag (Nominal retail sales, percent change from a year earlier, six-month moving average) 10 5 0 -5 -10 1998 1999 2000 2001 United States Japan Copyright © 2003 Global Insight, Inc. 2002 2003 Germany 4/29/2003 9 European Consumer Spending Heading South (Nominal retail sales, percent change from a year earlier, six-month moving average) 7.5 6.0 4.5 3.0 1.5 0.0 -1.5 -3.0 -4.5 Jan-01 Jul-01 Jan-02 Germany France Copyright © 2003 Global Insight, Inc. Jul-02 Jan-03 United Kingdom 4/29/2003 10 Eurozone Consumers Continue to Hold Back on Spending (Seasonally adjusted retail sales, percent change from a year earlier, six-month moving average) 5 4 3 2 1 0 1998 1999 2000 2001 Copyright © 2003 Global Insight, Inc. 2002 2003 4/29/2003 11 Iraq War Scenarios Copyright © 2003 Global Insight, Inc. Baseline – Short War Global Insight view for the past year Limited coalition casualties No major oil disruption Oil prices average $32 in Q1, $28 in Q2, and $24 in the second half of 2003 After a brief rally, the dollar falls gradually, losing 8% of its value against industrial country currencies during 2003 Rebounding confidence and stock prices help to bolster growth Tax cuts plus additional $70 billion in defense spending help to sustain the recovery in the U.S. – a little more fiscal flexibility in Europe The Fed leaves interest rates unchanged, but the ECB cuts 50bp 90% probability Copyright © 2003 Global Insight, Inc. 4/29/2003 13 Long Post-War Conflict Post-war conflict drags on for six months or more with higher coalition casualties Confidence falls further and remains depressed longer Because of sabotage, oil prices spike to $50 per barrel and average $35 per barrel in 2003 Defense spending rises by $100 billion The dollar falls by more than 10% on a trade-weighted basis The Fed cuts interest rates by another 50 basis points 10% probability Copyright © 2003 Global Insight, Inc. 4/29/2003 14 World Growth (Percent change, annual rate) 4 3.5 3 2.5 2 1.5 1 0.5 0 2001 2002 2003 2004 Long Post-War Conflict 2005 2006 2007 Baseline-Short War Copyright © 2003 Global Insight, Inc. 4/29/2003 15 Post-War Scenarios The Long-Awaited Boom U.S. capital spending recovers Strong rebound in North America and non-Japan Asia in second half of 2003 Tepid recovery in Japan and Europe More Stagnation U.S. capital spending does not recover until early 2004 Consumer spending decelerates further No rebound in growth until 2004 Copyright © 2003 Global Insight, Inc. 4/29/2003 16 Iraq’s Bright Post-War Future Oil revenues of $10-$15 billion in the first year and up to $20 billion in the second year Potentially lucrative agricultural sector – good land and lots of water from the Tigris and the Euphrates rivers (the Fertile Crescent of biblical times) Tourism could also be big – Najaf and Karbala are the two holiest cities of the Shiite sect of Islam The large well-educated Iraqi diaspora will help to revive the economy Copyright © 2003 Global Insight, Inc. 4/29/2003 17 Post-War Economic Risk – A Rapidly Falling U.S. Dollar The huge U.S. current account deficit will continue to pull down the dollar… …However, growth differentials will prevent a hard landing What role will Asian central banks play in propping up the dollar? What will the European Central Bank do if the euro rises another 10% in each of the next two years? Copyright © 2003 Global Insight, Inc. 4/29/2003 18 A Gaping Imbalance (Billions of dollars) (Percent of GDP) 200 2 0 0 -200 -2 -400 -4 -600 -6 -800 -8 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 Current Account Deficit Deficit as % of GDP Copyright © 2003 Global Insight, Inc. 4/29/2003 19 The Dollar is Overvalued (Real trade-weighted dollar index, 1996=1.0) 1.5 1.4 1.3 1.2 1.1 1.0 0.9 0.8 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 Developing Countries Industrial Countries Copyright © 2003 Global Insight, Inc. 4/29/2003 20 Baseline Forecast Copyright © 2003 Global Insight, Inc. Sluggish World Growth The world economy is in recession when real GDP growth is below 2%. (Percent change in real GDP) 5 4 3 2 1 0 1986 1989 1992 1995 1998 Copyright © 2003 Global Insight, Inc. 2001 2004 2007 4/29/2003 22 Growth Imbalances Real GDP Growth Rates Canada U.S. U.K. France Germany Italy Japan 0 1 2 2002 2003 Copyright © 2003 Global Insight, Inc. 3 4 4/29/2003 23 Parallels with Japan Japan Weak Domestic Demand Deflation Real Interest Rates Too High Real Exchange Rate Too High Fiscal Rigidity Financial Stress Heavy Dependence on Bank Financing High Debt Levels Burst Asset Bubbles Rigid Labor Markets Poor Corporate Governance • • • • • • • • • • • Copyright © 2003 Global Insight, Inc. U.S. • ? • • • Germany • ? • • • • • • • • • 4/29/2003 24 Debt Is High in Much of the G7 Household debt as a percent of disposable personal income 140 130 Japan 120 110 United Kingdom 100 United States 90 80 Germany 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001* Source: OECD; National statistics *Estimate Copyright © 2003 Global Insight, Inc. 4/29/2003 25 U.S. – Reasons to Be Optimistic The worst-case war scenarios did not happen Inflation is not a threat Oil prices have fallen Interest rates are at a 41-year low Fiscal policy is (and will continue to be) stimulative The unemployment rate is not that high by historical standards Cash flow is strong – how will it be spent? Inventories are very low High-tech bust is over Productivity growth remains strong Copyright © 2003 Global Insight, Inc. 4/29/2003 26 U.S. – Reasons to Be Pessimistic U.S. corporations are still extremely risk averse Capacity utilization is still very low Job losses continue Debt levels are high No help from the rest of the world Copyright © 2003 Global Insight, Inc. 4/29/2003 27 No Employment Growth So Far The U.S. lost 2.0 million jobs from March 2001 to March 2003 (Percent change, annual rate) 3 2 1 0 -1 -2 -3 1998 1999 2000 2001 2002 2003 Copyright © 2003 Global Insight, Inc. 2004 2005 2006 4/29/2003 28 The U.S. Expansion Will Strengthen 8 (Percent change, annual rate) (Percent) 7 6 6 4 5 2 4 0 3 -2 2 1998 1999 2000 2001 2002 Real GDP Growth 2003 2004 2005 2006 Unemployment Rate Copyright © 2003 Global Insight, Inc. 4/29/2003 29 Europe Remains a Drag on Global Growth Growth likely to remain subdued through the end of 2003 Improving global economic/geopolitical outlook will be crucial Exports will remain key to growth Recovery will be constrained by Tight monetary and fiscal policies Strong euro Structural problems will limit longer-term growth Copyright © 2003 Global Insight, Inc. 4/29/2003 30 Forecasts for Europe (Percent change in real GDP) 3 2 1 0 France Germany 2001 Italy 2002 2003 Spain 2004 Copyright © 2003 Global Insight, Inc. U.K. 2005 4/29/2003 31 The Dollar-Euro Exchange Rate (Dollars per euro) 1.20 1.10 1.00 0.90 0.80 0.70 1997 1998 1999 2000 2001 2002 Copyright © 2003 Global Insight, Inc. 2003 2004 2005 4/29/2003 32 Japan – Another False Dawn? Third recession in a decade is barely over – due primarily to exports Debt and deflation continue to present big problems Risk of a meltdown is far less than the risk of secular stagnation Legacy of supply- and demand-side failures Mismatch of policy response and economic challenges unparalleled in developed world Reforms are going nowhere – again Copyright © 2003 Global Insight, Inc. 4/29/2003 33 Japan – Another Lost Decade? (Percent change in real GDP) 7 6 5 4 3 2 1 0 -1 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 Copyright © 2003 Global Insight, Inc. 4/29/2003 34 The Dollar-Yen Exchange Rate (Yen per U.S. dollar) 150 140 130 120 110 100 90 80 1997 1998 1999 2000 2001 2002 Copyright © 2003 Global Insight, Inc. 2003 2004 2005 4/29/2003 35 Asia: Mini-Growth Locomotive? Outlook Strong growth will likely ease in 2003 – although exports are booming China and Korea will continue to lead the pack Inflation will remain tame in the near-term Risks SARS Deflation Dependence on U.S. imports Non-economic shocks: terrorist attacks Rapid consumer credit expansion (South Korea, Hong Kong & Thailand) Fiscal strain Under-valued exchange rates Excluding Japan, Asia produces more than a tenth of world GDP and buys nearly a fifth of world imports Copyright © 2003 Global Insight, Inc. 4/29/2003 36 Asian Growth (Percent change in real GDP) 9 6 3 0 -3 China Hong Kong 2001 2002 Taiwan 2003 India 2004 Copyright © 2003 Global Insight, Inc. Australia 2005 4/29/2003 37 Asian Growth (Percent change in real GDP) 9 6 3 0 -3 Indonesia S. Korea 2001 Malaysia Philippines Singapore 2002 2003 2004 Copyright © 2003 Global Insight, Inc. Thailand 2005 4/29/2003 38 Latin America: Economic Prospects Worst recession in two decades is almost over Super competitive currencies will help Argentina and Brazil – as soon as the global economy recovers On the other hand, Mexico has lost competitiveness, especially to China Argentina’s depression is ending Brazil’s huge challenge – restore growth, keep inflation low, meet debt payments, and improve social conditions and income distribution Copyright © 2003 Global Insight, Inc. 4/29/2003 39 Latin America at a Glance (Percent change in real GDP) 8 4 0 -4 -8 -12 -16 Latin America Argentina 2001 2002 Brazil 2003 Copyright © 2003 Global Insight, Inc. Mexico 2004 Venezuela 2005 4/29/2003 40 Other Regions: Growing But Vulnerable Emerging Europe is being helped by investment flows from and exports to the EU – but weak growth in Western Europe is hurting Russia and other former Soviet republics are sensitive to oil price gyrations – and slow progress on reforms is a drag on growth Oil price volatility, the War Against Terrorism, the IsraeliPalestinian conflict, and the war against Iraq have all undermined investment, construction, and tourism in the Middle East and North Africa Weak commodity prices, the global recession, and the AIDS epidemic have lowered growth prospects in sub-Saharan Africa Copyright © 2003 Global Insight, Inc. 4/29/2003 41 Growth in Other World Regions (Percent change in real GDP) 7 6 5 4 3 2 1 0 Eastern Europe FSU 2001 2002 Middle East 2003 2004 Copyright © 2003 Global Insight, Inc. Africa 2005 4/29/2003 42 The Bottom Line A weak but sustained recovery is underway The short Iraq war will likely delay but not kill off the global recovery The risks are still predominantly on the downside The large growth disparities – and resulting current account imbalances – could force big currency realignments North America (among industrialized regions) and Asia (among emerging regions) offer the best short- and medium-term growth opportunities Copyright © 2003 Global Insight, Inc. 4/29/2003 43