Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Financial economics wikipedia , lookup

International monetary systems wikipedia , lookup

Interbank lending market wikipedia , lookup

Reserve currency wikipedia , lookup

Systemic risk wikipedia , lookup

Global financial system wikipedia , lookup

International status and usage of the euro wikipedia , lookup

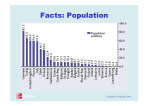

The Economics of European Integration © Baldwin & Wyplosz 2006 Chapter 19 The Financial Markets and the Euro © Baldwin & Wyplosz 2006 The Potential Role of the Euro Euro area EU USA 309 383 291 GDP (€ billion) 7.298 9.458 11.035 Stock market capitalization 2002 (€ billion) 3.000 4.900 8400 Currency used in foreign exchange transactions: average daily turnover, 2004 (% of total of $ 1,880 billion) € --------18.6% £ ------8.4% $ ------44.3% Population in 2003 (million) © Baldwin & Wyplosz 2006 Four Questions • What is special about financial markets? • What to expect from financial market integration? • Will financial markets change and grow after the Euro? • Will the euro become an international currency alongside the US dollar? © Baldwin & Wyplosz 2006 What Do Financial Markets Do? • Borrowing and lending, acting mostly as intermediaries: – lending is inherently risky – risk is to those who lend to financial institutions. © Baldwin & Wyplosz 2006 Examples of Financial Institutions • Banks: – take deposits, i.e. borrow – make loans. • Bond markets: – deal in standardized large-scale loans – allow borrowers and lenders to meet. • Stock markets: – deal in shares, i.e. titles to corporate ownership – allow borrowers and lenders to meet. • Collective funds: – intermediaries who collect funds from private savers. © Baldwin & Wyplosz 2006 Dealing with Risk • Every investor wants high returns and no risk. • But she is also willing to give up some return for less risk, or to take more risk for a better return: this is the basic trade-off. Risk adjusted return Risk.free rate © Baldwin & Wyplosz 2006 Markets Price Risk Markets price risk: the risk premium Asset’s risk-return characteristics adjust to meet investors’ willingness. Risk adjusted return Risk premium Risk.free rate © Baldwin & Wyplosz 2006 What Do Financial Markets Do About Risk? • Markets price risk: – asset’s risk-return characteristics adjust to meet investors’ willingness. • Markets reduce risk via diversification: – pooling toegether assets with negative risk correlation reduce overall risk – example: • asset R pays € 100 if it rains today • asset S pays € 100 if it does not rain today • markets can bundle R and S into one riskless asset that pays € 50 everyday. © Baldwin & Wyplosz 2006 What Makes Financial Markets Special • Scale economies: – matching needs of borrowers and lenders – diversification. • Scale economies lead to networks. • Risk and asymmetric information: – borrowers have incentives to conceal the risks that they may impose on lenders – lenders are aware and may: • overprice risk • refuse to lend. • Consequence: financial markets cannot operate freely, they must be regulated. © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Allocation efficiency © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Allocation efficiency Before © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Allocation efficiency Before After © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Allocation efficiency • Diversification • Competition • Economies of scale © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Allocation efficiency – Same returns from saving – Same borrowing costs – Capital goes where it is more productive – But not everyone gains © Baldwin & Wyplosz 2006 Winners and Losers • At home, before integration: © Baldwin & Wyplosz 2006 Winners and Losers • Home capital was scarce – Capital owners lose A © Baldwin & Wyplosz 2006 Winners and Losers • Home capital was scarce – Capital owners lose A – Labour gains A + B © Baldwin & Wyplosz 2006 Winners and Losers • Home capital was scarce – Capital owners lose A – Labour gains A + B – Home gains B © Baldwin & Wyplosz 2006 Winners and Losers • At home capital was scarce – Capital owners lose A – Labour gains A + B – Home gains B • Abroad capital was abundant – – – – Capital gains F Labour loses D+F Foreign loses D But they receive C+D from home – Total gain is C. © Baldwin & Wyplosz 2006 Winners and Losers • At home capital was scarce – Capital owners lose A – Labour gains A + B – Home gains B • Abroad capital was abundant – – – – Capital gains F Labour loses D+F Foreign loses D But they receive C+D from Home – Total gain is C © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Diversification – More choice to borrowers and lenders – Risk is reduced © Baldwin & Wyplosz 2006 Effects of Financial Market Integration • Competition should increase – Currencies act as non-tariff barriers – Rents from dominating position reduced or eliminated – Better service to customers • Scale economies better exploited – emergence of large institutions (banks, market exchanges) • Note that these two effects work in opposite directions © Baldwin & Wyplosz 2006 Implication for Banks: the Principles • In principle, banks should compete throughout the euro area. • In practice, many limits to this scenario: – good to be known by your banker (information asymmetry) – large costs of switching banks – importance of wide branch networks. © Baldwin & Wyplosz 2006 Implications for banks: facts • Number of banks in Euro area • Percent of crossborders mergers Luxembourg Ireland Netherlands Portugal Spain Berlgium Austria Greece Finland France Germany Italy Lots of mergers (scale economies) .... but mostly within countries Euro area 0 20 40 60 80 100 © Baldwin & Wyplosz 2006 Implication for Banks: So far... • Banks merge, but mostly within countries: – regulations remain local in spite of harmonization efforts – cultural differences – tax considerations. • Early effect: – more concentration and less competition. © Baldwin & Wyplosz 2006 Bank Concentration on the Rise Concentration in national banking Market share of five largest banks (%) 100 90 1997 80 2003 70 60 50 40 30 20 10 Finland Portugal Austria Netherlands Luxembourg Italy Ireland France Spain Greece Germany Denmark Belgium 0 © Baldwin & Wyplosz 2006 Implication for Banks: the Early Facts • Banks merge, but mostly within countries: – regulations remain local in spite of harmonisation efforts – cultural differences – tax considerations. • Early effect: – more concentration and less competition – merger is not the only possibility: banks could establish branches abroad: they don’t, really. © Baldwin & Wyplosz 2006 Little Change in Market Penetration Share of branches of foreign banks (% ) 1.60 1.40 1997 1.20 2001 1.00 0.80 0.60 0.40 0.20 U.K. Sweden Finland Portugal Austria Netherlands Italy France Spain Germany Belgium 0.00 © Baldwin & Wyplosz 2006 Implication for Bond Markets: the Principles • Bond markets deal in highly standardised loans. • They used to be segmented by currency risk: – risk of devaluation implies higher interest rates. • Gone currency risk, convergence has happened, and is nearly complete: – not fully complete, though – maybe the effect of national regulations. © Baldwin & Wyplosz 2006 Implication for Bond Markets: the Facts Short-term rates 13.00 Long-term rates Germany Greece Italy Spain Germany Italy United Kingdom 13.00 United Kingdom 11.00 Greece Spain 11.00 Euro launched 9.00 9.00 Euro launched 7.00 5.00 5.00 3.00 3.00 1.00 1995M1 Greece joins 7.00 Greece joins 1.00 1997M1 1999M1 2001M1 2003M1 2005M1 1995M1 1997M1 1999M1 2001M1 2003M1 2005M1 © Baldwin & Wyplosz 2006 Implication for Stock Markets: the Principles • Worldwide stock markets have remained surprisingly national (home bias): – information asymmetries – currency risk. • With the single currency, euro area stock markets should be less subject to home bias. © Baldwin & Wyplosz 2006 Implication for Stock Markets: the Facts • Some increase in the use of the euro in world portfolios. © Baldwin & Wyplosz 2006 Implication for Stock Markets: the Facts • Some increase in the use of the euro in world portfolios, nothing dramatic yet. • Mergers of exchanges: – Euronext (Amsterdam + Brussels + Paris) – failed attempt between London, Frankfurt and Stockholm. • Overall, European markets remain small relatively to the US. © Baldwin & Wyplosz 2006 Overall, European markets remain small relatively to the US. Exchange New York Tokyo London Euronext Frankfurt Madrid Zurich € bn 10,729 2,850 2,284 1,910 936 769 667 € bn % GDP 112.7 76.5 131.3 78.0 42.1 91.8 221.5 OMX Milano Oslo Athens Vienna Dublin Warsaw 593 592 134 100 93 89 57 € bn % GDP 90.6 42.0 58.9 57.5 37.9 55.7 25.7 Luxembourg Budapest Prague Cyprus Bratislava Malta 40 26 25 4 4 2 % GDP 145.3 28.8 27.4 35.7 11.3 56.7 © Baldwin & Wyplosz 2006 Loose Ends: Regulation and Supervision • A single financial market would seem to require a single regulator and a single supervisor. • Instead, the chosen route has been to: – harmonise and recognise each other’s regulation – foster cooperation among supervisors. • This can be a cause of inefficiencies: – rampant protectionsim – inadequate information in case of crisis. © Baldwin & Wyplosz 2006 The International Role of the Euro • 19th century: the pound Sterling. • 20th century: the US dollar. • 21th century: the euro? © Baldwin & Wyplosz 2006 The International Role of the Euro • As it is internally, a currency can be: – an international unit of account: trade invoicing – an international medium of exchange: a vehicle currency – an international store of value: foreign exchange reserves, individual hoarding. • Internally, these functions are established by law. • Externally, they have to be earned. © Baldwin & Wyplosz 2006 Trade Invoicing • Small changes so far. • The dollar remains the currency of choice in international trade and for pricing commodities (oil, wheat, etc.). Share of exports invoiced in euros 70 60 50 40 30 20 10 2002 Spain Portugal Italy 2003 Luxembourg 2001 Greece Germany France Belgium 0 © Baldwin & Wyplosz 2006 Vehicle Currency: Exchange Markets • Currencies are used on exchange markets: – directly for conversion into/from other currencies – indirectly as intermeadiary for other bilateral conversions. • Realtive to its constitutent currencies, the euro’s overall share on world exchange markets has declined following the disappearance of within-EU conversions. © Baldwin & Wyplosz 2006 Vehicle Currency: Bond Markets • The share of the euro in international bond issues has risen. © Baldwin & Wyplosz 2006 Currency Shares of International Bonds © Baldwin & Wyplosz 2006 Vehicle Currency: International Reserves • The euro remains a small part of international reserves of central banks. 90 80 70 60 50 40 30 20 10 0 1965 1969 1973 1977 1981 1985 1989 1993 U.S. dollar Japanese yen Deutsche mark ECUs 1997 2001 Euro © Baldwin & Wyplosz 2006 Vehicle Currency: International Reserves • The euro remains a small part of international reserves of central banks. • The euro is used as anchor currency by 35 countries, mostly succeeding its constituent currencies. © Baldwin & Wyplosz 2006 Parallel Currency • In troubled countries, foreign currencies circulate alongside the national currency. • The dollar has long dominated. • The euro takes up the role of the DM and the French franc in areas close to the EU and Africa. • Overall, the ECB has shipped abroad 8 per cent of its initial production of euros, more has leaked. © Baldwin & Wyplosz 2006 Does it Matter? • Trade invoicing in euro reduces currency risk for euro area exporters. • Large financial markets are more efficient. • Seigniorage is small. • Some cherish the symbol. • The ECB has taken a hands-off attitude. © Baldwin & Wyplosz 2006