Document

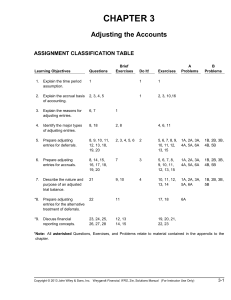

... (a) Under the time period assumption, an accountant is required to determine the relevance of each business transaction to specific accounting periods. (b) An accounting time period of one year in length is referred to as a fiscal year. A fiscal year that extends from January 1 to December 31 is ref ...

... (a) Under the time period assumption, an accountant is required to determine the relevance of each business transaction to specific accounting periods. (b) An accounting time period of one year in length is referred to as a fiscal year. A fiscal year that extends from January 1 to December 31 is ref ...

financial-and-managerial-accounting-9th-edition

... KEY: post entries and prepare trial balance 37. A trial balance is normally prepared at the end of the day. ANS: F PTS: 1 OBJ: LO4 NAT: AACSB correlation: analytic LOC: Learning type: Recall KEY: post entries and prepare trial balance 38. When the columns of the trial balance equal each other, it me ...

... KEY: post entries and prepare trial balance 37. A trial balance is normally prepared at the end of the day. ANS: F PTS: 1 OBJ: LO4 NAT: AACSB correlation: analytic LOC: Learning type: Recall KEY: post entries and prepare trial balance 38. When the columns of the trial balance equal each other, it me ...

CHAPTER 7 Cash and Receivables

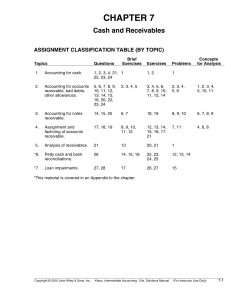

... The net method is desirable from a theoretical standpoint because it values the receivable at its net realizable value. In addition, recording the sales at net provides a better assessment of the revenue that was earned from the sale of the product. If the purchasing company fails to take the discou ...

... The net method is desirable from a theoretical standpoint because it values the receivable at its net realizable value. In addition, recording the sales at net provides a better assessment of the revenue that was earned from the sale of the product. If the purchasing company fails to take the discou ...

B.Com. Part-I Financial Accounting Sem. I Unit-2 extra material

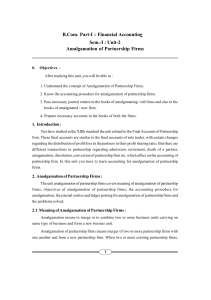

... journal entries are to be passed. a) If an asset is sold away for cash Cash / Bank A/c .................. Dr. To Particular Asset A/c b) If an asset is taken over by the partner / partners Partner/s Capital A/c .................. Dr. To Particular Asset A/c c) If a liability is paid off Particular L ...

... journal entries are to be passed. a) If an asset is sold away for cash Cash / Bank A/c .................. Dr. To Particular Asset A/c b) If an asset is taken over by the partner / partners Partner/s Capital A/c .................. Dr. To Particular Asset A/c c) If a liability is paid off Particular L ...

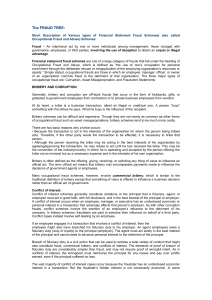

The FRAUD TREE:

... agreeing/approving the transaction, he may refuse to act until he has received the bribe. This may be the convention of the industry/country in which he is operating and accepted by the person offering the bribe not as immoral but as a necessary expense and in the interests of his own organisation. ...

... agreeing/approving the transaction, he may refuse to act until he has received the bribe. This may be the convention of the industry/country in which he is operating and accepted by the person offering the bribe not as immoral but as a necessary expense and in the interests of his own organisation. ...

Full file at http://TestbankCollege.eu/Test-Bank-Financial

... Full file at http://TestbankCollege.eu/Test-Bank-Financial-Accounting-3rd-Edition-Kemp ...

... Full file at http://TestbankCollege.eu/Test-Bank-Financial-Accounting-3rd-Edition-Kemp ...

Exam Name___________________________________ TRUE

... 43) The conceptual framework of accounting should have many positive effects as new accounting standards are developed. Which of the following is not one of those effects? A) Users' understanding and confidence in financial statements should increase. B) Accountants should be better able to assess t ...

... 43) The conceptual framework of accounting should have many positive effects as new accounting standards are developed. Which of the following is not one of those effects? A) Users' understanding and confidence in financial statements should increase. B) Accountants should be better able to assess t ...

FAP 20e Chapter 4 SM - Arab Academy Research Papers AAST

... income summary. Specifically, closing entries at the end of an accounting period prepare the revenues (and gains), expenses (and losses), and withdrawals accounts for the next period by giving them zero balances. Closing entries also update the owner’s capital account for the events of the year just ...

... income summary. Specifically, closing entries at the end of an accounting period prepare the revenues (and gains), expenses (and losses), and withdrawals accounts for the next period by giving them zero balances. Closing entries also update the owner’s capital account for the events of the year just ...

Financial Accounting and Accounting Standards

... Accounting standard-setters weigh the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available. ...

... Accounting standard-setters weigh the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available. ...

A The framework of uniform chart of accounts

... It is not only the owners or shareholders of a company who are directly related with the operations and results of that company. Apart from these people, establishments which have commercial, financial and economical relationships with the company, including individuals, creditors, finance and inves ...

... It is not only the owners or shareholders of a company who are directly related with the operations and results of that company. Apart from these people, establishments which have commercial, financial and economical relationships with the company, including individuals, creditors, finance and inves ...

Accounting Concepts - Association of Certified Fraud Examiners

... Accounts and the Accounting Cycle Entries to the left side of an account are debits (dr), and entries to the right side of an account are credits (cr). Debits increase asset and expense accounts, while credits decrease them. Conversely, credits increase liability, owners’ equity, and revenue ...

... Accounts and the Accounting Cycle Entries to the left side of an account are debits (dr), and entries to the right side of an account are credits (cr). Debits increase asset and expense accounts, while credits decrease them. Conversely, credits increase liability, owners’ equity, and revenue ...

Preview Sample File

... that is independent of the shareholders. Shareholders of most companies have limited liability for the debts of the company and if there is more than one director, the decision making is usually a shared responsibility. a. b. *c. d. ...

... that is independent of the shareholders. Shareholders of most companies have limited liability for the debts of the company and if there is more than one director, the decision making is usually a shared responsibility. a. b. *c. d. ...

denmark_costbased_approp_system

... picture of the real draw on resources in the applicable fiscal year. In the new cost-based budget system investments are financed through borrowing, and the agency budget is not affected by the total expense in that year. Instead, investments are recorded in the budget corresponding to annual costs; ...

... picture of the real draw on resources in the applicable fiscal year. In the new cost-based budget system investments are financed through borrowing, and the agency budget is not affected by the total expense in that year. Instead, investments are recorded in the budget corresponding to annual costs; ...

Acc Plus Aut09

... intangibles do not pass the tests for capitalisation except for development expenditure, but only under fairly strict criteria. There are, however, differences in the accounting treatment between IAS 38 and the new IFRS for SMEs published in July in that in the latter document development may not be ...

... intangibles do not pass the tests for capitalisation except for development expenditure, but only under fairly strict criteria. There are, however, differences in the accounting treatment between IAS 38 and the new IFRS for SMEs published in July in that in the latter document development may not be ...

Fixed Asset Policy

... exist in addition to this policy and complement but may not substitute this policy. ...

... exist in addition to this policy and complement but may not substitute this policy. ...

FREE Sample Here - We can offer most test bank and

... 8) When a portion of prepaid rent expires, what will be the effect on the balance sheet equation? A) This transaction affects only the income statement, so there will be no effect on the balance sheet. B) There will be no overall effect on total assets, because two different asset accounts will chan ...

... 8) When a portion of prepaid rent expires, what will be the effect on the balance sheet equation? A) This transaction affects only the income statement, so there will be no effect on the balance sheet. B) There will be no overall effect on total assets, because two different asset accounts will chan ...

PowerPoint ******

... Criticism of DVA • Should an institution measure its liabilities including the possibility of its own financial failure? • Accountancy standards have generally evolved to a point where “own credit risk” can be incorporated in the valuation of liabilities. • Why do accounting rules view an instituti ...

... Criticism of DVA • Should an institution measure its liabilities including the possibility of its own financial failure? • Accountancy standards have generally evolved to a point where “own credit risk” can be incorporated in the valuation of liabilities. • Why do accounting rules view an instituti ...

What You Need To Know

... entity, the nature and extent of their risks, and how the entity manages those risks. Sets the accounting treatment for intangible assets that are not dealt with specifically in another IPSAS. IPSAS 31 does not apply to intangible assets acquired in an entity combination from a non-exchange transact ...

... entity, the nature and extent of their risks, and how the entity manages those risks. Sets the accounting treatment for intangible assets that are not dealt with specifically in another IPSAS. IPSAS 31 does not apply to intangible assets acquired in an entity combination from a non-exchange transact ...

FREE Sample Here

... Refers to inflows of assets from the sale of goods and services. ____ Used to identify external transactions. ____ Used to record repetitive types of transactions. ____ Liabilities created by a customer's prepayment. ____ Determines the effects of an event in terms of the accounting equation. ____ ...

... Refers to inflows of assets from the sale of goods and services. ____ Used to identify external transactions. ____ Used to record repetitive types of transactions. ____ Liabilities created by a customer's prepayment. ____ Determines the effects of an event in terms of the accounting equation. ____ ...

Chapter 5 Merchandising Operations

... of Goods Sold account. In the case of a return, the cost of the merchandise is transferred from Cost of Goods Sold back to Merchandise Inventory. • Sales of Merchandise on Credit: Two entries are necessary. Record the sale as a debit to Accounts Receivable. Update the Cost of Goods sold by tra ...

... of Goods Sold account. In the case of a return, the cost of the merchandise is transferred from Cost of Goods Sold back to Merchandise Inventory. • Sales of Merchandise on Credit: Two entries are necessary. Record the sale as a debit to Accounts Receivable. Update the Cost of Goods sold by tra ...

Cash Flow Statement

... increase in uncollected cash from credit sales. It represents $22.5m of use of cash to invest in accounts receivable. 2. Inventory increased by $148.50 million indicating use of cash to ...

... increase in uncollected cash from credit sales. It represents $22.5m of use of cash to invest in accounts receivable. 2. Inventory increased by $148.50 million indicating use of cash to ...

Task Team of FUNDAMENTAL ACCOUNTING School of Business

... the amount due. Credit terms dictate when payment is due (the credit period) and clarify the nature of any discounts offered to customers who pay their accounts early. By encouraging customers to make early payment, cash discounts reduce the amount a supplier has invested in its accounts receivable, ...

... the amount due. Credit terms dictate when payment is due (the credit period) and clarify the nature of any discounts offered to customers who pay their accounts early. By encouraging customers to make early payment, cash discounts reduce the amount a supplier has invested in its accounts receivable, ...

6. Compliance audit of a real estate agent`s trust

... • cash receipts for all trust money received by the agent, detailing date received, amount, name of client, and purpose of the receipt; • register of items other than trust money received, such as documents of title, detailing date received, particulars of documents and client name; • trust trans ...

... • cash receipts for all trust money received by the agent, detailing date received, amount, name of client, and purpose of the receipt; • register of items other than trust money received, such as documents of title, detailing date received, particulars of documents and client name; • trust trans ...