Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

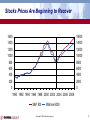

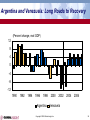

Outlook for the Americas: Are the Clouds Lifting? Presented to: Global Insight Outlook Seminar Atlanta, Georgia April 29, 2003 Presented by: Sara Johnson Managing Director, Global Macroeconomics Group Copyright © 2003 Global Insight, Inc. The Iraq Cloud Has Lifted; What Next? • Success in Iraq resolves a major uncertainty, enabling investment, staffing, and travel plans to move forward. • The United States remains the region’s growth engine. Fiscal stimulus and an upturn in capital spending will boost U.S. growth from 2.6% this year to 4.2% in 2004. • South America’s political instability threatens its economic progress. Extremely competitive currencies will drive near-term growth in Argentina and Brazil. • • U.S. dollar depreciation will generally help the Americas, with the exception of Canada. The 34-nation Free Trade Area of the Americas agreement will move forward, with the goal of 2006 enforcement. Copyright © 2003 Global Insight, Inc. 2 North America Produces 91% of Americas’ GDP … (Percent of Americas’ GDP, 2002) South Mexico America Canada 5% Central 7% 6% America & Caribbean 2% United States 80% Copyright © 2003 Global Insight, Inc. 3 … with Half of the Region’s Population (Percent of Americas’ Population, 2002) Caribbean 4% Central America 4% South America 42% United States 34% Mexico 12% Canada 4% Copyright © 2003 Global Insight, Inc. 4 The U.S. and Canada Are Leading the Recovery 5 (Percent change, real GDP) 4 3 2 1 0 -1 -2 United States Mexico Canada 2001 2002 2003 2004 Copyright © 2003 Global Insight, Inc. Other Americas 2005 5 U.S. Recovery Forces Are in Place • • • • • • • Expansionary monetary and fiscal policies Resilient consumer spending End of the high-tech bust Lean inventories Strong productivity growth Low inflation, falling oil prices A successful outcome in Iraq sets the stage for solid growth in late 2003 and 2004. Copyright © 2003 Global Insight, Inc. 6 Reasons for Caution • • • • • • U.S. companies are still very risk averse Employment losses through March Low capacity utilization Household financial stress Weak export markets SARS and geopolitical risks Copyright © 2003 Global Insight, Inc. 7 The U.S. Expansion Will Strengthen 8 (Percent change, annual rate) (Percent) 7 6 6 4 5 2 4 0 3 -2 2 1998 1999 2000 2001 2002 Real GDP Growth 2003 2004 2005 2006 Unemployment Rate Copyright © 2003 Global Insight, Inc. 8 Shifting Sources of Growth in the U.S. Economy 1998 2001 2002 2003 2004 4.28 0.25 2.45 2.60 4.18 Consumption 3.18 1.67 2.15 1.61 2.67 Structures Equip. & Software Residential 0.21 -0.05 -0.52 -0.15 0.19 1.27 -0.61 -0.15 0.42 0.86 0.32 0.01 0.17 0.10 -0.11 Federal -0.05 0.29 0.47 0.69 0.19 State & Local 0.39 0.36 0.35 0.02 0.05 Net Trade -1.20 -0.18 -0.66 -0.14 -0.16 GDP Growth (%) Contributions Copyright © 2003 Global Insight, Inc. 9 Price and Wage Inflation Will Stay Mild 6 5 4 3 2 1 0 -1 -2 -3 (Year-over-year percent change) 1998 1999 2000 CPI 2001 2002 Producer Prices 2003 2004 2005 2006 Employment Cost Index Copyright © 2003 Global Insight, Inc. 10 The Federal Reserve Will Start to Raise Interest Rates in December 2003 10 (Percent) 8 6 4 2 0 1998 1999 2000 Federal Funds 2001 2002 2003 2004 10-Year Treasury Yield Copyright © 2003 Global Insight, Inc. 2005 2006 Mortgage Rate 11 Stocks Prices Are Beginning to Recover 1600 1400 1200 1000 800 600 400 200 0 16000 14000 12000 10000 8000 6000 4000 2000 0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 S&P 500 Wilshire 5000 Copyright © 2003 Global Insight, Inc. 12 Real Consumer Spending and Confidence 7 (Annual percent change, 1996$) (Michigan Index, 1967=1.0) 110 6 105 5 100 4 95 3 90 2 85 1 80 0 75 1998 1999 2000 2001 2002 2003 Real Consumption Growth 2004 2005 2006 Consumer Sentiment Copyright © 2003 Global Insight, Inc. 13 Home-Building Will Decrease in 2003-05 (Housing starts, millions of units) 2.4 2.0 1.6 1.2 0.8 0.4 0.0 1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 Single-Family Multi-Family Copyright © 2003 Global Insight, Inc. 14 Manufacturing Capacity Utilization Is Low (Percent) 90 1960-2002 average = 81.2 85 80 75 70 65 1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 Copyright © 2003 Global Insight, Inc. 15 An Uneven Recovery in Business Investment (Percent change, 1996 dollars) 30 20 10 0 -10 -20 Structures Computers 2000 2001 Software 2002 Communic. Equipment 2003 Copyright © 2003 Global Insight, Inc. Other Equipment 2004 16 A Surge in Federal Spending: Government Purchases of Goods and Services 9 (Year-over-year percent change) 6 3 0 -3 -6 1990 1992 1994 1996 1998 Federal 2000 2002 2004 2006 State & Local Copyright © 2003 Global Insight, Inc. 17 Government Budgets Are Back in Deficit (Billions of dollars, fiscal years) 300 200 100 0 -100 -200 -300 -400 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Federal State & Local Copyright © 2003 Global Insight, Inc. 18 Real U.S. Exports and Imports Reflect the Business Cycle and Exchange Rates 16 (Year-over-year percent change) 12 8 4 0 -4 -8 -12 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Real Exports Real Imports Copyright © 2003 Global Insight, Inc. 19 A Healthy Canadian Economy • • • • • Home-building, consumption, and public investment led Canada’s solid 3.4% growth in 2002. Business investment is recovering in 2003, but auto and housing markets are cooling off a bit. To curb inflation, the Bank of Canada is raising interest rates; its key rate will reach 5% in mid-2004. High relative interest rates and a trade surplus will boost the Canadian dollar to 70 U.S. cents in 2004. Canada’s failure to support the Iraq war effort has chilled relations with the United States. Copyright © 2003 Global Insight, Inc. 20 Canada’s Real GDP Growth (Percent change, 1997 dollars) 6 5 4 3 2 1 0 -1 -2 1986 1989 1992 1995 Canada 1998 2001 2004 2007 United States Copyright © 2003 Global Insight, Inc. 21 Mexico: Integration Under NAFTA • • • • • Mexico’s sluggish recovery is led by consumer spending and construction activity. Manufacturing remains weak, awaiting a pick-up in the U.S. economy and maquiladora exports. Capital inflows have supported the peso in recent years, hurting competitiveness against China and other emerging markets. The peso is expected to depreciate. Mexico has achieved remarkable macroeconomic stability under NAFTA. Cautious monetary policies have lowered inflation to around 5%. President Fox’s structural reforms are stalled in the face of PRI opposition; July congressional elections are pivotal. Copyright © 2003 Global Insight, Inc. 22 Mexico’s Inflation Has Subsided as a Result of Cautious Monetary Policies (Consumer price index, percent change) 35 30 25 20 15 10 5 0 1990 1992 1994 1996 1998 2000 Copyright © 2003 Global Insight, Inc. 2002 2004 2006 23 Mexico’s Long-Term Economic Growth Is 4-5% 8 (Percent change, real GDP) 6 4 2 0 -2 1986 1989 1992 1995 Mexico 1998 2001 2004 2007 United States Copyright © 2003 Global Insight, Inc. 24 Brazil Has a Difficult Balancing Act • • • • • Brazil faces conflicting challenges—revive growth, subdue inflation, meet debt payments, and improve social conditions and income distribution. Growth in agricultural and industrial exports is reviving the economy, but consumption and investment remain weak. Capital flight sent the real to new lows in 2002, driving up inflation and interest rates. The Selic rate is 26.5%. A large, inefficient government sector is a drag on the economy; taxes take 36% of GDP. Foreign capital—essential for strong growth—will return if economic policies are sound. President Lula da Silva aims to enact pension and tax reforms this year. Copyright © 2003 Global Insight, Inc. 25 Brazil’s Economy Gradually Improves 8 (Percent change, real GDP) 6 4 2 0 -2 -4 1986 1989 1992 1995 Brazil 1998 2001 2004 2007 South America Copyright © 2003 Global Insight, Inc. 26 Argentina Is Still Risky • • • • • Argentina’s economy is recovering from its free fall, but risks remain very high in a fragile political environment. After a 70% drop in 2002, the peso has appreciated 20% in recent months, temporarily cooling inflation. Import substitution is boosting domestic production and generating a current account surplus. The liberation of the corralón (a freeze on time deposits) will provide a needed stimulus to consumer spending. Debt default will limit growth for years, since investors have abandoned the country. It will take nearly a decade for real per capita GDP to regain its 1998 peak. Copyright © 2003 Global Insight, Inc. 27 Argentina and Venezuela: Long Roads to Recovery (Percent change, real GDP) 12 8 4 0 -4 -8 -12 1990 1992 1994 1996 1998 Argentina 2000 2002 2004 2006 Venezuela Copyright © 2003 Global Insight, Inc. 28 Venezuela in Crisis • • • • • Venezuela’s political turmoil has done lasting damage to PDVSA, business investment, and the economy. After an 8.9% contraction in 2002, real GDP is expected to decrease 10% this year. Venezuela suspended foreign currency trading in January, effectively paralyzing imports. We expect a 30% bolívar depreciation and 40% CPI inflation in the next 12 months. A huge fiscal deficit (7% of GDP) will limit the government’s ability to finance social programs, exacerbating divisions. We expect that the Chavez presidency will end by referendum in late 2003 or early 2004. Copyright © 2003 Global Insight, Inc. 29 Colombia, Chile, and Peru • Colombia’s economic growth is held back by intensified guerilla violence. President Uribe initiated an expansion of military and police forces, along with major fiscal reforms. • Chile’s economy will accelerate in 2003 and 2004 as the world economy, copper prices, and exports strengthen. • • • Signing of the U.S.-Chile Free Trade Agreement is delayed. Peru achieved 5% growth in 2002, thanks to rising copper, zinc, and gold production. Consumer spending and construction are now taking over as engines of growth. The halt of President Toledo’s privatization program due to public protests will discourage foreign investment. Copyright © 2003 Global Insight, Inc. 30 Real GDP Growth in South America (Percent change) 6 5 4 3 2 1 0 Bolivia Chile 2001 Colombia 2002 2003 Ecuador 2004 Copyright © 2003 Global Insight, Inc. Peru 2005 31 Caribbean Economies Await Tourism Revival • The number of international visitors to the Caribbean will decline for a third consecutive year. A strengthening U.S. economy will spark a strong rebound in 2004. • The Dominican Republic will lead the region’s growth, thanks to inflows of foreign investment, rising exports from the free-trade zone, and an expanding tourism industry. • Puerto Rico’s manufacturing is declining as the U.S. phases out tax-free repatriation of profits. Public transit and port infrastructure projects are driving growth. • • Trade sanctions and weakness in its tourism, sugar, and nickel industries will undermine Cuba’s economy. Trinidad & Tobago is benefiting from investments to develop its oil and gas reserves. Copyright © 2003 Global Insight, Inc. 32 International Tourism Recoveries Delayed 16 (Percent change in international visitor arrivals) 12 8 4 0 -4 -8 1996 1998 North America 2000 2002 Caribbean 2004 2006 Central & South America Copyright © 2003 Global Insight, Inc. 33 Real GDP Growth in the Caribbean 6 (Real GDP, percent change) 5 4 3 2 1 0 -1 Bahamas Dominican Republic Jamaica 2001 2003 2002 Puerto Rico 2004 Copyright © 2003 Global Insight, Inc. Trinidad & Tobago 2005 34 Central America Depends on Exports • • • • • Central America is struggling with a decline in tourism and weak prices for exports of coffee, sugar, and bananas. Costa Rica has the region’s most attractive investment environment--an established democracy, well-educated population, and a stable economy. The U.S. has de-certified Guatemala for failure to counter drug trafficking and official corruption. A high crime rate will deter private investment. El Salvador sells two-thirds of its exports to the United States and depends on rising remittances from migrants. Panama’s growth will pick up in the second half of 2003 as canal traffic and re-exports from the free trade zone recover. Copyright © 2003 Global Insight, Inc. 35 Real GDP Growth in Central America (Real GDP, percent change) 6 5 4 3 2 1 0 Costa Rica El Salvador 2001 Guatemala 2002 2003 Honduras 2004 Copyright © 2003 Global Insight, Inc. Panama 2005 36 Global Insight’s Medium-Term Risk Ratings (Five-year risk aggregates) High score = high risk United States Canada Puerto Rico Costa Rica Panama Mexico Dominican Rep. 0 20 40 Financial Risk Copyright © 2003 Global Insight, Inc. 60 80 100 Business Risk 37 Global Insight’s Medium-Term Risk Ratings (Five-year risk aggregates) High score = high risk Chile Peru Colombia Ecuador Brazil Venezuela Argentina 0 20 40 Financial Risk Copyright © 2003 Global Insight, Inc. 60 80 100 Business Risk 38