Internal Control

... dad had given her money to go shopping. The Hamilton Spectator, Wednesday, June 22, 2005. ...

... dad had given her money to go shopping. The Hamilton Spectator, Wednesday, June 22, 2005. ...

FRANKLIN ELECTRIC CO., INC. AUDIT COMMITTEE CHARTER

... completeness and accuracy of the financial statements rests with the Company’s management. The responsibility of the Company’s independent registered public accounting firm is to perform an audit of the Company’s financial statements and to express an opinion on (i) the conformity of the Company’s a ...

... completeness and accuracy of the financial statements rests with the Company’s management. The responsibility of the Company’s independent registered public accounting firm is to perform an audit of the Company’s financial statements and to express an opinion on (i) the conformity of the Company’s a ...

working program - Almaty Management University

... Audit evidence and their views. Sources and methods of obtaining audit evidence. System of criteria of evidence. Audit procedures (methods) and audit evidence. Classification of evidence. ISA 500, "Audit Evidence." Audit procedures. Analytical procedures. ISA 330, "Audit procedures regarding the ass ...

... Audit evidence and their views. Sources and methods of obtaining audit evidence. System of criteria of evidence. Audit procedures (methods) and audit evidence. Classification of evidence. ISA 500, "Audit Evidence." Audit procedures. Analytical procedures. ISA 330, "Audit procedures regarding the ass ...

1305080572_448208

... Provide assurance on financial statement-related items Evaluate effectiveness of operations and related controls Investigate concerns of fraud Evaluate the effectiveness of internal control processes Perform operational audits Evaluate the organization’s compliance with laws, regulations, and compan ...

... Provide assurance on financial statement-related items Evaluate effectiveness of operations and related controls Investigate concerns of fraud Evaluate the effectiveness of internal control processes Perform operational audits Evaluate the organization’s compliance with laws, regulations, and compan ...

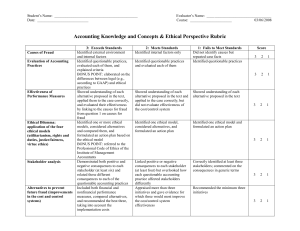

Rubric for Power Point Presentation

... formulated an action plan based on the ethical model BONUS POINT: referred to the Professional Code of Ethics of the Institute of Management ...

... formulated an action plan based on the ethical model BONUS POINT: referred to the Professional Code of Ethics of the Institute of Management ...

Competency area - Chartered Institute of Internal Auditors

... International Professional Practices Framework Core competency Applies the relevant portions of the International Professional Practices Framework ...

... International Professional Practices Framework Core competency Applies the relevant portions of the International Professional Practices Framework ...

Leading Practice Examples of Audit Committee Reporting

... Typical Audit Committee Agenda Call to order Review and approval of minutes from prior meeting Audit committee report by internal auditors Audit committee report by external auditors ...

... Typical Audit Committee Agenda Call to order Review and approval of minutes from prior meeting Audit committee report by internal auditors Audit committee report by external auditors ...

Part II. Essay Questions (60%)

... c. modify the initial assessments of inhere risk and preliminary judgments about materiality levels. d. determine the nature, timing, and extent of substantive tests for financial statement assertions. 13. Which of the following is not one of the principal CPA firm’s alternatives when issuing a repo ...

... c. modify the initial assessments of inhere risk and preliminary judgments about materiality levels. d. determine the nature, timing, and extent of substantive tests for financial statement assertions. 13. Which of the following is not one of the principal CPA firm’s alternatives when issuing a repo ...

Internal Controls - Trans

... Over-reliance on one individual in the accounting function Volunteer boards; do not fail to require an audit ...

... Over-reliance on one individual in the accounting function Volunteer boards; do not fail to require an audit ...

Answers

... reviews, where they enter the store as a customer, purchase goods and rate the overall shopping experience. This is then fed back to each shop to improve customer service and can provide the basis for further training if necessary. Overall review of financial/operational controls The department coul ...

... reviews, where they enter the store as a customer, purchase goods and rate the overall shopping experience. This is then fed back to each shop to improve customer service and can provide the basis for further training if necessary. Overall review of financial/operational controls The department coul ...

The Auditor - Whose Agent Is He Anyway

... opposite view, ‘agency theory suggests that published accounts are far from being “largely irrelevant” to shareholders nor are audits of the same.’ The aim of financial statements is to report on the company’s financial performance during the year and its position at the balance sheet date, to help ...

... opposite view, ‘agency theory suggests that published accounts are far from being “largely irrelevant” to shareholders nor are audits of the same.’ The aim of financial statements is to report on the company’s financial performance during the year and its position at the balance sheet date, to help ...

internal-auditing-instructional-material

... Need detail planning Requiring comprehensive cost analysis data to set objectives in safeguarding financial resources ...

... Need detail planning Requiring comprehensive cost analysis data to set objectives in safeguarding financial resources ...

Audit Committee 18 September 2012

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...

III Local audit of project accounts

... the separation of conflicting or important functions and processes such as commitment to obligations, signing and recording of expenses, matching of cash and bank account balances, clarification of long-term unsettled receivables and obligations, physical existence of material goods, etc. Existenc ...

... the separation of conflicting or important functions and processes such as commitment to obligations, signing and recording of expenses, matching of cash and bank account balances, clarification of long-term unsettled receivables and obligations, physical existence of material goods, etc. Existenc ...

Credit Risk Financial Analyst

... Financial Models – maintain credit models to ensure accurate credit grading of airline customers Risk systems – ensure internal systems accurately record counterparty exposure Liaise will all internal departments to ensure all necessary information is collected in a timely manner to prepare necessar ...

... Financial Models – maintain credit models to ensure accurate credit grading of airline customers Risk systems – ensure internal systems accurately record counterparty exposure Liaise will all internal departments to ensure all necessary information is collected in a timely manner to prepare necessar ...

November 12, 2014 International Ethics Standards Board for

... the proposal, IESBA evaluates whether the current time-on/time-off period of 7/2 remains appropriate to address the treat of long association for key audit partners (KAPs) of a public interest entity (PIE). We agree with the IESBA of the need to propose changes to increase the cooling-off period for ...

... the proposal, IESBA evaluates whether the current time-on/time-off period of 7/2 remains appropriate to address the treat of long association for key audit partners (KAPs) of a public interest entity (PIE). We agree with the IESBA of the need to propose changes to increase the cooling-off period for ...

Please click here to print a copy of the position.

... risk/rewards analysis of prospective contracts and in the preparation and submission of proposals for grants and contracts with the Federal government and in contract administration activities. Candidates must be experienced in the preparation and oversight of the operating budget, management and co ...

... risk/rewards analysis of prospective contracts and in the preparation and submission of proposals for grants and contracts with the Federal government and in contract administration activities. Candidates must be experienced in the preparation and oversight of the operating budget, management and co ...

Hang Chi Holdings Limited 恒智控股有限公司

... 5.2 to be primarily responsible for making recommendations to the Board on the appointment, reappointment and removal of the external auditor, and to approve the remuneration and terms of engagement of the external auditor, and any questions of its resignation or dismissal; 5.3 to review and monit ...

... 5.2 to be primarily responsible for making recommendations to the Board on the appointment, reappointment and removal of the external auditor, and to approve the remuneration and terms of engagement of the external auditor, and any questions of its resignation or dismissal; 5.3 to review and monit ...

Auditor`s Responsibility

... • Identifies five interrelated components of internal control Control environment Control activities Monitoring of controls ...

... • Identifies five interrelated components of internal control Control environment Control activities Monitoring of controls ...

Major Duties and Responsibilities of Assistant Manager (Audit)

... independent department entrusts to conduct financial and management audit of its Partner Organizations (POs), which are directly implementing PKSF’s programs and projects at field level all over the country. IAD is also responsible for conducting pre-audit of all payments and expenditures of PKSF in ...

... independent department entrusts to conduct financial and management audit of its Partner Organizations (POs), which are directly implementing PKSF’s programs and projects at field level all over the country. IAD is also responsible for conducting pre-audit of all payments and expenditures of PKSF in ...

Corporate Governance

... presentation) (UK/International approach) In practice there is a concerted effort to bring US and UK/International accounting standards together. ...

... presentation) (UK/International approach) In practice there is a concerted effort to bring US and UK/International accounting standards together. ...