Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

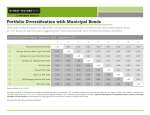

MARKETVIEW MuniBonds:OfftoaGoodStartin2017 January30,2017 2317Views Followingachallengingfourthquarterin2016,muniperformanceandmutual fundflowshavebeenimproving. Inmid-December2016,MarketViewf ocusedontheslumpinthemunicipalbondmarketinthef inal monthsof theyear.Atthattime,acombinationof headwinds—concernsaboutthepotentialf or higherinterestratesandchangestotaxpolicyunderthenewadministration—hadledto substantialoutf lowsf romtax-f reemutualf undsandputpressureonmunicipalbondprices, resultinginlossesf ormunicipalbondsinthef ourthquarter.Whathashappenedsince? Municipalbondf undscontinuedtoseeadditionaloutf lowsinthef inalweeksof theyear.According toMorningstar,tax-f reebondf undsexperienced$17.5billionof outf lowsinthemonthof Decemberalone,f oratotalof $28billionoverthetwo-monthperiodf ollowingtheelection. However,thepaceof outf lowslikelywasaf f ectedbyseasonalf actors,suchasyear-endtax-loss trading.“Withbondpricesdroppingandstockpricesrisingaf tertheelectioninNovember,many thoughtthatitwasbenef icialtorecognizebondlossesinordertoof f setcapitalgainsonstocks,” saidDanielSolender,LordAbbettpartneranddirectorof municipalbondstrategies.“Withmutual f unds,investorsneededtoselltheirsharestoachievethisobjective,”Solendercontinued, “althoughmanyof thesaleswereactuallyexchangestootherf undsratherthanoutright redemptionsbecauseinvestorswantedtoremaininthemarket.” Asweturnedthepagetoanewyear,thef lowsituationhasstabilized,andhasbeenpositiveover thepastthreeweeks.(AccordingtoLipper,weeklyreportingf undshadnetinf lowsof $974million, $512million,and$7million,respectively,ineachof thepastthreeweeks.) Whataboutperf ormance?Despitetheheadwindsof largemutualf undoutf lows,municipals(as measuredbytheBloombergBarclaysMunicipalBondIndex)postedpositivereturnsinDecember, generatingareturnof 1.2%,wellaheadof the0.1%returnof thebroadtaxablebondmarket(as representedbytheBloombergBarclaysAggregateBondIndex).Thistrendhascontinuedinthe f irstf ewweeksof 2017,withmunicipalsinpositiveterritory,whiletaxablebondsaremodestly negative.AsillustratedinTable1,thebroadmunicipalmarkethasgeneratedareturnof 2.0% sinceDecember1,ledhigherbylonger-maturityandlower-ratedmunicipals—thoseareasthat suf f eredthemostinthef ourth-quarterpullback. Table1:MunicipalBondPerformanceBegan2017onaPositiveNote Returnsyeartodate(January25,2017) 1 Source:BloombergandThomsonReutersMunicipalMarketData.Broadtaxablef ixedincomerepresentedbythe BloombergBarclaysU.S.AggregateBondIndex.Municipalbondsrepresentedbymaturity-specif icsubsetsof the BloombergBarclaysMunicipalBondIndex.High-yieldmunicipalbondsarerepresentedbytheBloombergBarclaysHigh YieldMunicipalBondIndex. Pastperformanceisnoguaranteeoffutureresults.Forillustrativepurposesonlyanddoesnotrepresentthe perf ormanceof anyspecif icportf oliomanagedbyLordAbbettoranyparticularinvestment.Lower-ratedbondsmay carrygreaterrisksthanhigher-ratedbonds.Incomef rommunicipalbondsmaybesubjecttothealternativeminimum tax.Federal,state,andlocaltaxesmayapply.Indexesareunmanaged,donotref lectthedeductionof f eesand expenses,andarenotavailablef ordirectinvestment. Whataboutgoingf orward?Weposeaf ewquestionsandanswers: Whatwillhappenwithinterestrates?Aswehavehighlightedmanytimes,accurately predictingthedirectionof interestrateshistoricallyhasbeenverydif f iculttodo.Manyhave anticipatedhigherratesf ormostof thepasteightyears,onlytobedisappointedthusf ar.Yes,it wouldseemreasonablethatratesmaybeheadinghigherf romhere(sincethehikeonDecember 14),butthepaceandmagnitudeof thatmoveisveryuncertain.Andyieldshavealreadymoved higher,withthe10-yearU.S.Treasurybondyieldrisingbynearly120basispoints(bps)sinceJuly. Whatwillhappentothefederaltaxcode?Investorsareconcernedthatchangestothetax codemayreducethetaxable-equivalentyieldonmunicipalbonds,and,consequently,maketaxf reebondslessappealing.Changesintaxbracketsandstatementsaboutalteringthetax-exempt statusof municipalsaretopicsthathavesurroundedthemunimarketf ordecades.Butaswe pointedoutinDecember,historyshowsthatthishasnothadanimpactonthemarket.According totheCitiResearchreportwecited,thetopmarginaltaxratesf ormunicipalbondsf luctuatedin therangeof 28–70%between1980andDecember2016.Butthereportf oundnocorrelation betweenmunicipalyieldsandthetopmarginaltaxrate.Thisislikelybecausetheaveragetaxrate f ormunicipalbondholdershasremainedsteady,ataround25%,duringtheperiod surveyed.[Resultsmayhavedifferedduringdifferentintervalsinthesurveyperiod.] Whataboutmutualfundflows?AswealsopointedoutinDecember,thisisnotthef irsttime wehaveseenlargeoutf lowsf romtax-f reemutualf unds.Thesupply/demandimbalancemayhave anegativeimpactonshort-termperf ormance,aswejustwitnessed.Butif weweretolookover longertimeperiods,thef undamentalstypicallywinoutovertechnicalf actors.Further,if wewere tolookbackoverthepastsevenyears—aperiodthatcoincidedwithmultipleperiodsof largef und outf lows—therepresentativeBloombergBarclaysMunicipalBondIndexoutperf ormedthetaxable BloombergBarclaysAggregateIndex,andthatperf ormanceincludedthesharppullback municipalsexperiencedinthef ourthquarterof 2016.Thesereturns,however,donottakeinto accountthetax-exemptincomethatmunicipalshaveprovided,andsoactuallyunderstatethe outperf ormancethatmunicipalshavedelivered.Thevolatilityinmutualf undf lowsseemsto suggestthatsomeinvestorstakeatacticalapproachtoallocatingtomunicipals,butthe perf ormancerecordshowstheywouldhavebeenmuchbetterof f maintaininganallocationthrough 2 thecycle. Table2:Historically,MaintainingaMuniBondAllocationLongerTermHasBeen Beneficial ReturnsasofDecember31,2016 Source:BloombergandThomsonReutersMunicipalMarketData.Broadtaxablef ixedincomerepresentedbythe BloombergBarclaysU.S.AggregateBondIndex.Municipalbondsrepresentedbymaturity-specif icsubsetsof the BloombergBarclaysMunicipalBondIndex.High-yieldmunicipalbondsarerepresentedbytheBloombergBarclaysHigh YieldMunicipalBondIndex. Pastperformanceisnoguaranteeoffutureresults.Forillustrativepurposesonlyanddoesnotrepresentthe perf ormanceof anyspecif icportf oliomanagedbyLordAbbettoranyparticularinvestment.Lower-ratedbondsmay carrygreaterrisksthanhigher-ratedbonds.Incomef rommunicipalbondsmaybesubjecttothealternativeminimum tax.Federal,state,andlocaltaxesmayapply.Indexesareunmanaged,donotref lectthedeductionof f eesand expenses,andarenotavailablef ordirectinvestment. Thereismuchuncertaintyaboutseveralf actorsthatmayaf f ectthemarket.Butaf ewthingsare veryclear: Relativevalueismoreattractive.Theratioof‘AAA’ratedmunicipalbondsto comparablematurityU.S.Treasurybondsisthemostcommonmeasureofrelativevalue fortax-freebonds.AccordingtoMunicipalMarketData,themuni/Treasuryratiofor10yearand30-yearmunicipalbondshasrisen,toapproximately95%and100%,respectively, ascomparedtoapproximately85%ofTreasuriesinAugust2016. Investment-gradecreditspreadsarewider.Theadditionalyieldprovidedinsingle‘A’ and‘BBB’ratedmunicipalsover‘AAA’ratedbondshasrisen.Forexample,accordingto theBloombergBarclaysMunicipalIndex,‘BBB’ratedbondsnowofferayieldadvantageof 165bpsover‘AAA’ratedbonds,40bpshigherthanthelevelsseeninAugust. Yieldshaveadjustedhigher—fornow.ThecombinationofhigherU.S.Treasuryyields, moreattractiverelativevalue,andwidercreditspreadshasresultedinhighertax-free yields,especiallyamongsingle‘A’and‘BBB’ratedbonds.Chart1illustratesthismovein 10-yearmaturitybonds,whichnowofferyieldsthatare100–160bpshigherthanwhatwas availableinAugust. 3 Chart1.MunicipalYieldsHaveAdjustedHigherSinceAugust2016 10-yearyields(asofJanuary25,2017) Source:BloombergandThomsonReutersMunicipalMarketData.Duetomarketvolatility,themarketmaynotperf orm inasimilarmannerinthef uture. Pastperformanceisnoguaranteeoffutureresults.Forillustrativepurposesonlyanddoesnotrepresentthe perf ormanceof anyspecif icportf oliomanagedbyLordAbbettoranyparticularinvestment.Lower-ratedbondsmay carrygreaterrisksthanhigher-ratedbonds.Incomef rommunicipalbondsmaybesubjecttothealternativeminimum tax.Federal,state,andlocaltaxesmayapply.Indexesareunmanaged,donotref lectthedeductionof f eesand expenses,andarenotavailablef ordirectinvestment. Overthelongterm,municipalshaveprovidedattractiverisk-adjustedreturns versusU.S.Treasuries.Overthepast20years,10-yearmunibonds(asrepresentedby theBloombergBarclaysMunicipalBond10-YearIndex)hasgeneratedsimilartotalreturns to10-yearTreasurybonds(asrepresentedbytheCitigroup10-YearTreasuryBondIndex), buthasdonesowithabout40%lowervolatility.(SeeChart2.)Thatwouldhavetranslated tohigherrisk-adjustedreturns,evenina0%taxbracket. Chart2:Historically,MunisHaveProvidedVeryAttractiveRisk-RewardOvertheLong Term Trailing20years:January1,1997–December31,2016 4 Source:MorningstarDirect. Pastperformanceisnoguaranteeoffutureresults.Forillustrativepurposesonlyanddoesnotrepresentany specif icportf oliomanagedbyLordAbbettoranyparticularinvestment.Incomef rommunicipalbondsmaybesubject tothealternativeminimumtax.Federal,state,andlocaltaxesmayapply.Indexesareunmanaged,donotref lectthe deductionof f eesorexpenses,andarenotavailablef ordirectinvestment. Themarketisf ullof uncertainty,butgiventhelong-termreturnprof ile,thehigheryields,andmore attractiverelativevalueavailableinthemarkettoday,investorsmaywanttotakeanotherlookat allocatingtotax-f reebonds. Thereisnoguaranteethatmarketswillperf orminasimilarmannerundersimilarconditionsinthef uture. ANoteaboutRisk:Thevalueof aninvestmentinf ixed-incomesecuritieswillchangeasinterestratesf luctuateand inresponsetomarketmovements.Asinterestratesf all,thepricesof debtsecuritiestendtorise.Asratesrise,prices tendtof all.Investinginthebondmarketissubjecttorisks,includingmarket,interestrate,issuer,credit,inf lationrisk, andliquidityrisk.Themunicipalbondmarketmaybeimpactedbyunf avorablelegislativeorpoliticaldevelopmentsand adversechangesinthef inancialconditionsof stateandmunicipalissuersorthef ederalgovernmentincaseit providesf inancialsupporttothemunicipality.Incomef romthemunicipalbondsheldcouldbedeclaredtaxablebecause of changesintaxlaws.Certainsectorsof themunicipalbondmarkethavespecialrisksthatcanaf f ectthemmore signif icantlythanthemarketasawhole.Becausemanymunicipalinstrumentsareissuedtof inancesimilarprojects, conditionsintheseindustriescansignif icantlyaf f ectaninvestment.Incomef rommunicipalbondsmaybesubjectto thealternativeminimumtax.Federal,stateandlocaltaxesmayapply.InvestmentsinPuertoRicoandotherU.S. territories,commonwealths,andpossessionsmaybeaf f ectedbylocal,state,andregionalf actors.Thesemay include,f orexample,economicorpoliticaldevelopments,erosionof thetaxbase,andthepossibilityof credit problems. 5 ThisMarketViewmaycontainassumptionsthatare“f orward-lookingstatements,”whicharebasedoncertain assumptionsof f utureevents.Actualeventsaredif f iculttopredictandmaydif f erf romthoseassumed.Therecanbe noassurancethatf orward-lookingstatementswillmaterializeorthatactualreturnsorresultswillnotbematerially dif f erentf romthosedescribedhere. Thismaterialisprovidedf orgeneralandeducationalpurposesonly.Theexamplesprovidedarehypothetical,aref or illustrativepurposesonly,andarenotindicativeof anyparticularinvestorsituation. Abasispointisoneone-hundredthof apercentagepoint. Spreadisthedif f erenceinyieldbetweentwodif f erentinvestments. Usedasameasureof volatility,standarddeviationisaquantitycalculatedtoindicatetheextentof deviationf ora groupasawhole. Standarddeviationisameasureof thedispersionof asetof dataf romitsmean.If thedatapointsaref urtherf rom themean,thereishigherdeviationwithinthedataset.Yieldistheannualinterestreceivedf romabondandis typicallyexpressedasapercentageof thebond'smarketprice.Tax-equivalentyieldisthepretaxyieldthatataxable bondneedstopossessf oritsyieldtobeequaltothatof atax-f reemunicipalbond.Thiscalculationcanbeusedto f airlycomparetheyieldof atax-f reebondtothatof ataxablebondinordertoseewhichbondhasahigherapplicable yield. TheBloombergBarclaysMunicipalBondIndexisarules-based,market-value-weightedindexengineeredf orthe long-termtax-exemptbondmarket.Theindexisabroadmeasureof themunicipalbondmarketwithmaturitiesof at leastoneyear.Tobeincludedintheindex,bondsmustberatedinvestment-grade(Baa3/BBB-orhigher)byatleast twoof thef ollowingratingsagencies:Moody's,Standard&Poor's,Fitch.If onlytwoof thethreeagenciesratethe security,thelowerratingisusedtodetermineindexeligibility.If onlyoneof thethreeagenciesratesasecurity,the ratingmustbeinvestment-grade.Bondsmusthaveanoutstandingparvalueof atleast$7millionandbeissuedas partof atransactionof atleast$75million.Thebondsmustbef ixedrate,haveadated-dateaf terDecember31, 1990,andmustbeatleastoneyearf romtheirmaturitydate.TheBloombergBarclaysMunicipalBond10-Year Indexisamaturity-specif iccomponentof theMunicipalBondindex. TheBloombergBarclaysU.S.AggregateBondIndexrepresentssecuritiesthatareSEC-registered,taxable,and dollardenominated.TheindexcoverstheU.S.investmentgradef ixedratebondmarket,withindexcomponentsf or governmentandcorporatesecurities,mortgagepass-throughsecurities,andasset-backedsecurities.Totalreturn comprisespriceappreciation/depreciationandincomeasapercentageof theoriginalinvestment. TheBloombergBarclaysHighYieldMunicipalBondIndexisanunmanagedindexconsistingof noninvestmentgrade,unratedorbelowBa1bonds. TheCitigroup10YearTreasuryBondIndexisabroadmeasureof theperf ormanceof themedium-termU.S. Treasurysecurities. Indexesareunmanaged,donotref lectthedeductionof f eesorexpenses,andarenotavailablef ordirectinvestment. Thecreditqualityof thesecuritiesinaportf olioisassignedbyanationallyrecognizedstatisticalratingorganization (NRSRO),suchasStandard&Poor’s,Moody’s,orFitch,asanindicationof anissuer’screditworthiness.Ratings rangef rom‘AAA’(highest)to‘D’(lowest).Bondsrated‘BBB’oraboveareconsideredinvestmentgrade.Creditratings ‘BB’andbelowarelower-ratedsecurities(junkbonds).High-yielding,non-investment-gradebonds(junkbonds)involve higherrisksthaninvestmentgradebonds.Adverseconditionsmayaf f ecttheissuer’sabilitytopayinterestand principalonthesesecurities. 6 TheopinionsinMarketViewareasof thedateof publication,aresubjecttochangebasedonsubsequent developments,andmaynotref lecttheviewsof thef irmasawhole.Thematerialisnotintendedtoberelieduponas af orecast,research,orinvestmentadvice,isnotarecommendationorof f ertobuyorsellanysecuritiesortoadopt anyinvestmentstrategy,andisnotintendedtopredictordepicttheperf ormanceof anyinvestment.Readersshould notassumethatinvestmentsincompanies,securities,sectors,and/ormarketsdescribedwereorwillbeprof itable. Investinginvolvesrisk,includingpossiblelossof principal.Thisdocumentispreparedbasedontheinf ormationLord Abbettdeemsreliable;however,LordAbbettdoesnotwarranttheaccuracyandcompletenessof theinf ormation. Investorsshouldconsultwithaf inancialadvisorpriortomakinganinvestmentdecision. Investorsshouldcarefullyconsidertheinvestmentobjectives,risks,chargesandexpensesof theLordAbbettFunds.Thisandotherimportantinformationiscontainedinthefund's summaryprospectusand/orprospectus.Toobtainaprospectusorsummaryprospectusonany LordAbbettmutualfund,youcanclickhereorcontactyourinvestmentprofessionalorLord AbbettDistributorLLCat888-522-2388.Readtheprospectuscarefullybeforeyouinvestor sendmoney. NotFDIC-Insured.Maylosevalue.Notguaranteedbyanybank.Copyright©2017Lord,Abbett& Co.LLC.Allrightsreserved.LordAbbettmutualfundsaredistributedbyLordAbbett DistributorLLC.ForU.S.residentsonly. Theinformationprovidedisnotdirectedatanyinvestororcategoryofinvestorsandis providedsolelyasgeneralinformationaboutLordAbbett’sproductsandservicesandto otherwiseprovidegeneralinvestmenteducation.Noneoftheinformationprovidedshouldbe regardedasasuggestiontoengageinorrefrainfromanyinvestment-relatedcourseofaction asneitherLordAbbettnoritsaffiliatesareundertakingtoprovideimpartialinvestmentadvice, actasanimpartialadviser,orgiveadviceinafiduciarycapacity.Ifyouareanindividual retirementinvestor,contactyourfinancialadvisororotherfiduciaryaboutwhetheranygiven investmentidea,strategy,productorservicemaybeappropriateforyourcircumstances. 7