Chapter 5

... – Explanatory notes disclosing changes in account procedures, or significant events occurring after balance sheet dates ...

... – Explanatory notes disclosing changes in account procedures, or significant events occurring after balance sheet dates ...

FRANKLIN ELECTRIC CO., INC. AUDIT COMMITTEE CHARTER

... member shall have past employment experience in finance or accounting, requisite professional certification in accounting, or any other comparable experience or background which results in the individual’s financial sophistication, such as serving or having served as a chief executive officer, chief ...

... member shall have past employment experience in finance or accounting, requisite professional certification in accounting, or any other comparable experience or background which results in the individual’s financial sophistication, such as serving or having served as a chief executive officer, chief ...

Merchandising Operations and the Multiple

... Identify the sections of a classified balance sheet. Identify and compute ratios for analyzing a company's profitability. Explain the relationship between a retained earnings statement and a statement of ...

... Identify the sections of a classified balance sheet. Identify and compute ratios for analyzing a company's profitability. Explain the relationship between a retained earnings statement and a statement of ...

approaches concerning the control techniques` utilization for

... The distribution costs usually include market research expenditure, storage and handling expenditure, commercial, advertisement and promotion expenditure, direct sale expenditure, transport cost and others, not previously mentioned, but which – related to the activity of business – are related to th ...

... The distribution costs usually include market research expenditure, storage and handling expenditure, commercial, advertisement and promotion expenditure, direct sale expenditure, transport cost and others, not previously mentioned, but which – related to the activity of business – are related to th ...

Financial Accounting and Accounting Standards

... regulatory filings, which represents trillions of dollars in market capitalization. ...

... regulatory filings, which represents trillions of dollars in market capitalization. ...

Line 43a – Other Consulting and Contract

... issues. These meetings have been held for the past 15 years. NCCS maintains an ongoing list of issues and adds ideas suggested by the many national and subsector organizations, nonprofit managers, attorneys, accountants, and other interested individuals who are part of the NCCS Quality Reporting Net ...

... issues. These meetings have been held for the past 15 years. NCCS maintains an ongoing list of issues and adds ideas suggested by the many national and subsector organizations, nonprofit managers, attorneys, accountants, and other interested individuals who are part of the NCCS Quality Reporting Net ...

FREE Sample Here

... Which of these events cannot be quantified into dollars and cents and recorded as an accounting transaction? Learning Objective 1.8 Explain the meaning of the monetary unit assumption and the economic entity assumption *a. The appointment of a new accounting firm to perform an audit. b. The purchase ...

... Which of these events cannot be quantified into dollars and cents and recorded as an accounting transaction? Learning Objective 1.8 Explain the meaning of the monetary unit assumption and the economic entity assumption *a. The appointment of a new accounting firm to perform an audit. b. The purchase ...

Financial Accounting

... A sole proprietor’s owner’s equity balance was $10,000 at the beginning of the year and was $22,000 at the end of the year. During the year the owner invested $5,000 in the business and had withdrawn $24,000 for personal use. The sole proprietorship’s net income for the year was $ ...

... A sole proprietor’s owner’s equity balance was $10,000 at the beginning of the year and was $22,000 at the end of the year. During the year the owner invested $5,000 in the business and had withdrawn $24,000 for personal use. The sole proprietorship’s net income for the year was $ ...

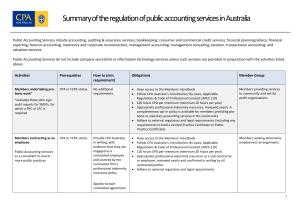

Australia

... audit of SMSFs (minimum eight hours) • financial statement or compliance audit training (minimum eight hours) • financial accounting training (minimum four hours). These requirements are included in the minimum 120 hour CPD requirement. Detailed guidance on the requirements ,as prescribed by the Joi ...

... audit of SMSFs (minimum eight hours) • financial statement or compliance audit training (minimum eight hours) • financial accounting training (minimum four hours). These requirements are included in the minimum 120 hour CPD requirement. Detailed guidance on the requirements ,as prescribed by the Joi ...

ACCOUNTING

... misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by the management, as well as evaluating the overall financial state ...

... misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by the management, as well as evaluating the overall financial state ...

G.A.A.P.

... The time period principle is the concept that a business should report the financial results of its activities over a standard time period, which is usually monthly, quarterly, or annually. ...

... The time period principle is the concept that a business should report the financial results of its activities over a standard time period, which is usually monthly, quarterly, or annually. ...

Document

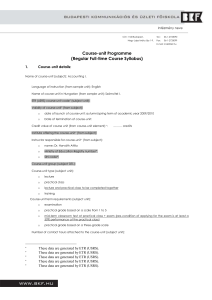

... Name of course-unit (subject): Accounting I. Language of instruction (from sample unit): English Name of course-unit in Hungarian (from sample unit): Számvitel I. ETR (USRS) course-unit code (subject unit): Validity of course-unit (from subject): ...

... Name of course-unit (subject): Accounting I. Language of instruction (from sample unit): English Name of course-unit in Hungarian (from sample unit): Számvitel I. ETR (USRS) course-unit code (subject unit): Validity of course-unit (from subject): ...

5 ACCOUNTING FOR

... competence, judgment, and ethical behavior of professional accountants. The chapter begins with an overview of career opportunities offered by the accounting profession. Opportunities in public, management, and government accounting are surveyed, as are career paths in education. We take this opport ...

... competence, judgment, and ethical behavior of professional accountants. The chapter begins with an overview of career opportunities offered by the accounting profession. Opportunities in public, management, and government accounting are surveyed, as are career paths in education. We take this opport ...

1. The primary function of financial accounting is

... 54. The most political issue in the FASB's most recent deliberations and amendments to GAAP on business combinations was: A The negative effects on subsequent earnings of amortizing goodwill if firms were required to use the . purchase method of accounting for the combination. B The negative effect ...

... 54. The most political issue in the FASB's most recent deliberations and amendments to GAAP on business combinations was: A The negative effects on subsequent earnings of amortizing goodwill if firms were required to use the . purchase method of accounting for the combination. B The negative effect ...

Villegas y Villegas Mexico Joins Alliott Group Press Release

... industrial cities, and their clients have been expanding rapidly reflecting the scope of services offered by Villegas y Villegas Currently the focus of Villegas y Villegas main clients’ is the position within a global market for which Villegas y Villegas is now establishing a strong presence within ...

... industrial cities, and their clients have been expanding rapidly reflecting the scope of services offered by Villegas y Villegas Currently the focus of Villegas y Villegas main clients’ is the position within a global market for which Villegas y Villegas is now establishing a strong presence within ...

Financial Accounting and Accounting Standards

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

Financial Accounting and Accounting Standards

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

Financial Accounting and Accounting Standards

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

... similar decisions. (b) helps present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts. (c) portrays the economic resources of an enterprise, the claims to those resources, and the effects of transactions, events, and ...

chapter 2 - CSUN.edu

... Identify and compute ratios for analyzing a company's profitability. Explain the relationship between a retained earnings statement and a statement of ...

... Identify and compute ratios for analyzing a company's profitability. Explain the relationship between a retained earnings statement and a statement of ...

Business Administration

... Macroeconomics, Introduction This course introduces basic concepts and tools used in macroeconomic analysis. You’ll learn about the theory, measurement, and determination of national income; business cycles; the multiplier; fiscal policy, budget deficits and the national debt; aggregate supply and a ...

... Macroeconomics, Introduction This course introduces basic concepts and tools used in macroeconomic analysis. You’ll learn about the theory, measurement, and determination of national income; business cycles; the multiplier; fiscal policy, budget deficits and the national debt; aggregate supply and a ...

Chapter 1 - Pearson Schools and FE Colleges

... financial statements. The prudence concept. When preparing financial statements, accountants often have to use their judgement in determining the valuation of a particular asset, i.e. premises, machinery etc., or perhaps deciding whether an outstanding debt will ever be paid. It is the accountant’s du ...

... financial statements. The prudence concept. When preparing financial statements, accountants often have to use their judgement in determining the valuation of a particular asset, i.e. premises, machinery etc., or perhaps deciding whether an outstanding debt will ever be paid. It is the accountant’s du ...

DOC - ESW Group

... MSCM’s reports on the Company’s financial statements as of and for the fiscal years ended December 31, 2011 and 2012 contained a qualification that due to the Company’s experience of negative cash flows from operations and its dependency upon future financing raise substantial doubt about its abilit ...

... MSCM’s reports on the Company’s financial statements as of and for the fiscal years ended December 31, 2011 and 2012 contained a qualification that due to the Company’s experience of negative cash flows from operations and its dependency upon future financing raise substantial doubt about its abilit ...

DOC - ESW Group

... On May 31, 2013, Environmental Solution Worldwide Inc. (the “Company”) received notice that, effective as of June 1, 2013, MSCM LLP (“MSCM”), the Company’s independent registered public accountants, merged with MNP LLP (“MNP”). Most of the professional staff of MSCM continued with MNP either as empl ...

... On May 31, 2013, Environmental Solution Worldwide Inc. (the “Company”) received notice that, effective as of June 1, 2013, MSCM LLP (“MSCM”), the Company’s independent registered public accountants, merged with MNP LLP (“MNP”). Most of the professional staff of MSCM continued with MNP either as empl ...

Financial Accounting and Accounting Standards

... 3. Which product line is most profitable? 4. Is cash sufficient to pay dividends to the stockholders? 5. What price for our product will maximize net income? 6. Will the company be able to pay its short-term debts? Chapter ...

... 3. Which product line is most profitable? 4. Is cash sufficient to pay dividends to the stockholders? 5. What price for our product will maximize net income? 6. Will the company be able to pay its short-term debts? Chapter ...

Accounting

Accounting or Accountancy is the measurement, processing and communication of financial information about economic entities. Accounting, which has been called the ""language of business"", measures the results of an organization's economic activities and conveys this information to a variety of users including investors, creditors, management, and regulators. Practitioners of accounting are known as accountants. The terms accounting and financial reporting are often used as synonyms.Accounting can be divided into several fields including financial accounting, management accounting, auditing, and tax accounting. Accounting information systems are designed to support accounting functions and related activities. Financial accounting focuses on the reporting of an organization's financial information, including the preparation of financial statements, to external users of the information, such as investors, regulators and suppliers; and management accounting focuses on the measurement, analysis and reporting of information for internal use by management. The recording of financial transactions, so that summaries of the financials may be presented in financial reports, is known as bookkeeping, of which double-entry bookkeeping is the most common system.Accounting is facilitated by accounting organizations such as standard-setters, accounting firms and professional bodies. Financial statements are usually audited by accounting firms, and are prepared in accordance with generally accepted accounting principles (GAAP). GAAP is set by various standard-setting organizations such as the Financial Accounting Standards Board (FASB) in the United States and the Financial Reporting Council in the United Kingdom. As of 2012, ""all major economies"" have plans to converge towards or adopt the International Financial Reporting Standards (IFRS).