Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

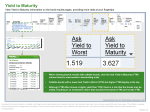

JC Clark Yield Trust 2012 Year End Update January 22, 2013 Dear Investors: Heading into 2012, the goal for the JC Clark Yield Trust (“the Fund”) was to generate a 4-5% net return to clients. We are happy to report to you that we accomplished this goal by generating a 5.8% return. Entering 2012, we had indicated that based on our macro view, we wanted to keep the fund at the short end of the duration spectrum. During the year we stayed true to this view by maintaining duration at less than 5 years (11 out of 12 months duration was less than 4 years). During the year there were two key themes that we followed and continue to focus on – global currency debasement and the potential for fixed income outflows. As part of the first theme, we wrote a piece called “A Cup of Coffee”, where we showed how a 1964 dime would have purchased a Tim Horton’s cup of coffee in 1964 and that 48 years later, based on its silver content, would still purchase that same cup of coffee today. That 1964 dime weighs 2.33 grams and contains 80% silver and 20% copper, with the intrinsic metal value worth approximately $1.90. A 2012 minted dime weighs 1.75 grams, contains 92% steel, 5.5% copper and 2.5% nickel, and is intrinsically worth less than 10 cents. Our conclusion was that monetary debasement will eventually lead to rising interest rates, which would be a major headwind for fixed income investors. To help combat this challenge, we have begun to identify bond opportunities that would benefit from a rising precious metals environment. As of the end of the year, we had approximately 5.5% of the Fund invested in precious metals related securities. Relating to the second theme, over the past number of years there have been considerable inflows into the fixed income space which have come at the direct expense of equity funds. For the first 11 months of 2012, $23.8 billion of capital flowed into Canadian Fixed Income and High Yield mutual funds, while $15.5 billion of capital has moved out of Canadian Equity, International Equity and Money Market mutual funds. At some point, this trend will reverse and investors will sell their fixed income funds to invest back into equity funds. When this happens, 1 it could put tremendous selling pressure on bonds, as fixed income managers sell bond positions to fund redemptions. Our solution to this is to focus on bonds that have a short maturity with the thinking that they will be less exposed to capital losses in the event that bond managers become net sellers. Looking Forward to 2013 Last year was an incredible year for Investment Grade and High Yield corporate bonds. Investment Grade bonds had their second best performance over the past 10 years, generating a total return of 11.8% (based on iShares Investment Grade Corporate Bond ETF). Equally as impressive were High Yield bonds, which generated a total return of 14.1% (based on the iShares High Yield Corporate Bond ETF). With Canadian and US 10 & 30 Year government rates at less than 2% and 3%, respectively, coupled with the dramatic returns in Investment Grade and High Yield, we believe that 2013 and beyond will provide significantly lower total returns for fixed income investors. Yield Trust Positioning At the end of 2012, the Fund was invested in 4.9% Cash & T-Bills, 54.7% Corporate Bonds and 40.4% Convertibles/Debentures/Preferred Shares. On a Yield-to-Maturity (“YTM”) basis, the duration of the Fund was approximately 3.1 years and the gross yield was approximately 5.4%. On a Yield-to-Worst (“YTW”) basis, the duration of the Fund was approximately 2.1 years and the gross yield was approximately 3.7%. The Fund had 10.3% of its assets invested in securities that come due in less than 1 year, 66% in securities that come due within 1-5 years, 20.5% in securities that come due in 5-10 years and 3.2% in securities that come due in greater than 10 years. Our top 10 issuer names consisted of Mega Brands, The Brick, Clearwater Seafoods, Harvest Energy, Ford Credit Canada, Fairfax Financial, Videotron/Quebecor, Superior Plus, Boyd Group and FirstService. Fixed Income Ideas Our largest fixed income position in the Fund is Mega Brands 10% of 2015 Debentures. We have written and talked extensively about this bond in the past but it continues to offer a compelling risk-to-reward ratio. The bond comes due on March 30, 2015, which coincides with the expiration of warrants, which were issued during the Company’s recapitalization. The warrants are exercisable at $9.94/share; with the stock trading above $10/share, we believe there is a strong likelihood they will be exercised and the cash proceeds used to redeem the bond. In this scenario, we believe we are effectively earning a 5%+ YTM lending against cash (assuming the warrants are exercised). The major risk is that with the bond trading north of $106, the Company could call the bond at $105 under a refinancing event. Our second largest bond position is The Brick 12% of 2014 Debentures, which we highlighted during our mid-year letter. In early November, The Brick received a buyout offer from Leon’s Furniture, which will further consolidate the Canadian retail furniture industry. In the bond 2 agreement there is a provision which requires The Brick to make an offer to bondholders at $110 in the event of a change of control. Initially we thought we would be tendering these bonds into the $110 offer, but subsequent due diligence of the transaction makes us comfortable holding this bond until maturity. Proforma Debt/EBITDA is projected to increase to 2.4x which we believe is manageable; we would still be earning a 4%+ YTM for a bond that comes due in early 2014. If and when the Competition Bureau approves the deal, we will be in a better position to determine if we want to hold the bond or tender into the $110 offer. Our third largest position is Clearwater Seafoods 7.25% of 2014 Debentures. The bond comes due in less than 2 years and we are earning a 6.7% YTM. During our mid-year letter we highlighted three reasons why we were excited about the credit – significant EBITDA growth potential, successful balance sheet refinancing and a TriNav Fisheries study highlighting their significant asset value. Over the past 6 months, this thesis has played out with strong EBITDA growth and the news that one of the controlling shareholders had purchased 11% of the Company, bringing the control group ownership stake to 69.1%. The debentures are convertible at $5.90/share and with the stock up 80%+ over the past 6 months to $4.90/share, the bond has appreciated as a conversion becomes a higher probability event. The major risk with the credit is that the Company has the right to repurchase the bonds at $100, and with the bond trading north of $102, we have used this opportunity to begin reducing the position. Summary With the view that rising interest rates, potential fixed income outflows and tight corporate credit spreads pose significant headwinds for fixed income investors, we believe that return expectations need to be moderated going forward. We will continue to look for attractive fixed income corporate securities within North America but believe it is essential to carefully manage the aforementioned risks and maintain a conservative portfolio posture. Please do not hesitate to call me if there are any questions about the JC Clark Yield Trust. I can be reached at 416-361-6461 or email at [email protected]. Sincerely, John Dynes, CFA, CMT 3