Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

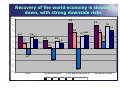

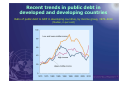

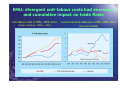

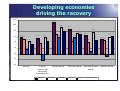

TRADE AND DEVELOPMENT REPORT, 2011 Post-Crisis Policy Challenges in the World Economy EMBARGO The contents of this Report must not be quoted or summarized in the print, broadcast or electronic media before 6 September 2011 17:00 hours GMT 2 Recovery of the world economy is slowing down, with strong downside risks 10 8.6 8.0 7.4 8 6.3 5.4 6 4.0 2 4.1 4.4 3.9 4 5.4 3.1 2.6 2.5 2.5 1.8 1.7 0.3 0 -2 -2.1 -4 -3.6 -6 -6.7 -8 World Developed countries 2007 2008 2009 South-East Europe and CIS 2010 2011 (forecast) Developing countries 3 The "two-speed recovery" continues Real GDP at market prices, 2002–2011 (Index numbers, 2002 = 100) World import volume, Jan. 2000–Apr. 2011 (Index numbers, 2000 = 100) Note: Linear trends correspond to 2002–2007. 4 Commodity prices have recovered amidst high volatility Monthly evolution of selected commodity prices, January 2002–May 2011 (Price indices, 2000 = 100) 5 Risks remain on the downside • The shift towards fiscal and monetary tightening represents a major risk of a prolonged period of mediocre growth in developed economies – if not of an outright contraction. • Given the economic weakness in developed economies and the lack of significant reforms in international financial markets, developing countries are vulnerable to trade and financial shocks (trade volumes; prices of primary commodities) 6 Fiscal imbalances were not a driving factor but a result of the crisis Government revenues and expenditure and fiscal balance, 1997–2010, in % of GDP 7 Recent trends in public debt in developed and developing countries Ratio of public debt to GDP in developing countries, by income group, 1970–2010 (Median, in per cent) 8 IMF-sponsored programmes systematically underestimate their negative impact on GDP growth and fiscal balances Growing out of debt • The best strategy for reducing public debt ratios is to promote growth and maintain low interest rates • Fiscal retrenchment seeking to cut fiscal deficit and thus "regain the confidence of financial markets" is likely to be self defeating, as it affects GDP growth and further reduces fiscal revenues. • Fiscal space for applying pro-growth policies is not a static variable: an expansionary fiscal policy generates higher fiscal revenues • To change the composition of public expenditure or public revenues can maximize their economic impact without necessarily modifying the total amount of expenditure or the fiscal balance • Fiscal expansion tends to be more effective if – higher spending takes precedence over tax cuts – spending targets infrastructure and social transfers – tax cuts target lower income groups (higher propensity for spending) 10 Financial deregulation was one of the main factors leading to the global crisis • Financial deregulation: – Led to a large, opaque and undercapitalized “shadow banking system” – Increased the concentration in the traditional banking segment in a few “to big to fail” (and “too powerful to regulate”) institutions – Reduced the diversity of the financial system and increased the systemic risk • While government regulation has weakened, its lender-oflast-resort support to the financial system has increased, and even extends to the shadow banking system. 11 Financial Re-Regulation and Restructuring • Strong re-regulation is urgently needed. It must: – Be tighter with the “too-big-to-fail” institutions – Cover the “shadow banking” and avoid regulation arbitrage – Incorporate a macro-prudential dimension, with anti-cyclical capital requirements and capital controls • In addition, the financial system must be restructured – Re-regulation alone will not orient credit to real investment or make it accessible to small and medium-sized firms – Banking restructuring should aim at more diverse financial systems, with a bigger role for public and cooperative institutions – Giant institutions must be sized down – The activities of commercial and investment banking should be clearly separated, in order to reduce the risk of contagion 12 The financialization of commodity markets has continued unabated Commodity investment, assets under management, 2005–2011 ($bn) 450 400 350 300 250 200 150 100 50 0 2005 2006 2007 2008 2009 2010-1st 2010-2nd 2010-3rd 2010-4th 2011-1st 2011-2nd quarter quarter quarter quarter quarter quarter Herd behaviour of money managers probably caused oil-price gyrations Ratio of money managers’ long and short positions and WTI-oil price, 2009–2011 20 120 18 110 100 14 90 12 80 10 70 8 60 6 50 4 40 2 0 06/01/2009 05/01/2010 Money manager positions 04/01/2011 Price (right scale) 30 24/05/2011 $ per barrel Ratio of long to short positions 16 Policy recommendations to improve commodity market functioning • Increase transparency in physical and derivatives markets • Arrange for internationally coordinated tighter regulation of financial investors • Consider occasional direct intervention to avert price collapses and deflate price bubbles 15 Exchange rates have become disconnected from macroeconomic fundamentals Real effective exchange rate, selected countries, January 2000–May 2011 (Index numbers, 2005 = 100, CPI based) 16 EMU: divergent unit-labour costs had enormous and cumulative impact on trade flows Unit labour costs in EMU, 1999–2010 Current-account balances in EMU, 1991–2010 (Index numbers, 1999 = 100) (Per cent of GDP) Chart 6.8 and Chart 6.9 Leaving currencies entirely to market forces entails considerable risks for both the global financial system and the multilateral trading system • Instead, a rules-based managed floating can deliver – sufficient stability of the real exchange rate to enhance international trade and facilitate decision-making on fixed investment in the tradable sector – sufficient flexibility of the exchange rate to accommodate differences in the development of unit labour costs or national inflation rates across countries • Such a system could be based in two approaches: – Adjustment of nominal exchange rates to inflation differentials. This would address more directly the need to avoid imbalances in trade flows. – Adjustment of nominal exchange rates to interest rate differentials. This is more directly related to limiting financial speculation in the currency markets. • This currency regime can be practiced as a unilateral exchangerate strategy but would be of greatest benefit to international financial stability if applied at multilateral level 18 Trade and Development Report 2011 Post-Crisis Policy Challenges in the World Economy Growth in developed economies remains very sluggish 6 4 4 3 2.9 2.4 2.3 2.1 1.8 1.9 2 0.5 0.4 0 -0.4 -2 -1.2 -2.6 -4 -4.2 -6 -6.3 -8 Japan 2007 United States 2008 2009 2010 European Union (EU-27) 2011 (forecast) 20 Developing economies driving the recovery 12 11.1 10 9 .4 8 .9 8 7.8 8 7.2 6 .9 7 6 5.9 5.9 5.6 5.4 5.9 4 .5 2 5.2 4 .8 4 .2 4 4 6 .4 6 5.8 5 4 .7 4 .4 6 .6 3 .5 1.8 1 0 -0 .8 -2 -2 .2 -4 Africa Latin Am erica and the Caribbean 2007 Eas t As ia 2008 2009 South As ia 2010 South-Eas t As ia 2011 (forecas t) Wes t As ia 21