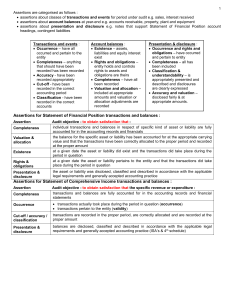

Aue2602 Summary

... debtors have been reflected at appropriate carrying value i.e. suitable allowance has been made for recovery of nonrecoverable debts (valuation) and bank balances are carried at their correct value (valuation) Presentation and disclosure : In addition to above also that presentation and disclosu ...

... debtors have been reflected at appropriate carrying value i.e. suitable allowance has been made for recovery of nonrecoverable debts (valuation) and bank balances are carried at their correct value (valuation) Presentation and disclosure : In addition to above also that presentation and disclosu ...

1 THE SUPREME COURT OF APPEAL OF SOUTH AFRICA

... and payments made to the point where the funds were depleted. I do not however consider it necessary to deal with all of them. (d) The investigation also uncovered discrepancies in the firm’s bank reconciliation. It was discovered that cashbook balances were substantially in excess of the bank state ...

... and payments made to the point where the funds were depleted. I do not however consider it necessary to deal with all of them. (d) The investigation also uncovered discrepancies in the firm’s bank reconciliation. It was discovered that cashbook balances were substantially in excess of the bank state ...

a) Purposes of internal controls

... The following information is available to reconcile Gucci’s book balance of cash with its bank statement cash balance as of December 31. Prepare the bank reconciliation for this company as of December 31. a. The December 31 cash balance according to the accounting records is $1,610, and the bank sta ...

... The following information is available to reconcile Gucci’s book balance of cash with its bank statement cash balance as of December 31. Prepare the bank reconciliation for this company as of December 31. a. The December 31 cash balance according to the accounting records is $1,610, and the bank sta ...

theme: cash flow - Real Life Accounting

... Depreciation or Amortization expense immediately because that’s easy. Next, adjust for any accruals such as Accounts Receivable, Accounts Payable, or Payroll Taxes Payable. If you happen to have any gains or losses from the disposition of assets, then add back the losses or subtract the gains. Once ...

... Depreciation or Amortization expense immediately because that’s easy. Next, adjust for any accruals such as Accounts Receivable, Accounts Payable, or Payroll Taxes Payable. If you happen to have any gains or losses from the disposition of assets, then add back the losses or subtract the gains. Once ...

This PDF is a selection from a published volume from... National Bureau of Economic Research

... stock-flow consistency on the system as well. This is very important for analyzing and understanding the economic process. This feature is key to ensuring that many of the types of analyses outlined in table 2.1 provide consistent results such as multifactor productivity analysis, which relates the ...

... stock-flow consistency on the system as well. This is very important for analyzing and understanding the economic process. This feature is key to ensuring that many of the types of analyses outlined in table 2.1 provide consistent results such as multifactor productivity analysis, which relates the ...

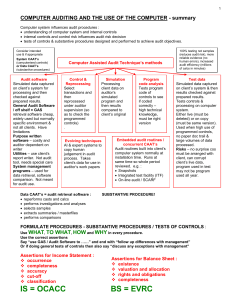

the relevance of auditing in a computerized accounting system

... your attention to customers that are delinquent, and produces dunning notices. It allows you to have daily cash control. You get out the bills on time, yet you avoid errors such as billing a customer twice for the same time. The further advantage is that debits and credits are posted automatically t ...

... your attention to customers that are delinquent, and produces dunning notices. It allows you to have daily cash control. You get out the bills on time, yet you avoid errors such as billing a customer twice for the same time. The further advantage is that debits and credits are posted automatically t ...

LO 2 - Wiley

... it cannot pay at the present time. If Wolder Co. does expect eventual collection, it would make the following entry at the time the note is dishonored (assuming no previous accrual of interest). Nov. 1 ...

... it cannot pay at the present time. If Wolder Co. does expect eventual collection, it would make the following entry at the time the note is dishonored (assuming no previous accrual of interest). Nov. 1 ...

Financial Accounting and Accounting Standards

... accounting period in which it is earned. b. Companies should match expenses with revenues. c. The economic life of a business can be divided into artificial time periods. d. The fiscal year should correspond with the calendar ...

... accounting period in which it is earned. b. Companies should match expenses with revenues. c. The economic life of a business can be divided into artificial time periods. d. The fiscal year should correspond with the calendar ...

FREE Sample Here - Find the cheapest test bank for your

... 4. The assets for the balance sheet must equal the liabilities and stockholders’ equity. ANS: T 5. The retained earnings account is the link between the balance sheet and the statement of cash flows. ANS: F 6. A summary annual report is a condensed annual report that omits much of the financial info ...

... 4. The assets for the balance sheet must equal the liabilities and stockholders’ equity. ANS: T 5. The retained earnings account is the link between the balance sheet and the statement of cash flows. ANS: F 6. A summary annual report is a condensed annual report that omits much of the financial info ...

Financial Accounting and Accounting Standards

... designers who frequently traveled together came up with a fraud scheme: They submitted claims for the same expenses. For example, if they had a meal together that cost $200, one person submitted the detailed meal bill, another submitted the credit card receipt, and a third submitted a monthly credit ...

... designers who frequently traveled together came up with a fraud scheme: They submitted claims for the same expenses. For example, if they had a meal together that cost $200, one person submitted the detailed meal bill, another submitted the credit card receipt, and a third submitted a monthly credit ...

Chapter Twelve - Dr.Mahmood Asad

... • Learning about accounting is extremely important because as a businessperson you will constantly be dealing in numbers. Thus, some basic information on how businesspeople can use accounting to better understand and control their businesses will be discussed. ...

... • Learning about accounting is extremely important because as a businessperson you will constantly be dealing in numbers. Thus, some basic information on how businesspeople can use accounting to better understand and control their businesses will be discussed. ...

LO 5 - Test Banks Shop

... Students have a difficult time understanding the concept of equity. Have students think about their equity in their assets. If they purchased a car for $10,000 and took out a $3,000 loan, what is their equity in the car? Put this transaction into the accounting equation to see that the left side rep ...

... Students have a difficult time understanding the concept of equity. Have students think about their equity in their assets. If they purchased a car for $10,000 and took out a $3,000 loan, what is their equity in the car? Put this transaction into the accounting equation to see that the left side rep ...

Assignment 1 is compulsory and due

... extract sample of trade receivables at year-end and also list of payments from masterfile after year-end and compare with the source documents to confirm is before year-end and that the trade receivables do exist at yearend extract a list of debtors who have a hold on their account or who have e ...

... extract sample of trade receivables at year-end and also list of payments from masterfile after year-end and compare with the source documents to confirm is before year-end and that the trade receivables do exist at yearend extract a list of debtors who have a hold on their account or who have e ...

intermediate-accounting-17th-edition-stice-test-bank

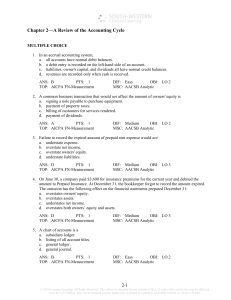

... Chapter 2—A Review of the Accounting Cycle MULTIPLE CHOICE 1. In an accrual accounting system, a. all accounts have normal debit balances. b. a debit entry is recorded on the left-hand side of an account. c. liabilities, owner's capital, and dividends all have normal credit balances. d. revenues are ...

... Chapter 2—A Review of the Accounting Cycle MULTIPLE CHOICE 1. In an accrual accounting system, a. all accounts have normal debit balances. b. a debit entry is recorded on the left-hand side of an account. c. liabilities, owner's capital, and dividends all have normal credit balances. d. revenues are ...

FREE Sample Here

... The ending owner's equity amount is shown on Learning Objective 1.11 Understand what the complete set of financial statements is and how statements are prepared a. the statement of financial position only. b. the statement of changes in equity only. c. both the income statement and the statement of ...

... The ending owner's equity amount is shown on Learning Objective 1.11 Understand what the complete set of financial statements is and how statements are prepared a. the statement of financial position only. b. the statement of changes in equity only. c. both the income statement and the statement of ...

FAP 20e Chapter 9 SM

... Revenues and expenses usually are not matched under the direct write-off method because the revenues recorded from the uncollectible accounts often appear on the income statement of one period while the bad debts expenses of those revenues appear on the income statement of a later period when the ac ...

... Revenues and expenses usually are not matched under the direct write-off method because the revenues recorded from the uncollectible accounts often appear on the income statement of one period while the bad debts expenses of those revenues appear on the income statement of a later period when the ac ...

CONTENTS - Northampton Borough Council

... The Authority accounts for income and expenditure in the period to which the service to which it relates has taken place, rather than when cash payments are received or made. Where income and expenditure has been recognised but cash has not been received or paid, a debtor or creditor for the relevan ...

... The Authority accounts for income and expenditure in the period to which the service to which it relates has taken place, rather than when cash payments are received or made. Where income and expenditure has been recognised but cash has not been received or paid, a debtor or creditor for the relevan ...

GSFIC Revenue Recognition

... during the year and make the accrual entries at year-end. The types of revenue accruals will vary from LUA to LUA depending upon its size and the types of activities and services it performs. To record a revenue accrual, a receivable account is debited and the revenue control account, as well as a s ...

... during the year and make the accrual entries at year-end. The types of revenue accruals will vary from LUA to LUA depending upon its size and the types of activities and services it performs. To record a revenue accrual, a receivable account is debited and the revenue control account, as well as a s ...

2014 Dynamics SL Year End Event

... The next step is to pull the vendor history. Quick Query/Financial/Accounts Payable/Vendor History. If you are using multiple companies follow the above instructions to filter to one company. You will need to filter this query to only show the fiscal year that you will be running 1099’s for. To add ...

... The next step is to pull the vendor history. Quick Query/Financial/Accounts Payable/Vendor History. If you are using multiple companies follow the above instructions to filter to one company. You will need to filter this query to only show the fiscal year that you will be running 1099’s for. To add ...

chapter 2

... CHAPTER STUDY OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset, liability, and owner's equity items. 2. Define debits and credits and explain their use in recording business transactions. The terms ...

... CHAPTER STUDY OBJECTIVES 1. Explain what an account is and how it helps in the recording process. An account is a record of increases and decreases in specific asset, liability, and owner's equity items. 2. Define debits and credits and explain their use in recording business transactions. The terms ...

Chap007

... Revenues and expenses usually are not matched under the direct write-off method because the revenues recorded from the uncollectible accounts often appear on the income statement of one period while the bad debts expenses of those revenues appear on the income statement of a later period when the ac ...

... Revenues and expenses usually are not matched under the direct write-off method because the revenues recorded from the uncollectible accounts often appear on the income statement of one period while the bad debts expenses of those revenues appear on the income statement of a later period when the ac ...

Instructor`s Manual Chapter 2-7e

... c. Statement of Changes in Stockholders' Equity d. Statement of Cash Flows 2. Comparative Statements in Subsequent Years 3. Illustration of Financial Statement Relationships II. Accounting Concepts and Principles A. Schematic Model of Concepts and Principles B. Concepts/Principles Related to the Ent ...

... c. Statement of Changes in Stockholders' Equity d. Statement of Cash Flows 2. Comparative Statements in Subsequent Years 3. Illustration of Financial Statement Relationships II. Accounting Concepts and Principles A. Schematic Model of Concepts and Principles B. Concepts/Principles Related to the Ent ...

Financial Statements for Manufacturing Businesses

... good decisions. Thirdly, the management accountant provides a knowledge of basic decision-making tools that helps find the best alternative in decision-making. It is the accountant’s knowledge about preparing financial statements and his or her abilities to analyze and interpret financial statements ...

... good decisions. Thirdly, the management accountant provides a knowledge of basic decision-making tools that helps find the best alternative in decision-making. It is the accountant’s knowledge about preparing financial statements and his or her abilities to analyze and interpret financial statements ...

Capitalization of Fixed Assets

... 1. Annual repair and maintenance expenditures normally are not considered capital improvements and should not be capitalized unless they add to the value of the property or materially prolong its useful life. 2. All costs associated with placing an asset in service, including freight, installation c ...

... 1. Annual repair and maintenance expenditures normally are not considered capital improvements and should not be capitalized unless they add to the value of the property or materially prolong its useful life. 2. All costs associated with placing an asset in service, including freight, installation c ...