Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

History of the Federal Reserve System wikipedia , lookup

Private equity wikipedia , lookup

Financial economics wikipedia , lookup

Investment fund wikipedia , lookup

Monetary policy wikipedia , lookup

Inflation targeting wikipedia , lookup

Interest rate wikipedia , lookup

Investment management wikipedia , lookup

Private equity in the 1980s wikipedia , lookup

Interbank lending market wikipedia , lookup

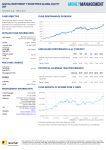

Quarterly Investment Briefing November 12, 2015 Clayton T. Bill, CFA Stephen J. Nilles, CFP Capital Market Returns Current & Annualized Period Ending September 30, 2015 U.S. Equities Non-U.S. Equities Emerging Market Equities Fixed Income Real Estate 15 13.3 12.5 10 Rate of Return % 5 2.9 2.7 1.1 1.2 7.5 6.2 5.1 3.8 1.7 3.1 6.9 4.8 4.6 4.7 3.3 0 -0.5 -1.6 -5 -10 -5.5 -6.3 -7.3 -4.8 -9.5 -10.3 -15 -20 -2.9 -4.1 -15.0 -19.1 -18.1 -25 3Q 2015 YTD Source: Russell, Barclays, Bloomberg and FTSE NAREIT 1-YR 3-YR 5-YR 10-YR 2 Market Volatility and Pullbacks in Historical Context Number of 5% drawdowns experienced each year Source: Standard & Poor’s, FactSet, J.P. Morgan Asset Management 3 U.S. Equity Rebound Surprises Market Timers Source: Russell 4 Corporate Earnings: Set to Improve? Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management 5 Benign Inflation Helps U.S. Equity Valuations Low but positive levels of inflation help support higher than average equity valuations, as these environments are typically accompanied by low interest rates. The Federal Reserve has attempted to utilize monetary policy to generate inflation towards its target of about 2% with mixed results. Source: Strategas, 6 Non-U.S. Valuations Fall, Become More Attractive Developed and emerging-market equities experienced multiple compression in Q3 due to weak equity performance. Valuations of most developed and emerging markets remained lower than U.S. multiples and fell further below long-term averages. Source: Fidelity 7 First Fed Rate Hike Not Typically the Start of a Downturn Historically, the first interest-rate hike in a Federal Reserve tightening cycle occurs during the mid-cycle phase, is a sign that the economic expansion is strengthening, and rarely presages an abrupt move into the late-cycle phase. Typically, economically sensitive assets such as equities have performed well in the period immediately after the initial hike. Source: Fidelity 8 Domestic European Recovery Outweighs Foreign Drag As evidenced by continued improvements in economic sentiment, Europe’s domestic recovery continues amid supportive monetary policy and pent-up demand. Exports are more important for the euro-area countries than the U.S., but the majority of those exports go to other European economies, with a relatively small share destined for China. Source: Fidelity 9 China is Slowing, not Collapsing Important Driver of World Growth Source: Russell 10 Emerging Markets Have Rebounded From Past 20% Pullbacks Source: Russell 11 Turning Stock Volatility Into Tax Assets Source: Russell 12 Consider Investment Decisions Based on Probabilities – Not Possibilities Source: Russell 13