GLOBAL AND DOMESTIC ECONOMY (MKTG 101)

... produced and by whom through their dollar votes. Survival, profit, survival, and growth are not guaranteed for producers; prices change according to supply and demand, and consumers have freedom of choice. ...

... produced and by whom through their dollar votes. Survival, profit, survival, and growth are not guaranteed for producers; prices change according to supply and demand, and consumers have freedom of choice. ...

Basic Need, Merit, or Economic Good

... water can be a basic human need, merit good, or an ordinary economic good: – under conditions of extreme scarcity, there is only one option and only one choice to be made, which is to get the water to the thirsty, which closes all options. In this case, water is no more an economic good but a basic ...

... water can be a basic human need, merit good, or an ordinary economic good: – under conditions of extreme scarcity, there is only one option and only one choice to be made, which is to get the water to the thirsty, which closes all options. In this case, water is no more an economic good but a basic ...

Marketing mix of XY company

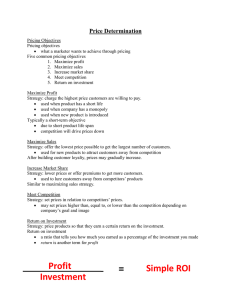

... Brand, logo, external product features Innovations, services 4. Pricing policy Price strategy and price setting Fundamental price and their comparison with competitors (at the level of either producer or retail) Price discounts 5. Distribution Buyers and their localization Distribution ...

... Brand, logo, external product features Innovations, services 4. Pricing policy Price strategy and price setting Fundamental price and their comparison with competitors (at the level of either producer or retail) Price discounts 5. Distribution Buyers and their localization Distribution ...

entry

... To maximize profit, produce the output level for which: MR = MC (that is, p = MC) . . . unless p < AVC. In that case, shut-down (produce zero output) for the short-run. If AVC < p < ATC, continue to produce in short-run, but exit in long-run if market conditions don’t improve. These rules describe t ...

... To maximize profit, produce the output level for which: MR = MC (that is, p = MC) . . . unless p < AVC. In that case, shut-down (produce zero output) for the short-run. If AVC < p < ATC, continue to produce in short-run, but exit in long-run if market conditions don’t improve. These rules describe t ...

Chapter 11

... 2. There are no restrictions to entry into the industry. 3. Established firms have no advantages over new ones. 4. Sellers and buyers are well informed about prices. B. How Perfect Competition Arises 1. Perfect competition arises when firm’s minimum efficient scale is small relative to market demand ...

... 2. There are no restrictions to entry into the industry. 3. Established firms have no advantages over new ones. 4. Sellers and buyers are well informed about prices. B. How Perfect Competition Arises 1. Perfect competition arises when firm’s minimum efficient scale is small relative to market demand ...

Goal 8.05 Predict how prices change when there is

... Market price: the price paid by the buyer and accepted by the seller Perfect competition: a market with a large number of firms all producing the same product at the same price. ...

... Market price: the price paid by the buyer and accepted by the seller Perfect competition: a market with a large number of firms all producing the same product at the same price. ...

Practice Quiz #12

... In the opening of free trade, if world prices of a good are less than domestic prices of that same good, a. domestic consumers will experience a loss of surplus. b. domestic prices will drop to the world price level. c. all domestic producers of that good will try to find another market because they ...

... In the opening of free trade, if world prices of a good are less than domestic prices of that same good, a. domestic consumers will experience a loss of surplus. b. domestic prices will drop to the world price level. c. all domestic producers of that good will try to find another market because they ...

27 – Oligopoly and Strategic Behavior

... output during the price war, thus signaling potential competitors that they will engage in a price war. Existing domestic firms can also raise the cost of entry by foreign firms by getting the U.S. government to pass stringent environmental or health and safety standards. B. Limit-Pricing Strategies ...

... output during the price war, thus signaling potential competitors that they will engage in a price war. Existing domestic firms can also raise the cost of entry by foreign firms by getting the U.S. government to pass stringent environmental or health and safety standards. B. Limit-Pricing Strategies ...

Supply - TeacherWeb

... Elasticity of Supply A. A measure of the way quantity supplied reacts to a change in price B. Elasticity = % change in quantity demanded % change in price ...

... Elasticity of Supply A. A measure of the way quantity supplied reacts to a change in price B. Elasticity = % change in quantity demanded % change in price ...

Oligopoly (lecture)

... • The cartel model is appropriate for oligopolists that collude, set a monopoly price, and prevent market entry • The contestable market model describes oligopolies that set a competitive price and have no barriers to entry • Oligopoly markets lie between these two extremes • Both models use strateg ...

... • The cartel model is appropriate for oligopolists that collude, set a monopoly price, and prevent market entry • The contestable market model describes oligopolies that set a competitive price and have no barriers to entry • Oligopoly markets lie between these two extremes • Both models use strateg ...

Perfect Competition Questions Question 1 Suppose there is a

... P 100 4QD and market supply is P=Qs. Denoting firm level quantity by q, assume TC=50+4q+2q2 so that MC=4+4q. a) What is the market equilibrium price and quantity? Set demand equal to supply and find 100-4Q=Q, so Q=20, P=20. b) How many firms are in the industry in the short run? Perfectly competitiv ...

... P 100 4QD and market supply is P=Qs. Denoting firm level quantity by q, assume TC=50+4q+2q2 so that MC=4+4q. a) What is the market equilibrium price and quantity? Set demand equal to supply and find 100-4Q=Q, so Q=20, P=20. b) How many firms are in the industry in the short run? Perfectly competitiv ...

MODEL handout

... The Cobb-Douglas production function is: Q = A La Kb Rc If a+b+c > 1, then there are economies of scale or increasing returns to scale. If a+b+c < 1, then decreasing returns to scale exist. If a+b+c = 1, then constant returns to scale exist. In this last case (crs): the marginal product of labor = a ...

... The Cobb-Douglas production function is: Q = A La Kb Rc If a+b+c > 1, then there are economies of scale or increasing returns to scale. If a+b+c < 1, then decreasing returns to scale exist. If a+b+c = 1, then constant returns to scale exist. In this last case (crs): the marginal product of labor = a ...