Oligopoly Video-Kinked Demand Curve Questions File

... What happens to the quantity demanded for the firm that initiated the change in price? Why? ...

... What happens to the quantity demanded for the firm that initiated the change in price? Why? ...

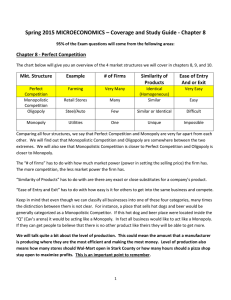

Chapter 8

... 1) All existing firms and potential entrants have identical costs. 2) Each firm’s costs do not change as other firms enter or exit the market (constant-cost industry). ...

... 1) All existing firms and potential entrants have identical costs. 2) Each firm’s costs do not change as other firms enter or exit the market (constant-cost industry). ...

Imperfect competition

... curves (as normal) The Super Normal Profits from the Short Run attract more firms into the market. They know about these profits, and there is nothing to stop them entering the industry. These can’t increase the supply of the specific brand in which the firm has a monopoly, but they can provide clos ...

... curves (as normal) The Super Normal Profits from the Short Run attract more firms into the market. They know about these profits, and there is nothing to stop them entering the industry. These can’t increase the supply of the specific brand in which the firm has a monopoly, but they can provide clos ...

lec10. markets

... over price. will cuts the AC curve at sell each extra unit its lowest point for the same price. because of the Price therefore = MR mathematical and AR relationship between marginal and average Output/Sales values. ...

... over price. will cuts the AC curve at sell each extra unit its lowest point for the same price. because of the Price therefore = MR mathematical and AR relationship between marginal and average Output/Sales values. ...

Perfect Competition Script

... *Is a hypothetical market form where no producer or consumer has the market power to influence prices. Certain conditions must be met *markets set the price *goods and services are perfect substitutes because all firms sell an identical product *everyone has equal access to technology and resources ...

... *Is a hypothetical market form where no producer or consumer has the market power to influence prices. Certain conditions must be met *markets set the price *goods and services are perfect substitutes because all firms sell an identical product *everyone has equal access to technology and resources ...

Chapter 7 - Humble ISD

... by lowering prices soon after the first seller announces the cut, but typically they prefer non-price competition ...

... by lowering prices soon after the first seller announces the cut, but typically they prefer non-price competition ...

Perfect Competition

... No individual firm or buyer, no matter how large their sales or purchases, can influence market quantity. ...

... No individual firm or buyer, no matter how large their sales or purchases, can influence market quantity. ...

232review packet cont+

... b. Each firm must face a horizontal demand curve. c. Firms are price-makers. d. Marginal cost equals average cost. e. Firms can increase sales by lowering their price. 4. Which of the following goods would be most likely to be produced a perfectly competitive firm (one characterized by perfect compe ...

... b. Each firm must face a horizontal demand curve. c. Firms are price-makers. d. Marginal cost equals average cost. e. Firms can increase sales by lowering their price. 4. Which of the following goods would be most likely to be produced a perfectly competitive firm (one characterized by perfect compe ...

Chapter 12 - Pegasus @ UCF

... 1. Revenues (TR) covers variable costs(TVC). In this case the firm produces where MR=MC If P>ATC, operate at economic profit If min AVC >P

... 1. Revenues (TR) covers variable costs(TVC). In this case the firm produces where MR=MC If P>ATC, operate at economic profit If min AVC >P

Homework Quiz 9

... c. May make a profit in the short run, but not in the long run. d. Will see substantial profits as long as it stays in the industry. e. Will be able to sell above average total cost. ...

... c. May make a profit in the short run, but not in the long run. d. Will see substantial profits as long as it stays in the industry. e. Will be able to sell above average total cost. ...