PJM Manual 28:

... Spot Market Accounting Overview..............................................................................16 Business Rules for InSchedule and Power Meter Data Submissions.........................16 Calculating Spot Market Interchange............................................................... ...

... Spot Market Accounting Overview..............................................................................16 Business Rules for InSchedule and Power Meter Data Submissions.........................16 Calculating Spot Market Interchange............................................................... ...

American Italian Pasta Co.

... given by counsel to the Audit Committee, AIPC or its Board of Directors after the commencement of the Audit Committee investigation; ...

... given by counsel to the Audit Committee, AIPC or its Board of Directors after the commencement of the Audit Committee investigation; ...

Segment Reporting

... produces and the different geographical areas in which it operates—to help users of financial statements: (a) better understand the entity’s past performance; (b) better assess the entity’s risks and returns; and (c) make more informed judgments about the entity as a whole. Many entities provide gro ...

... produces and the different geographical areas in which it operates—to help users of financial statements: (a) better understand the entity’s past performance; (b) better assess the entity’s risks and returns; and (c) make more informed judgments about the entity as a whole. Many entities provide gro ...

AU-C 315, Understanding the Entity and its Environment

... .03 The objective of the auditor is to identify and assess the risks of material misstatement, whether due to fraud or error, at the financial statement and relevant assertion levels through understanding the entity and its environment, including the entity's internal control, thereby providing a ba ...

... .03 The objective of the auditor is to identify and assess the risks of material misstatement, whether due to fraud or error, at the financial statement and relevant assertion levels through understanding the entity and its environment, including the entity's internal control, thereby providing a ba ...

Stockholm 17 mars

... communicated in the auditor’s report? If not, why? FAR has strong concerns about the content in a KAM as described in ED 701 paragraph 10 (a); “The description….shall include: (a) …….., its effect on the audit”. The meaning of describing “its effect on the audit” is further explained in paragraphs A ...

... communicated in the auditor’s report? If not, why? FAR has strong concerns about the content in a KAM as described in ED 701 paragraph 10 (a); “The description….shall include: (a) …….., its effect on the audit”. The meaning of describing “its effect on the audit” is further explained in paragraphs A ...

Personal Financial Statements, Pro Forma

... 20XX, included in the accompanying prescribed form in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. I also have compiled the supplementary information presented in the prescribed form. My compilation was l ...

... 20XX, included in the accompanying prescribed form in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. I also have compiled the supplementary information presented in the prescribed form. My compilation was l ...

Download attachment

... reporting entity. As a result, the CICA Handbook – Accounting has been restructured to move away from a single financial reporting framework referred to as Canadian generally accepted accounting principles (GAAP) to include various different financial reporting frameworks in Canadian GAAP. These dif ...

... reporting entity. As a result, the CICA Handbook – Accounting has been restructured to move away from a single financial reporting framework referred to as Canadian generally accepted accounting principles (GAAP) to include various different financial reporting frameworks in Canadian GAAP. These dif ...

Do Earnings Forecast Errors Affect Firm Value and

... guidelines required Taiwanese firms to include earnings forecasts in their prospectuses for years in which they raise additional capital. The firms are also required to disclose the earnings forecast for two years after the security issuance. The main motivation for this was to reduce the informatio ...

... guidelines required Taiwanese firms to include earnings forecasts in their prospectuses for years in which they raise additional capital. The firms are also required to disclose the earnings forecast for two years after the security issuance. The main motivation for this was to reduce the informatio ...

Read the full report

... Garry is a Professor of Accounting and Head, School of Accounting at RMIT University. He has been employed in the Australian higher education sector since 1985 after gaining experience in the IT industry, professional accounting services and in the financial services industry. His published research ...

... Garry is a Professor of Accounting and Head, School of Accounting at RMIT University. He has been employed in the Australian higher education sector since 1985 after gaining experience in the IT industry, professional accounting services and in the financial services industry. His published research ...

a review of the earnings management literature and its implications

... important opportunities for future research on earnings management to be informative for standard setters. For instance, most studies have not examined whether the observed effects are attributable to a few firms or are pervasive, both in the sample and in the population. This information is likely ...

... important opportunities for future research on earnings management to be informative for standard setters. For instance, most studies have not examined whether the observed effects are attributable to a few firms or are pervasive, both in the sample and in the population. This information is likely ...

ARATANA THERAPEUTICS, INC. AUDIT COMMITTEE CHARTER

... shall consist of at least three (3) members of the Board. Each Committee member must be able to read and understand fundamental financial statements, including, but not limited to, a company’s balance sheet, income statement and cash flow statement. Members of the Committee are not required to be en ...

... shall consist of at least three (3) members of the Board. Each Committee member must be able to read and understand fundamental financial statements, including, but not limited to, a company’s balance sheet, income statement and cash flow statement. Members of the Committee are not required to be en ...

ASIAN COMPANIES` Financial reporting frequency

... reporting frequency practices are not written, this point is worth mentioning for comprehensive analysis of Asian companies that are also listen in non-Asian stock exchanges. 3.) The research findings were generally true for commercial companies. Non-commercial or Financial companies have different ...

... reporting frequency practices are not written, this point is worth mentioning for comprehensive analysis of Asian companies that are also listen in non-Asian stock exchanges. 3.) The research findings were generally true for commercial companies. Non-commercial or Financial companies have different ...

Scott and Company LLC and Michael J. Slapnik, CPA

... By this Order, the Public Company Accounting Oversight Board (the "Board" or "PCAOB") is (1) censuring Scott and Company LLC (the "Firm" or "Scott"), (2) imposing upon the Firm a civil money penalty in the amount of $10,000, (3) in the event that the Board grants any future registration application ...

... By this Order, the Public Company Accounting Oversight Board (the "Board" or "PCAOB") is (1) censuring Scott and Company LLC (the "Firm" or "Scott"), (2) imposing upon the Firm a civil money penalty in the amount of $10,000, (3) in the event that the Board grants any future registration application ...

cti biopharma corp. - corporate

... The information provided pursuant to this Item 2.02 shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934 (the “Exchange Act”) or otherwise subject to the liabilities of that section, and shall not be incorporated by reference into any filing or other document ...

... The information provided pursuant to this Item 2.02 shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934 (the “Exchange Act”) or otherwise subject to the liabilities of that section, and shall not be incorporated by reference into any filing or other document ...

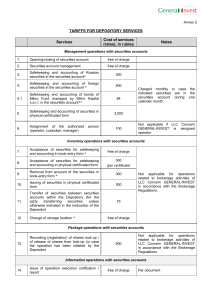

Tariffs depository

... 1. Settlement period shall be a calendar month; the calculation is carried out for each securities account of the Depositor. 2. All rates do not include any overhead costs and services of third parties (parent depositories, registrars). 3. Payment for Depository services shall be made by the Deposit ...

... 1. Settlement period shall be a calendar month; the calculation is carried out for each securities account of the Depositor. 2. All rates do not include any overhead costs and services of third parties (parent depositories, registrars). 3. Payment for Depository services shall be made by the Deposit ...

Accounting Fraud: Booms, Busts, and Incentives to Perform

... Crash in 1929, after the Savings & Loans scandal in the 1980s, and after the dot-com bubble of the late 1990s/early 2000s1. Sweeping changes in regulation have often followed these scandals; the Sarbanes-Oxley Act, for example, was drafted to reduce the likelihood of fraudulent reporting after the d ...

... Crash in 1929, after the Savings & Loans scandal in the 1980s, and after the dot-com bubble of the late 1990s/early 2000s1. Sweeping changes in regulation have often followed these scandals; the Sarbanes-Oxley Act, for example, was drafted to reduce the likelihood of fraudulent reporting after the d ...

Companies Act 2014 - Audit reports

... continues to incorporate the citation ‘Irish Generally Accepted Accounting Practice’ for statutory audit reports where FRS 101 ‘Reduced Disclosure Framework’ or FRS 102 ‘The Financial Reporting Standard applicable in the UK and Republic of Ireland’, has not been applied. If FRS 101 ‘Reduced Disclosu ...

... continues to incorporate the citation ‘Irish Generally Accepted Accounting Practice’ for statutory audit reports where FRS 101 ‘Reduced Disclosure Framework’ or FRS 102 ‘The Financial Reporting Standard applicable in the UK and Republic of Ireland’, has not been applied. If FRS 101 ‘Reduced Disclosu ...

PowerPoint slideshow for chapter 1

... The Securities and Exchange Commission (SEC), an agency of the U.S. government, has authority over the accounting and financial disclosures for companies whose shares of ownership (stock) are traded and sold to the public. Many countries outside the U.S. use generally accepted accounting principles ...

... The Securities and Exchange Commission (SEC), an agency of the U.S. government, has authority over the accounting and financial disclosures for companies whose shares of ownership (stock) are traded and sold to the public. Many countries outside the U.S. use generally accepted accounting principles ...

Chapter 1 - Faculty of Business and Economics Courses

... LO 14-5 Analyze the statement of cash flows to evaluate the increase and decrease in a company’s cash balance. LO 14-6 Assess a company’s financial position using its accounting statements and ratio analysis. © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instruc ...

... LO 14-5 Analyze the statement of cash flows to evaluate the increase and decrease in a company’s cash balance. LO 14-6 Assess a company’s financial position using its accounting statements and ratio analysis. © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instruc ...

Revenue Recognition

... interpretations of the Commission but rather represent the interpretations and practices followed by the Division of Corporation Finance and the Office of the Chief Accountant in administering the disclosure requirements of the Federal securities ...

... interpretations of the Commission but rather represent the interpretations and practices followed by the Division of Corporation Finance and the Office of the Chief Accountant in administering the disclosure requirements of the Federal securities ...

Download Dissertation

... the footnotes of the financial statements before SFAS 158 and SFAS 158 does not require firms to provide additional information for information users. Second, SFAS 158 influences only balance sheets, not income statements since the smoothing mechanism of the previous accounting regulation still appl ...

... the footnotes of the financial statements before SFAS 158 and SFAS 158 does not require firms to provide additional information for information users. Second, SFAS 158 influences only balance sheets, not income statements since the smoothing mechanism of the previous accounting regulation still appl ...

10414-378 IFRS IT White Paper WEB FINAL

... Compliance with Sarbanes-Oxley requirements and meeting external auditor expectations requires a company to have a documented process of how financial reports are completed. Depending on the extent to which processes will change, be created, or run in parallel in an IFRS implementation, internal con ...

... Compliance with Sarbanes-Oxley requirements and meeting external auditor expectations requires a company to have a documented process of how financial reports are completed. Depending on the extent to which processes will change, be created, or run in parallel in an IFRS implementation, internal con ...

Financial Statements for the period ending November

... International Financial Reporting Standards (“IFRS”) with the assumption that the Company will be able to realize its assets and discharge its liabilities in the normal course of business. These unaudited condensed interim consolidated financial statements were approved and authorized for issue on J ...

... International Financial Reporting Standards (“IFRS”) with the assumption that the Company will be able to realize its assets and discharge its liabilities in the normal course of business. These unaudited condensed interim consolidated financial statements were approved and authorized for issue on J ...

The Role of Carbon Accounting in Corporate

... participate in a carbon emission right trading market. The paper then provides detailed methodology that can be applied for firms to improve its climate change strategy and carbon management system to achieve carbon reduction targets. Climate policy is an extremely broad issue, thus the need to subs ...

... participate in a carbon emission right trading market. The paper then provides detailed methodology that can be applied for firms to improve its climate change strategy and carbon management system to achieve carbon reduction targets. Climate policy is an extremely broad issue, thus the need to subs ...

Accounting

Accounting or Accountancy is the measurement, processing and communication of financial information about economic entities. Accounting, which has been called the ""language of business"", measures the results of an organization's economic activities and conveys this information to a variety of users including investors, creditors, management, and regulators. Practitioners of accounting are known as accountants. The terms accounting and financial reporting are often used as synonyms.Accounting can be divided into several fields including financial accounting, management accounting, auditing, and tax accounting. Accounting information systems are designed to support accounting functions and related activities. Financial accounting focuses on the reporting of an organization's financial information, including the preparation of financial statements, to external users of the information, such as investors, regulators and suppliers; and management accounting focuses on the measurement, analysis and reporting of information for internal use by management. The recording of financial transactions, so that summaries of the financials may be presented in financial reports, is known as bookkeeping, of which double-entry bookkeeping is the most common system.Accounting is facilitated by accounting organizations such as standard-setters, accounting firms and professional bodies. Financial statements are usually audited by accounting firms, and are prepared in accordance with generally accepted accounting principles (GAAP). GAAP is set by various standard-setting organizations such as the Financial Accounting Standards Board (FASB) in the United States and the Financial Reporting Council in the United Kingdom. As of 2012, ""all major economies"" have plans to converge towards or adopt the International Financial Reporting Standards (IFRS).