Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

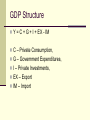

Why and How will global economic crisis effect Armenia's economy? Vahram Ghushchyan, Ph.D School of Corporate Governance 2009 Yerevan Global Economic Crisis Real estate market collapse in the US (2007-2008), Sharp increase in oil, gold, wheat and other commodities prices, Financial crisis in the US, Western Europe and Asia: Scarcity of financial resources, Large scale loses, Loss of customer confidence, Layoffs Fall of aggregate demand, Sharp decline in oil prices (Fall, 2008), Slow down of Russian Economy (Fall, 2008), Decrease in private transfers from Russia to Armenia (October 2008). Individual, non-commercial transfers from RF in 2008 ú ·á ëï ê» áë å ï »Ù µ» Ðá ñ Ïï »Ù µ» ñ Üá Û» Ùµ ¸» »ñ Ïï »Ù µ» ñ Ðá õÝ Çë Ðá õÉ Çë س Ðá õÝ í³ ö ñ »ï ñí ³ ñ س ñï ²å ñÇ É 70 60 50 40 30 20 10 0 -10 -20 ÛÇ ë Dynamics of private transfers from Russia in 2008 î áÏ áë³ ÛÇÝ ÷ á÷ áËáõÃÛáõÝ Ý³ Ëáñ¹ ï ³ ñí ³ ѳ Ù³ Ù³ ï The role of individual, non-commercial transfers from RF Tra nsfe rs from R F a nd U SA 1600 1400 Mln. USD 1200 1000 ² ØÜ è¸ 800 600 400 200 0 2004 2005 2006 2007 12% of GDP 15% of private consumption More than 40% of private investments 2008 Aggregate Demand (AD) and Aggregate Supply (AS) AS P AD1 AD2 GDP2 GDP1 Real GDP GDP Structure Y = C + G + I + EX - IM C – Private Consumption, G – Government Expenditures, I – Private Investments, EX – Export IM – Import Estimating the AD Yt Ct Gt I t EX t IM t Ct a0 a1W _ Put 1 a2W _ Prt 1 a3TR _ rust 1 a4TR _ rust a5TR _ usat 1 a6TR _ usat u1t Gt b0 b1Yt 1 b2 IM t 1 u2t I t c0 c1 int_ ratet c2W _ Put 1 c3W _ Prt 1 c4TR _ rust 1 c5TR _ rust c6TR _ usat 1 c7TR _ usat u3t EX t d 0 d1ex _ ratet 1 d 2 deflatort 1 d 3OilPt u4t IM t e0 e1deflatort 1 e2ex _ ratet 1 e3W _ Put 1 e4W _ Prt 1 e5TR _ rust 1 e6TR _ rust e6TR _ usat 1 e7TR _ usat u5t Three stage Least square I version II version Consumption Private sector average wages Transfers from the US (t-1) Transfers from the US (t) Transfers from RF (t-1) Time trend Constant 2.33* 4252.08** 4834.64** 2009.32* -4699.63* -70924.97* R2 0.84 2.18* 6.38* -3142.13* -67318.55* 0.85 Gov. Expenditures Imports Constant 0.87* -25694.52* R2 0.70 0.88* -26404.94* 0.70 Investments Discount Rate (CBA refinance rate) Transfers from RF (t-1) Transfers from RF (t) Time trend Constant -11856.88* 649.04* 1298.75* -1726.48* 40419.61* R2 0.84 1.86* 3.05* -56300.97* 0.86 Export GDP deflator (t-1) Constant -630.88* 97592.29* R2 GDP deflator (t-1) Transfers from RF (t) Time trend Constant R2 Number of observations 0.31 -594.05* 93776.33* 0.31 Import -611.8* 300.03* 361.12* 108341.6* 0.84* 456.89* 41454.44* 0.82 0.78 53 53 The impact of transfers from RF Increase of transfers from RF by $1 mln. in time t increase GDP by 1260.83 mln. drams in time t and an additional 2658.35 mln. drams in time t+1. Y C I G EX IM 1260.83 tr _ rus tr _ rus tr _ rus tr _ rus tr _ rus tr _ rus Y C I G EX IM 2658.35 tr _ rus _ 1 tr _ rus _ 1 tr _ rus _ 1 tr _ rus _ 1 tr _ rus _ 1 tr _ rus _ 1 Increase of transfers from RF by 1 dram in time t increase GDP by 2.95 drams in time t and an additional 8.24 drams in time t+1. Y C I G EX IM 2.95 TR _ rus TR _ rus TR _ rus TR _ rus TR _ rus TR _ rus Y C I G EX IM 8.24 TR _ rus _ 1 TR _ rus _ 1 TR _ rus _ 1 TR _ rus _ 1 TR _ rus _ 1 TR _ rus _ 1 Limitations Partial equilibrium, Labor Market, Data limitations (53 obs. only), From an average 30% growth trend to 30% decrease 60% deviation from previous trend, Stationarity. Simulations 10% decrease 20% decrease 30% decrease Years 2009 2010 2009 2010 2009 2010 GDP -36.06 -1.10 -50.29 -1.42 -64.51 -1.99 -26.28 0.00 -36.73 0.00 -47.19 0.00 -43.93 0.00 -65.69 0.00 -87.45 0.00 Expenditures -18.57 -4.35 -23.52 -4.63 -28.48 -4.95 Export -34.90 -11.52 -34.90 -11.52 -34.90 -11.52 Import -14.78 -2.75 -18.06 -2.86 -21.34 -2.98 Private Consumption Private Investments Gov. So, How to Fight the Crisis Simulate aggregate supply? It is a long time solutions: Simulate aggregate demand? Yes and sooner better: But How? Economic theory suggests the use of following tools: a) decrease taxes, b) increase government spending, c) use both tools together. So, How to Fight the Crisis What is the most efficient for Armenia? Increase government expenditures: What are the risks? Inefficient use of resources, Financing import: How to decrease risks and increase efficiency? Implement situation specific projects Can YOU be more specific please? Projects 1) Finance the private construction outside Yerevan. This will result in: Increase demand for domestic products, Decrease unemployment, Strengthening the tax collections in construction sector, Decrease regional disparity, 2) Expand Armenia’s competitiveness infrastructure: North-South highway and railway, 3) Concessional financing of SME’s ready to invest in R&D in construction sector. Financing of construction should be channeled trough mortgage fund. Its assets can latter be securitized, which will help to payoff the external borrowings.