Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Compounding wikipedia , lookup

Pharmacognosy wikipedia , lookup

Orphan drug wikipedia , lookup

Neuropsychopharmacology wikipedia , lookup

Epinephrine autoinjector wikipedia , lookup

Drug interaction wikipedia , lookup

Pharmacogenomics wikipedia , lookup

Drug discovery wikipedia , lookup

Neuropharmacology wikipedia , lookup

Pharmaceutical marketing wikipedia , lookup

Pharmaceutical industry wikipedia , lookup

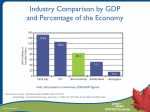

Biotechnology What is Biotechnology? bio—the use of biological processes; and technology—to solve problems or make useful products. Biotech in 21st century -- Using modern technology such as genetics, molecular biology to understand biological phenomenon in a new level of precision (at the cellular and molecular level), and solve problems or create product around that understanding Three major areas of Biotech Medical biotechnology (Red biotechnology) Some examples are the designing of organisms to produce antibiotics, and the engineering of genetic cures to diseases through genomic manipulation. Industrial biotechnology (White biotechnology) An example is the designing of an organism to produce a useful chemical. Agricultural biotechnology (Green biotechnology) An example is the designing of an organism to grow under specific environmental conditions or in the presence (or absence) of certain agricultural chemicals. “Financial Definition” of Biotech Companies in any of the three areas are technically biotech. Yet, for professional investors, “Biotech” is a buzz word that mainly associates with medical care sector (usually smaller) companies that uses new technologies. Industry at a glance There are 1,473 biotechnology companies in the United States, of which 314 are publicly held. Market capitalization: $311 billion as of mid-March 2004. Revenues: increasing from $8 billion in 1992 to $39.2 billion in 2003. Employed: 198,300 people as of Dec. 31, 2003. R & D: spent $17.9 billion on research and development in 2003. The top eight biotech companies spent an average of $104,000 per employee on R&D in 2003. 2003 Pharmaceutical Sales by Region World Audited Market 2003 Sales ($ billion) % of Global sales ($) % Growth (constant $) North America 229.5 49% 11% European Union 115.4 25% 8% Rest of Europe 14.3 3% 14% Japan 52.4 11% 3% Asia, Africa and Australasia 37.3 8% 12% Latin America 17.4 4% 6% $466.3 100% 9% TOTAL U.S. Government - Regulatory Body (FDA) - Public Health Care Programs - Medicare - Medicaid Position of US Biotech U.S. Health Care Industry Monitor and Regulate For Profit Health Benefit Providers Product Organizations Not-for-Profit Health Benefit Providers Service Organizations -Hospital management -Long term care -Etc. Biotech Pharmaceutical Companies Others Typical Value Chain of a Pharmaceutical Product using Biotechnology Discovery of Marketing of the Product the Product Typical Biotech vs. Pharmaceuticals Companies Biotech Pharmaceuticals Cap Size Small Big Balance Sheet /Cash Flow Cost Burn Cash ( - ) Strong Cash inflow R&D R&D, Manufacturing. Marketing Financing Almost all Equity Debt & Equity mixed Net Income Negative Positive Pipeline Strong Moderate/Weak Dividend None Moderate - Strong Investment Risk Very High Moderate Market Arthritis 46 million adults (non-institutionalized) in the U.S. (2003) 21% of adults (non-institutionalized) in the U.S. (2003) Cancer 23 million suffering worldwide. Estimated of 1.37 million people in the US will be diagnosed with cancer in 2005 about 1 in 3 lifetime risk; 38% of women and 43% of men The average cost of cancer treatment is well over $100,000 per person. Estimated $280 billion spent on treatment drugs for cancer annually. More than $100 Billions in US Diabetes Estimated 18.2 million people in the United States, or 6.3% of the population (2005) 165 million cases worldwide (2003) $132 billion spent in direct and indirect costs in America (2002) Heart Disease 25 million adults in the US Heart disease and stroke cost US around $214 billion annually. ($115 billion direct) (2002) Porter’s Competitive Force Political & Legal Forces • FDA External Force New Entrants LOW LOW-MID Power of Suppliers LOW Direct: Big Pharma End-user: Patients Substitutes MID-HIGH Biotech equipment firms Power of Buyers Barriers: Technology, Risk, Fixed Cost Non-biotech Drugs, Generic (future) Rivalry Competition mainly on function/quality instead of price US Regulatory Body - FDA Food and Drug Administration Sets health and safety standards Drugs, food , medical devices, cosmetics products, and biologics Also monitor for proper production standards Ensure labeling is truthful and informative. Pre Clinical Tests The beginning of the drug approval process To see the potential effects on humans, tests are performed on: Isolated tissues Cell Cultures Animals Company decides whether to put the drug into the human testing process, based on the marketability of the product, their financial situation etc. On average, only one compound in a thousand will actually make it to human testing The IND Filing The goal : provide pre-clinical data of sufficient quality to justify the testing of the drug in humans FDA has 30 days to review the IND application Must be filed annually until the completion of clinical testing At this time patents are usually applied for, patents last generally for 20 years About 85% of all IND applications move on to begin clinical trials If succeed, 20% chance of the product making it to the market Phase I Duration: 1 to 3 years Sample size: less than 100 patients Test on: Healthy volunteers If passed this Phase, chances of the product reaching to the market will be: ~30% Begins to analysis and develop the drugs safety profile How the drug is absorbed, metabolized and excreted Phase II Duration: ~2 years Sample size: 100 – 300 patients Test on: volunteers who suffer from the disease If passed this Phase, chances of the product reaching to the market will be: ~60% To evaluate the drug's safety and assess side effects Establishes the optimal dosage of the drug Phase III Duration: 3-4 years Sample size: >1000 patients Test on: volunteers who suffer from the disease If passed this phase, chances of the product reaching to the market will be: ~70% Verifies the drug’s effectiveness in its intended use Assessment of long term effects NDA Filing Upon desirable result from Phase III, New Drug Application (NDA) will be summit NDA contains data supporting the efficacy and safety of the drug Approval can take 2 month to several years, but average is around 18 to 24 months Drugs are subject to ongoing review, making sure no adverse side effects appear from the drug. After FDA’s approval, the drug can be marketed and distributed Patent Biotech inventions are subject to the same rules as all other inventions Generally last 20 years Since most companies file for patent during pre-clinical trail. Usually the patent is only good for another 10 years or so after it gained FDA approval What can be patented Product Method Use Examples DNA and RNA sequences Proteins, enzymes, antibiotics Antibodies, antigens Micro-organisms, cell lines, hybrids Phase IV Observational studies in an ongoing evaluation of the drug's safety during routine use Monitor any usage of the drug for conditions other than the approved medical indication Review & Approvals Key Points about the Clinical Process To bring a drug through all phases of the clinical trial process, it costs around: $350 - $500 millions 10-15 years Key factors that determine the quality of a company's pipeline: one or more successful products on the market a large pipeline of candidate drugs with some in late-stage enough cash to fund the development of their new drug candidates Review & Approvals 108 biotechnology medicines already approved and available to patients 324 biotechnology medicines in development either in human clinical trials or under review by the FDA for nearly 150 diseases 154 medicines for cancer, 43 for infectious diseases, 26 for autoimmune diseases and 17 for AIDS/HIV and related conditions Biotech in the Stock Market TECH BOOM AMEX BIOTECH INDEX vs. S&P 500 vs. NASDAQ 5 YEARS AMEX BIOTECH INDEX vs. S&P 500 vs. NASDAQ -S&P 500 -AMEX Biotech -NASDAQ Tech Bust Industry Financials U.S. Biotech Industry Statistics: 1994–2004* 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 Sales* 33.3 28.4 24.3 21.4 19.3 16.1 14.5 13 10.8 9.3 7.7 Revenues 46.0 39.2 29.6 29.6 26.7 22.3 20.2 17.4 14.6 12.7 11.2 R&D Expense 19.8 17.9 20.5 15.7 14.2 10.7 10.6 9.0 7.9 7.7 7.0 $0.59 $0.63 $0.84 $0.73 $0.74 $0.66 $0.73 $0.69 $0.73 $0.83 $0.91 6.4 5.4 9.4 4.6 5.6 4.4 4.1 4.5 4.6 4.1 3.6 No. of Public Companies 330 314 318 342 339 300 316 317 294 260 265 No. of Companies 1,444 1,473 1,466 1,457 1,379 1,273 1,311 1,274 1,287 1,308 1,311 Employees 187,5 00 177,0 00 194,6 00 191,0 00 174,0 00 162,0 00 155,0 00 141,0 00 118,0 00 108,0 00 103,0 00 Year R&D/ $ Sales Net Loss *Amounts are U.S. dollars in billions. Sources: Ernst & Young LLP, annual biotechnology industry reports, 19932005. Financial data based primarily on fiscal-year financial statements of publicly traded companies. Industry Financials Biotech Industry Net Loss / $ Sales $0. 50 $0. 45 $0. 43 $0. 47 $0. 39 $0. 44 $0. 35 $0. 40 $0. 35 $0. 29 $0. 30 $0. 25 $0. 28 $0. 21 $0. 27 $0. 20 $0. 19 Towards Breakeven ($0 loss/$ Sales) $0. 19 $0. 15 $0. 10 $0. 05 $- 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 Industry Ratios Market Cap P/E ROE % Long-term Net Profit P/B Debt/Equity Margin% (mrg) P/FCF (mrg) From Yahoo Finance Nov 10, 2005 Sector: Health Care Industry: Biotech 2208.2B 21.91 14.43 0.01 9.93 11.05 457.4 326.6B (-) 1.7 0.00 2.80 11.33 3035. 6 Amgen Inc. Genetech Inc. 99.0B 28.90 17.55 0.19 30.66 4.82 N/A 98.5B 87.85 15.61 0.27 20.52 12.82 52.11 Gilead Sciences Inc. Biogen Idec Inc. Medlmmune Inc. 23.5B 37.87 32.02 0.00 36.32 8.97 N/A 19.2B 107.52 4.29 0.00 36.33 3.86 N/A 14.5B 111.02 1.98 0.01 4.56 2.11 220.3 1 Cash Total Financing Key Issues Concerning the Future of the Industry Generic Competition Changing Social & Legal Environment Blockbuster Model vs. Personalized Health Care Biotech and Big Pharmas: New Collaborative Dynamics Generic competition Currently no bio-generic in the US market Technological difficulties Biotech companies argues: Biotech drugs are not defined by molecular make up but the production process Difficult but possible (they exist in China & Latin America, up and coming in Europe) Regulatory difficulties 1. 2. No clear regulatory guidelines to permit the production of generic biologics in the US Two challenges How to prove that a generic biologic is chemically and therapeutically equivalent to the original? Who is the proper authority regarding the biogenerics? – The law that is written to regulate generic drugs does not include bio-generic Generic competition Bio-generics are very likely to come in the future BUT they most likely will face stricter pre-approval testing requirements than chemically based generics More costly to produce and therefore less price difference between original & generic Changing Social & Legal Environment Pressure from the public and governments worldwide to contain drug prices In Sept 2004, Merck’s Blockbuster, Vioxx, was pulled off the market Studies found the drug to increase the risk of heart attacks and strokes if used longer than 18 months Pfizer's Bextra, which is in the same drug class (Cox-2 inhibitors) was also dropped out later So far, ~4,000 lawsuits has filed against Merck on Vioxx Investors panicked over closer scrutiny and tighter regulation towards the pharmaceutical and biotech industry Social & Legal Environment: Drug Safety Issues The Downside Cash burning biotech are vulnerable to higher testing cost and delay in the approval process The Upside Biotech generally focus on life-threatening disease, where side-effects are more tolerable New Technology can evaluate safety earlier in the development process and even prior to clinical trials E.g. Pharmacogenomics Higher safety standard will benefit the industry in the long run Blockbuster Model vs Personalized Health Care The Blockbuster model Blockbuster - A medicine with sales over $1billion The model: Find treatments for disease with the biggest market Pool resources on breeding the few potential blockbuster Pros: Hitting ‘the Jackpot’ Cons Attract competition Relay heavily on blockbuster Blockbuster Model vs Personalized Health Care The Future: Personalized Health Care Individualized Drugs Using New Diagnostic Equipment Business Model Lots of small but high-margin markets Pros Lower safety risk Less exposure to competition Relatively shorter approval time and lower research cost due to smaller scale of tests are needed Diversified Risk Cons Less overall margin Biotech and Big Pharmas: New Collaborative Dynamics Traditionally big pharmas are often in a stronger position when negotiating licences from biotech to market their drugs. Yet, big pharmas’ pipeline are getting weaker due to their focus on developing and marketing in recent years Of the drugs approved in 2004, more originated in biotech labs than in the labs of big pharma. Biotech pharmaceuticals accounted for over $42.1 billion in 2004 worldwide sales Biotech drugs account for 25% of the total active pipeline Of the 305 biotech projects of the top 10 pharmas, 63 % were inlicensed. Biotech and Big Pharmas: New Collaborative Dynamics 2004 Merger & Acquisition On the other hand, biotechs are growing bigger and the industry is consolidating As a result, Big Pharms now: 1. 2. 3. Seeks more partnerships with biotechnology companies Willing assume risk and enter partnerships at earlier stages in the drug development process Pays more to acquire biotech pipelines The Future Industry Maturing - From potential to performance Managements are becoming more skilled in the business instead merely focusing on the technology More consolidation Big pharma’s weak pipeline gives biotechs more bargaining power The days of investing merely on ideas/stories are gone, investors now look for companies with real profitable products with growth potential The Future From Potential to Profitability Industry is estimated to achieve the first net income in its 30year history in 2008. Future Challenges and Opportunities Bio-generic (especially in the international market) Tightening regulation and public concerns Shifting from blockbuster driven to the personalized health care model The Biotech Stock Picking System Successful Product(s) Solvency Quantity of Pipeline Quality of Pipeline Management Collaborations R&D Successful Product(s) 2. Worth Looking into Makes an okay biotech to a good one Best to have one or more established drug already generating cash for the business Solvency 1. Strong Sell if neither MUST have enough cash to “burn” for its R&D until it gets a drug into the market that can generate sufficient income to sustain the business (look at burn rate) If not, it MUST have a SECURED source of financing (e.g. collaboration with a big pharma) The Biotech Stock Picking System Quantity of Pipeline Quality of Pipeline Proven track record of taking a drug through the regulatory hurdles and/or to the marketplace A good mix of executives specialized in technology and business Collaborations Drugs in pipeline should be 1)Diversified and 2)Aimed at markets that is both large and under-serviced. Management Plenty of drugs in the pipeline with at least two ore more in later clinical trials (Phase 2 or 3) 1) Marketing and Developing partnership pharmaceutical companies 2) Research collaboration with corporate or academia partner (e.g. University) Research & Development Growing R&D spending and growing or sustaining R&D/$ Sales Inspired science. Defining moments. Amgen Inc. (AMGN) • “Applied Molecular Genetics Inc” • Specializes in molecular and cellular biology • Produces and markets therapeutic products for the treatment of nephrology, cancer, inflammatory diseases, metabolic and neurodegenerative disorders • 1st : sales • 2nd: market capitalization ($99b) History Initial Public Offering 1983 1980 Established sales surpass $1b 1992 1989 FDA approves EPOGEN® Now Sales surpass $10.5b Five Blockbusters CEO Of The Year -- Medicine Man Kevin Sharer In terms of innovation and commercialization, Amgen and his [Sharer's] leadership clearly are a model." Leadership Team Hassan Dayem, Ph.D Senior vice president and chief information officer since 2002; Vice president, Information Servicesand chief information officer at Merck & Co., Inc. from 1997 to 1998. Dennis M. Fenton, Ph.D. Executive vice president from 2000. Joined Amgen since 1988. Brian McNamee Senior vice preside, Human Resources from 2001. Vice president of Human Resources at Dell Computer Crop from 1999 to 2001. Various human resources positions since 1988. George Marrow Executive vice president of Worldwide Sales and Marketing since 2001 and became executive vice president, Global Commercial Operations in April 2003. Various management positions since 1993. Richard Nanula Executive vice president and chief financial officer since 2001. Various management positions since 1986. Roger M. Perlmutter, M.D., Ph.D. Executive vice president of Research and Development since 2001. Executive vice president, Worldwide Basic Research and Preclinical Development of Merck Research Laboratories. David J. Scott Senior Vice president, general counsel and secretary since March 2004. Senior vice present and general counsel of Medtronic, Inc from 1999 to 2004. Stock Price - AMGN • • • • • Stock price: $79.89 (as of Nov7, 2005) # of outstanding shares: 1,234 millions Exchange: NASDAQ Volume: 7,518,000 Zero Dividend Policy • Headquarters: California • Staff employed: more than 14,000 • Mission: To serve patients Successful products on the market Blockbusters Strategy: often target medical problems that haven't received much attention from the pharmaceutical industry EPOGEN® Aranesp® NEUPOGEN® Neulasta® ENBREL® Stimulate the production of red blood cells to treat anemia Selectively stimulate the production of neutrophils, one type of white blood cell that helps the body fight infections Blocks the biologic activity of tumor necrosis factor (TNF) by competitively inhibiting TNF, a substance induced in response to inflammatory and immunological responses, such as rheumatoid arthristis and psoriasis billions Revenue Composition 12 10 8 6 4 2 0 2000 EPOGEN NEUPOGEN 2001 2002 Aranesp ENBERL 2003 2004 Neulasta Others Sales Breakdown (as at Sep 2005) Others- 2% Enbrel-21% EPOGEN-21% NEUOGEN-10% Neulasta-19% Aranesp-27% Solid: US Dot pattern: international International Sales 12000 10000 8000 6000 4000 2000 0 2000 2001 US 2002 2003 International 2004 A deep product pipeline with late-stage candidates Other Principle Products • Kineret • Kepivance™ • Sensipar® rheumatoid arthritis chronic kidney disease mouth sores bought Potential Candidates • Panitumumab • AMG 162 colorectal cancer ($1 billon market) osteoporosis (bone loss) and possibly also bone cancer 2002 1991 2002 2004 1998 1999 2003 2002 2004 2001 2004 2001 1989 Positive Developments • July 4 FILLING UP AMGEN'S PIPELINE • encouraging early data on osteoporosis and cancer drugs • 10 more are ready for human testing • predicts Amgen will apply for FDA approval for four products in the next five years. • Amgen also periodically seeks government approval to use an existing product to treat additional maladies. Negative Developments • Lack of expertise in small molecule and immunotherapeutics development • Heavy reliance on Aranesp and Enbrel Marketing Financial Analysis 2005 results • First Quarter 2005 GAAP Earnings Per Share of 67 Cents • Total Product Sales Increased 24 Percent • 2005 Guidance Increased for Total Revenue and Adjusted EPS from the previous range of $2.70 to $2.85 to a range of $2.80 to $2.90 • Second Quarter 2005 GAAP Earnings Per Share Increased 44 percent to 82 Cents • 2005 Revenue Growth Guidance Raised to Mid-to-High Teens • 2005 Adjusted Earnings Per Share Guidance Increased to a Range of $3.10 to $3.20, a Growth Rate of 29 to 33 Percent • Third Quarter 2005 GAAP Earnings Per Share slipped to 77 cents • Product Sales Growth of 19 Percent Driven by Sales of Aranesp, Neulasta and Enbrel Income Statement Year 2004 As a % revenue / operating expense YOY growth 5-year growth Product Sales 95% 27% 228% Cost of Sales 24% 29% 331% R&D 28% 23% 146% S,G&A 35% 31% 291% Income 22% 4.6% 115% • Write-off of acquired in-process R&D • Amortization of acquired intangible assets • Diluted EPS: 2.26 (Sept 2005) • ROE: 17.55% (Sept 2005) Since 2002 Income Statement Hundreds *Sudden drop in 2002 was due to write off acquired IPR&D of Tularik and Immunex 200 150 2 8% 9% 47% 51% 26% 100 1 50 0.5 0 -50 1.5 0 2000 2001 2002 2003 2004 -0.5 -100 -1 -150 -1.5 EBIDTA Gross Profit Sales EPS Cost Structure 8000 7000 6000 5000 4000 3000 2000 1000 0 2000 R&D 2001 2002 Cost of Sales 2003 S,G&A 2004 Write off Balance Sheet • Cash/share = 5,551/1,234 =$4.5 • Intangible assets: 4,802 (Dec 2002) • Goodwill: 9,871(Dec 2002) – acquisition of Immunex – >Total assets increases 279% • D/E: 20% (Sept 2005) Cash flow Statement • Growth in operating is mainly contributed from growth in products sales • Heavy write off of acquired in-process research and amortization • Most of the investing is on manufacturing expansion • Repurchase of CS and issuance of debt • Free CF: 3,697-1,336=2,361 millions Cash Flow Statement 5000 4000 3000 2000 1000 0 -1000 -2000 -3000 -4000 -5000 -6000 2000 2001 2002 2003 2004 Operating Investing Financing Free CF R&D Productivity Product Candidates 1) Internal research 2) Acquisitions (Tularik & Immunex) 3) Licensing from and collaborations with 3rd parties 1) Internal Research - Rich Pipeline • Invest at least 20% of product sales in R&D each year since 1994 • 40 compounds undergoing preclinical or patient trials 2) Acquisitions • Acquisitions have contributed to Amgen's growth history. • • • • 1994 2000 2002 2004 Synergen Inc Kinetix Pharmaceuticals Inc Immunex Corporation Tularik Inc Collaborations • More than 100 active collaborations Amgen Ventures • offer early stage companies access to Amgen's extensive capabilities while providing Amgen with insight into external research innovations • pave the way for future collaborations Joint Venture • 50-50 joint venture with Kirin (KA) Licensing • Johnson & Johnson – PROCRIT Co-promotion • Wyeth – ENBREL • outside US – Aranesp, Neulasta, NEUPOGEN, ENBREL Current patents & patent applications Patent Expiry • Epogen • Neupogen • Epogen • Neupogen 2004 2006 Aranesp Neulasta Next generations! Other Issues Stock Option Expense Effect on EPS: -6% 5 year: AMGN vs. AMEX Biotechnology News • 2000-2001. Slow in moving the product pipeline; no significant innovation • Late 2001. Introduction of Aranesp (blockbuster) • 2002. Acquisition of one of the top tier in biotech :Immunex (expanded pipeline: Enbrel and Kineret) • 2003-2004. Patent expiration in one of the blockbuster: Epogen 1 year NEWS • April: reduced uncertainty about proposed changes in certain Medicare reimbursement policies • 16% Rise in July: Amgen's submission to the magazine's Editorial Advisory and Securities Review Committee • 7% Rise Recently: successful cancer treat test (Panitumumab) Capital Expansion Manufacturing • Global leader in biotech manufacturing • Producing more than 1/3 of the world’s output of nonvaccine and non-insulin protein therapeutics Investing in Future Growth… plans to invest billions of dollars in capital projects to expand its capabilities • Colorando • Puerto Rico • Rhode Island Marketing Strategy • Retention of marking rights to products in development i.e. Epogen and Neupogen Customer & Market • Top 3 wholesalers – AmerisourceBergen Corp (32%) – Mckesson Corporation (15%) – Cardinal Distribution (15%) • Direct sales to health care providers in US, Europe, Canada and Australia: – Clinics – Hospitals – Pharmacies Reliance on Supply • Limits on supply for ENBREL® • Certain of raw materials, medical devices and components are single-sourced from third parties Recognitions • 1st in Pharmaceutical Executive Industry Audit • 2nd in Science’s 2005 Top Biotech and Pharma Employers Survey The Biotech Stock Picking System – Successful Product(s) – Solvency – Quantity of Pipeline – Quality of Pipeline – Management – Collaborations – R&D Recommendation BUY! (long-term investment) Genentech In Business for Life Company Background Stock Price: US $93.98 (on Nov. 09, 2005) Ticker Symbol: DNA – N Workforce: 8300 employees Location: South San Francisco Outstanding Shares: 1,056,450,000 5-yr Stock Price Aty 1-yr Stock Price Aty Company History World’s 2nd largest biotechnology company 1976, Genentech was founded in 1976 by venture capitalist Robert A. Swanson and biochemist Dr. Herbert W. Boyer. Robert Swanson Dr. Herbert Boyer History 1980, went public. – Successfully raised $35 million for Genentech. 1990, Acquired by Roche Holding (Switzerland) - a $2.1 billion merger. 1999, Roche reissued Genentech shares – Genentech (ticker symbol DNA) returned to the NYSE – Started at $97 and closed at $127. – The largest public offering in the history of the US health care industry Top Executives CEO Executive Officers Arthur D. Levinson, Ph.D. (joined in 1980) Chairman and Chief Executive Officer Ian T. Clark (joined in January 2003 ) Senior VP, Commercial Operations Bachelor of Science degree in bilogoical sciences department Susan Desmond-Hellmann, M.D., M.P.H. (joined in 1995) President, Product Development David A. Ebersman, (joined in 1994) Senior Vice President, CFO Bachelor of Arts in Economics and International Relations. Stephen G. Juelsgaard, D.V.M., J.D. (joined 1985) Executive VP, General Counsel and Secretary (doctorate veterinary medicine, master of Science degree and Law degree ) Richard H. Scheller, PhD (joined 2001) Executive VP, Research Patrick Y.Yang, Ph.D. (joined 2003) Senior VP, Product Operations Mission and Values “ Our mission is to be the leading biotechnology company, using human genetic information to discover, develop, manufacture, and commercialize bio-therapeutics that address significant unmet medical needs. We commit ourselves to high standards of integrity in contributing to the best interests of patients, the medical profession, our employees and our communities, and to seeking significant returns to our stockholders, based on the continual pursuit of scientific and operational excellence.” Growth Strategy outlined for 1999 to 2005 The 5X5 goals that outlined in 1999 and hopes to achieve by the end of 2005: 1. 25 % average annual non-GAAP EPS growth 2. 25 % non GAAP net income as a percentage of operating revenues 3. 5 new products/indications approved 4. 5 significant products in late-stage clinical trials 5. $500 million in new revenues from strategic alliances or acquisitions Major Stakeholder- Roche At Dec 31, 2004, Roche’s ownership % was 56.1% At Sept 30, 2005, Roche’s ownership % was 55.5% Affiliation agreement shows: – – upon Roche's request, DNA will repurchase share of the common stock to increase Roche's ownership to the Min %, 55.7% Roche has a continuing option to buy stock from DNA at prevailing mkt prices to maintain its % owner interests. Products 1. Oncology cancer treatment 2. Immunology immune disorder 3. Vascular Medicine heart disease 4. Specialty Biotherapeutics other areas Product Approval Timeline Revenue Composition Avasitin – 14.80% Herceptin – 12.88% Growth Hormone 9.44% Thrombolytic 5.33% Xolair -5.% Pulmozyme – 4.8% Rituxan – 45.64% In 2004, Genetech: Entered into 3 partnerships Received 2 product approvals Launched 2 breakthrough oncology products : Avastin + Tarceva Saw promising results in numerous clinical trials Add 13 new projects to it development pipeline Delivered substantial growth Continued to receive recognition as the best place to work in 2004 Development Pipeline Information updated November 2005 Awaiting FDA Action Rituxan® Hematology/Oncology Frontline intermediate grade or aggressive NHL Rituxan® Immunology Refractory rheumatoid arthritis Development Pipeline FDA Filing Preparation Avastin® Metastatic breast cancer Non-small cell lung cancer Second line colorectal cancer Herceptin® Adjuvant breast cancer Metastatic breast cancer in combination with Taxotere Development Pipeline PHASE III Avastin Refractory Ovarian Cancer* Xolair Pediatric Asthma Lucentis Wet age-related macular degeneration Rituxan® Hematology/Oncology Relapsed chronic lymphocytic leukemia Rituxan-Immunology ANCA-associated vasculitis Lupus nephritis* Moderate-to-severe rheumatoid arthritis* Primary progressive multiple sclerosis Systemic lupus erythematosus Tarceva® Adjuvant non-small cell lung cancer* Tarceva® +/- Avastin® Second line non-small cell lung cancer Development Pipeline PHASE II 2nd Generation AntiCD20 Rheumatoid arthritis Apo2L/TRAIL Cancer therapy* Avastin® +/- Tarceva® Non-small cell lung cancer Omnitarg™ Ovarian cancer Raptiva® Adult atopic dermatitis* Rituxan® Immunology Relapsed remitting multiple sclerosis Topical VEGF Diabetic foot ulcers* Xolair® Peanut allergy Development Pipeline PHASE I Anti-NGF Acute and Chronic Pain BR3-FC Rheumatoid Arthritis* Tropical Hedgehog Antagonist Basal Cell Carcinoma* Important Products Introduction Avastin - New Tarceva - New Rituxan – 15% sales increase Herceptin – 13.6% Activase, TNKase, and Cathflo Activase – 8% Avastin – Oncology Avastin Anti-VEGF antibody For use in combination with intravenous 5Fluorouracil-based chemotherapy as a treatment for first-line metastatic colorectal cancer In 2004, Avastin launch was the most successful oncology therapeutic in US. The total sales of the 1st 10 month in US was 545 M, which exceeded the full year sales of any other product in the therapeutic area by about 175 M. In the 1st half 2005 sales of Avastin where 464 M compared with 171 million in first half 2004. Tarceva – Oncology approved Nov. 18, 2004 Small molecule HER1/EGFR inhibitor For use as an oral tablet for the treatment of patients with locally advanced or metastatic non-small cell lung cancer after failure of at least one prior chemotherapy regimen The only drug in epidermal growth factor receptor class to demonstrate an increase in survival I advanced non-small cell lung cancer patients in a phase Ii clinical trial Rituxan – Oncology Anti-CD20 antibody approved for the treatment of patient with relapsed or refractory low-grade or follicular, CD20 positive, Bcell non-Hodgkin's lymphoma One of Genentech top-selling drugs in 2004 In 2004, Sales of 1.71 B, 14.9% increase In first half of 2005, 890.8 M, 18.5 % increase compare with first half of 2004 Marketed in US by Genentech and Biogen Idee by Zenyaku in Japan Herceptin Anti-HER2 antibody For metastatic breast cancer in HER2 over expressed tumors No. 3 best-selling drug to the company In 2004, sales of 484 M, a 13.6% increase In the first half of 2005, sales of 291.1M, a 25.9% increase Marketed by Genentech in US, and Roche in the rest of the world 3 Vascular Drugs Activase, TNKase, and Cathflo Activase In 2004, total net sales of 200M, an increase of 8% compared with 2003 in the first half of 2005, sales of the 3 drugs were 106.9M, up 9.3% increase Activase In 2004, approved for treating heart attacks, acute ischemie stroke and massive pulmonary embolism The 1st drug to be indicated for the mngt of stroke Cathflo Activase® TNKase™ Cathflo Activase Thrombolytic agent For the restoration of function to central venous access devices as assessed by the ability to withdraw blood On Jan 4, 2005, approved by FDA for catheter clearance in pediatric patients TNKase Single-bolus thrombolytic agent For the treatment of acute myocardial infarction (AMI) Licensed Products receive royalty revenue under license agreements based on technology developed by us or on intellectual property to which Genentech has rights. products are sometimes sold under different trademarks or trade names. Significant licensed products, representing 94% of our royalty revenues in 2004 Licensed Products Sales Revenue Composition Avasitin – 14.80% Herceptin – 12.88% Growth Hormone 9.44% Thrombolytic 5.33% Xolair -5.% Pulmozyme – 4.8% Rituxan – 45.64% Product Sales Each Product Revenue Growth Each Product Revenue Growth Each Product Revenue Growth General Growth Royalties income In 2003, increase 37% to 500.9M In 2004, Increase 28% to 641.1 M Reasons: – – Due to higher 3rd Party sales by various licensees, mainly Roche (Rituxa + Herceptin) Increase of ex rate of Euro dollars Contract Revenue In 2003, increased 226% to 177.9M In 2004, increased to 30% to 231.2M Reason: – – – – – Driven from the collaborators for $$ earned on development efforts related to Lucentis, Rituxan Immunology Commercialization of Terceva New drug, Avastin Research and Development In 2003, R+D expense increased 16% to 722M In 2004, it increased 31%, In 2004, it’s a % of operating revenue was 21% Balance Sheet 2004 2003 Net mkt Value of Asset – increase 9403.4M 8736.2M Price/Book Value Increase 11.23 7.09 Income Statement 2004 2003 1.Sales Revenue Increase = 43 % 3.75B 2.8B Free Cash flow Increase 546 M 915 M Net Earning – increase 784.8 M 610.2 M Cash Flow Statement 2004 2003 Operating CF (increase) 1195.8 M 1236.9 M Financing CF (decrease) -846.3 M 325.5 M Investing CF (increase) -451.6M -1398.4 M Key Ratios 2004 2003 2002 2001 2000 P/B 11.23 3.76 1.59 2.42 3.77 P/E 88.92 81.08 217.80 185.79 -- Current Ratio 3.447 3.10 3.22 3.35 3.96 Net Profit Margin % 22.0 18.49 2.47 7.63 -0.10 ROE % 12.8 8.07 0.93 2.11 -1.13 Price/Book Value – 5yrs Trend 12 11.23 10 8 6 4 P/B 3.77 3.76 2.42 2 1.59 0 2000 2001 2002 2003 2004 Price/ Equity Ratio – 5yrs Trend 250 217.8 200 185.7 150 P/E ratio 100 81.08 88.92 50 0 2000 2001 2002 2003 2004 Current Ratio – 5yrs Trend 3.96 3.25 3.22 3.1 3.47 20 04 20 03 20 02 Current Ratio 20 01 20 00 4.5 4 3.5 3 2.5 2 1.5 1 0.5 0 Net Profit Margin % - 5 yrs trend 25 22 20 18.49 15 10 Net Profit Margin % 7.63 5 2.47 0 -0.1 2000 2001 -5 2002 2003 2004 ROE % trend 14 12.8 12 10 8.07 8 6 4 2 2.11 0 -1.13 2001 -22000 0.93 2002 2003 2004 2005 Q1 – Q3 Product Sales R+D Expenses Operation Costs Liquidity + Capital Resources CF Statement New Projects Recent News Stock Price information In 2005, Product Sales In 2005, Operation Cost In 2005, R+D Expense In 2005, Liquidity + Capital Resources Cash Flow Statement New Projects In 2004, addition of 13 projects to the pipeline 6 of which are new molecular entities: – – – – – Anti-NGF for acute and chronic pain, BRS-Fc for rheumatoid arthrities A tropical Hedgehog antagonist for basal cell carcinoma A tropical vascular endothelial growth factor for diabetic foot ulcers Two other undisclosed molecular entities Recent News In November 2005, the FDA approved Tarceva® (erlotinib) in combination with gemcitabine chemotherapy for the treatment of advanced pancreatic cancer in patients who have not received previous chemotherapy. Tarceva is the first drug in a Phase III trial to have shown a significant improvement in overall survival when added to gemcitabine chemotherapy as initial treatment for pancreatic cancer. Recent News On November 7, 2005, Genentech announced that preliminary data from a Phase III trial showed Lucentis™ (ranibizumab) is the first investigational therapy to demonstrate clinical benefit over photodynamic therapy in a head-to-head study of patients with wet age-related macular degeneration. Beat the QLT down (a Canadian based BioTech firm ) Recent Stock Price Nov 9, 2005, DNA stock price: 94.88 USD The Biotech Stock Picking System Successful Product(s) Solvency Quantity of Pipeline Quality of Pipeline Management Collaborations R&D Recommendation Hold ! Celgene The Top Management Team John W. Jackson Chairman and Chief Executive Officer Has been Chairman of the Board and Chief Executive Officer since January 1996 and a member of the Executive Committee of the Board of Directors. Sol J. Barer President and Chief Operating Officer Has been the President since October 1993 and the Chief Operating Officer and one of the directors since March 1994 and a member of the Executive Committee of the Board of Directors. Robert J. Hugin Chief Financial Officer Has been the Senior Vice President and Chief Financial Officer since June 1999 and was elected to serve as a director in December 2001. ABOUT THE COMPANY • Initially a unit of the Celanese Corporation in 1980. • spun off as an independent biopharmaceutical company in 1986. Very Convenient • Specializes in the discovery, development, and commercialization of orally administered drugs for the treatment of cancer and inflammatory diseases via gene regulation. • Have two main subsidiaries, 1.Signal Pharmaceuticals (formed in 2000) 2.Celgro. Snapshot • • • • • Stock price: $58.28 (as of Nov10, 2005) # of outstanding shares: 167.9 Million Dividend: always 0 Market Capitalization: 9.78 Billion Earning Per Share: $ 0.51 ABOUT THE COMPANY Major Products in the Market • THALOMID approved by FDA in July of 1998. • Ritalin® family & FOCALIN series FOCALIN approved by FDA in November 2001. FOCALIN XR (extended-release capsules) approved on May 27, 2005 • ALKERAN in-licensed from GlaxoSmithKline for distribution in the US in March 2003 to distribute, promote, and sell ALKERAN. These are the current major Revnue Drivers THALOMID® No.1 Revenue Driver What does it do? • Initially approved as the treatment of moderate to severe Erythema Nordosom Leprosum (ENL) and maintenance therapy for prevention and suppression of the disease. • Its function has been expanded to treat various types of cancers. • Also it is under development as a potential treatment for various serious chronic illnesses, such as: In 2003 the National Comprehensive Cancer Network guidelines recommended the combination of THALOMID and dexamethasone as the first-line standard of care for newly-diagnosed myeloma patients. On October 22, 2004, Celgene received an approvable letter from the FDA relating to its THALOMID® multiple myeloma (or MM) supplemental new drug application, or sNDA. S.T.E.P.S.® - Celgene's Innovative Restricted Distribution Program What is it? • S.T.E.P.S.® stands for System for Thalidomide Education and Prescribing Safety. • Since its inception, nearly 115,000 individuals have taken advantage of Celgene’s S.T.E.P.S.® program. • A blueprint for pharmaceutical products that offer life-saving or other important therapeutic benefits but have potentially problematic side effects. • THALOMID(R) is the first drug approved under a special "Restricted Distribution for Safety" regulation. • The system is included as part of the THALOMID prescribing information and was developed to prevent fetal exposure to THALOMID. • S.T.E.P.S. intellectual property estate includes five U.S. patents expiring between the years 2018 and 2020 Prescription for THALOMID must go through the S.T.E.P.S.—Mandatory RETALIN® family & FOCALIN series No.2 Revenue Driver What does it do? FOCALIN • a refined form of Ritalin that offers tolerability and dosing advantages over the parent drug. • For the treatment of attention deficit disorder and attention deficit hyperactivity disorder (ADHD) in children and adolescents. FOCALIN XR • is long-acting version of FOCALIN and is for the treatment of Attention-Deficit/Hyperactivity Disorder (ADHD) in adults, adolescents, and children. ADHD is one of the most common psychiatric disorders of childhood and is estimated to affect five to seven percent of children and approximately four percent of the adult population in the U.S. ALKERAN No.3 Revenue Driver What does it do? A therapy for the palliative treatment of • multiple myeloma (Since the therapy was first introduced in 1962, ALKERAN has remained a standard treatment for the management of MM.) • non-resectable epithelial carcinoma of the ovary. In the 2004 American Society of Hematology meeting, clinical trial data was presented. In combination with other anti-cancer therapeutics, including THALOMID(R) (the #1 revenue driver), ALKERAN(R) was a key component of several investigational MM studies which reported positive results. REVLIMID The Potential Product Recent News WASHINGTON, Sept 14, 2005 /PRNewswire-FirstCall via COMTEX News Network/ -- Celgene Corporation announced that the Oncologic Drugs Advisory Committee (ODAC) of the U.S. Food and Drug Administration (FDA) recommended full approval of REVLIMID for the treatment of patients with transfusion- dependent anemia due to low- or intermediate-1-risk myelodysplastic syndromes (MDS) associated with a deletion 5q cytogenetic abnormality with or without additional cytogenetic abnormalities. REVLIMID A current cost driver but a Potential Revenue Driver What does it do? • A leading IMiD IMMUNOMODULATORY DRUGS (in clinical trials) • A potential treatment for myelodysplastic syndromes (MDS) and multiple myeloma affect approximately 300,000 and 200,000 people worldwide, respectively. • It offers “Transforming Potential” in Hematological Cancers. • It is being evaluated in more than 30 blood cancers and solid tumors. • Taken orally as capsules very convenient ABOUT THE COMPANY Other Current Researches • • • • • • • Other IMiDs® : ACTIMID™, (CC-11006) PDE4 & TNF-alpha Inhibitors Benzopyrans Kinases Inhibitors Tubulin Inhibitors Ligase Modulators Stem cells Programs These are the current major Cost Drivers The Product Pipeline The core programs: • ACTIMID™ • (CC-11006) • PDE4 & TNF-alpha Inhibitors Other investigational compounds: • Benzopyrans • Kinases Inhibitors • Tubulin Inhibitors • Ligase Modulators • placental • cord blood derived stem cell programs ABOUT THE COMPANY • The company has been running negative since its “independence” in 1986, until 2003. For the fiscal year ended December 2003 the Celgene Corporation achieved revenues totaling $271.5 million, an increase of 100% on 2002 revenues which totaled $135.7 million • Currently Celgene is a profitable fast growing company. The fuel for Celgene’s fast growth comes from its current products in the market. Company Performance Overview —Income Statement (2000~2004) In Millions 2000 2001 2002 2003 2004 Sales 84.2 114.2 135.7 271.5 377.5 Gross Operating Profit 79.6 105.7 123.9 233.2 332.1 EBIDTA -23.0 -20.0 -30.7 8.2 57.0 Net Income -16.3 -1.9 -100.0 13.6 52.8 Diluted EPS -0.13 -0.02 -0.66 0.08 0.31 Revenue Composition —the Major Revenue Drivers THALOMID 90.00% 80.00% FOCALIN 70.00% 60.00% ALKERAN 50.00% 40.00% other 30.00% 20.00% collaborative ageements and other revenue 10.00% 0.00% 2004 2003 2002 Royalty revenue (from FOCALIN) Revenue Composition —the Major Revenue Drivers % of Total Revenue 2004 2003 2002 THALOMID 81.74% 82.40% 87.71% FOCALIN 1.11% 0.88% 2.84% ALKERAN 4.49% 6.57% -- Other 0.23% 0.21% -- Total net product sales 87.57% 90.05% Collaborative agreements and other Revenue 5.30% Royalty revenue 7.13% 90.55% 5.59% 5.98% 4.36% 3.47% •About 90% of the total revenue came from product sales, almost all of which came from the sales of the three current drugs in the market. •Other sales accounted for <0.25 % THALOMID® No.1 Revenue Driver 2002 2003 2004 $ 119,060 thousand $ 223,686 thousand $ 308,577 thousand 87.71% 82.40% 81.74% • 2002--2003: net sales were higher in 2003, as compared to 2002, due to the combination of price increases and oncologists’ expanded use of the product as a treatment for various types of cancers, especially first-line use in MM. Net sales in 2003 also benefited from the market introduction, during the first half of the year, of two new higher-strength formulations, which had higher per unit sales prices. • 2003-2004: net sales were higher in 2004, as compared to 2003, primarily due to a combination of price increases implemented in the second half of 2003 and in the first nine months of 2004 and increased number of prescriptions. The total number of prescriptions increased approximately 9.4% from the prior year period. THALOMID® No.1 Revenue Driver Significant Event 1. In October 2004 Celgene acquired all of the outstanding shares of Penn T Limited, a worldwide supplier of THALOMID®. • Through manufacturing contracts acquired in this acquisition, the company is now able to have total control over the manufacturing of THALOMID® worldwide. • It also increased Celgene’s participation in the potential sales growth of THALOMID® in key international markets. THALOMID® No.1 Revenue Driver Significant Event 2. In December 2004 it revised the Pharmion product supply agreement acquired in the Penn T acquisition. Under the modified agreement, Pharmion paid Celegene • A one-time payment of $77.0 million in return for a reduction in their total product supply purchase price from 28.0 percent of Pharmion’s thalidomide net sales, including cost of goods to 15.5 percent of net sales. • An additional $8.0 million over the next three years to extend the two companies’ existing thalidomide research and development efforts. • A one-time payment of $3.0 million for granting Pharmion license rights to develop and market thalidomide in three additional Asian territories (Hong Kong, Korea and Taiwan), as well as for eliminating termination rights held by Celgene tied to the regulatory approval of thalidomide in Europe in November 2006. S.T.E.P.S.® - Celgene's Innovative Restricted Distribution Program • In 2004, $0.5M from S.T.E.P.S. use licensing fees. In November 2004, Celgene granted a non-exclusive license to the four companies who manufacture and distribute (sell) isotrentinoin (Accutane(R) for the rights to Celgene's patent portfolio (the S.T.E.P.S. System) directed to methods for safely delivering the product to potentially high-risk patient populations. This will bring more income in the coming years. THALOMID® No.1 Revenue Driver Near Future Outlook Opportunity: (having the total control over the supply of THALOMID) • Lower cost of production through economy of scale and less cost paid to the intermediaries. • Greater potential future income from both the company’s own sales and from sales by others in the international market, and from license fees from the STEPS system. Threat: • Depend too much on this one drug. • Near-Term Competition With THALOMID®: reduce THALOMID® sales. RETALIN® family & FOCALIN series No.2 Revenue Driver In April 2000, Celgene granted Novartis Pharma AG an exclusive license (excluding Canada) for the development and marketing of FOCALIN(R) and long acting drug formulations in return for substantial milestone payments and royalties on FOCALIN(R) and the entire RITALIN(R) family of drugs. In 2002, Novartis launched FOCALIN(R) and RITALIN(R) LA, the long-acting version of RITALIN(R), in the United States, following regulatory approval. RETALIN® family & FOCALIN series No.2 Revenue Driver Product Sales Royalty Revenue 2002 2003 2004 $ 3861 thousand $ 2383 thousand $ 4177 thousand 2.84% 0.88% 1.11% $ 4710 thousand $ 11848 thousand $ 26919 thousand 3.47% 4.36% 7.13% • 2002—2003: The sales dropped by 38.3% due to the timing of shipments to Novartis for their commercial distribution. • 2003—2004: FOCALIN® net sales increased by 75.3% in 2004,due to better timing of shipments to Novartis for their commercial distribution. • Revenue from the royalty has increased in both 2003 and 2004. 2002—2003: by 151.5% 2003—2004: by 127.2%. The increases were due to increases in the royalty rate on both RITALIN® and RITALIN® LA as well as increases in RITALIN® LA sales by Novartis. RETALIN® family & FOCALIN series No.2 Revenue Driver Celgene has been able to maximize the full potential of this unique asset. A steady stream of income from: • royalties on sales of the entire Ritalin family of drugs, • a portion of the revenue from product sales of FOCALIN. Retained the exclusive commercial rights to FOCALIN(R) and FOCALIN(R) XR for oncology-related disorders. Eg. chronic fatigue associated with chemotherapy. RETALIN® family & FOCALIN series No.2 Revenue Driver Important news • The company recently completed a double-blinded randomized placebo-controlled clinical trial evaluating FOCALIN's potential in the treatment of cancer fatigue associated with chemotherapy A huge potential market • It is evaluating potential clinical and regulatory development strategies for this indication. ALKERAN No.3 Revenue Driver 2002 2003 2004 -- $ 17827 thousand $ 16956 thousand -- 6.57% 4.49% Because the supply and distribution agreement with GSK was executed in March 2003, therefore sales for this product are reflected only in the 2003 period. • 2003—2004: net sales dropped by 4.9%, due to supply disruptions earlier in the year inconsistent supplies of ALKERAN® IV inconsistent end-market buying patterns. ALKERAN No.3 Revenue Driver A strategically valuable agreement • provides Celgene with an approved oncology product that complements its THALOMID and REVLIMID(the potential revenue driver). Overall, a stable revenue driver... REVLIMID Potential Revenue Driver Near Future Outlook REVLIMID could have a positive effect on the lives of tens of thousands of patients around the world and on the company itself. Definitely a great potential revenue driver. Cost Structure —Major Cost Components as % of total expenses 50.00% 45.00% 40.00% 35.00% 30.00% COG R&D S,G and A 25.00% 20.00% 15.00% 10.00% 5.00% 0.00% 2004 2003 2002 R&D expenditure accounts for most of the total cost, followed by S,G and A and then COG. Cost Structure —Major Cost Components % of Total Expenses COG R&D S,G and A 2004 2003 2002 17.8% 19.3% 8.3% 48.0% 44.8% 33.9% 34.1% 35.9% 26.4% Major Cost Component R&D R&D spending has been increasing in each of the past years. Major Cost Component R&D 2002 2003 2004 R&D $ 84.9 M $ 122.7 M $ 160.9 M % of Total Revenue 62.6% 45.2% 42.6% Increase from Prior Year + 17.3 M (25.5%) + 37.8 M (44.5%) + 38.2 M (31.1%) • 2002~2003: the increase was primarily due to the initiation of several large studies related to THALOMID® and REVLIMID® clinical programs in the second half of 2002. • 2003~2004: the increase was primarily due to increased spending in various late-stage regulatory programs. These included Phase II regulatory programs for REVLIMID® in MDS and MM, as well as ongoing REVLIMID® Phase III SPA trials in MM. Major Cost Component R&D Break Down 2002 2003 2004 Major Human Phamaceutical clinical Programs $ 27.4 M $ 52.8 M $ 78.3 M Other Human Phamaceutical clinical Programs $ 22.2 M $ 29.2 M $ 33.4 M biopharmaceutical discovery and development programs $ 32.3 M $ 33.7 M $ 40.6 M placental stem cell and biomaterials programs $ 3.0 M $ 7.0 M $ 8.6 M Total $ 84.9 M $ 122.7 M $ 160.9 M Major R&D Cost Drivers To support multiple core programs: • THALOMID®, • REVLIMID®, • ACTIMIDTM, • CC-11006, • PDE4/TNF-alpha inhibitors To investigate other compounds, such as: • kinase inhibitors, • benzopyrans, • ligase inhibitors • tubulin inhibitors, • placental • cord blood derived stem cell programs. Major Cost Component R&D Near Future Outlook At current stage, it’s still quite uncertain about which of these compounds will turn from a cost driver to become a revenue driver. One thing that is certain is that R&D spending will keep accelerating into the near future years. Major Cost Component COG 2002 2003 2004 COG $ 20.87 M $ 52.95 M $ 59.72 M % of Net Product Sales 18.1% 21.7% 17.0% Increase from Prior Year + 1.9 M (9.9%) + 32.1 M (153.7%) + 6.8 M (12.8%) 2002~2003: •Big increase, primarily due to significant growth in THALOMID® sales volumes, higher royalties on THALOMID® product sales. •COG also increased as a % of net product sales. 2003~2004: •Smaller increase primarily as a result of higher royalties on THALOMID®, partially offset by lower ALKERAN® sales. Major Cost Component COG • Overall, the COG occupies less than 22% of the net product sales. • It is possible to further lower its cost of production for THALOMID through the economy of scale (since it controls the worldwide supply now) • The introduction of the REVLIMID will certainly increase the COG, but also the revenue. Major Cost Component S,G and A 2002 2003 2004 S, G and A $ 66.17 M $ 98.47 M $ 114.20 M % of Total Revenue 48.7% 36.3% 30.3% Increase from Prior Year + 13.6 M (25.9%) + 32.3 M (48.8%) + 15.7 M (16.0%) 2002~2003: The significant increase in employees largely explains the jump in S,G and A expenses. Major Cost Component S,G and A 2002~2003 continuous: S, G and A expenses increased primarily due to • first-time expenses of approximately $10.1 million related to the Stem Cell Therapies segment following the December 2002 acquisition of Anthrogenesis Corp. • an increase of approximately $12.0 million in commercial expenses related to the expansion of the sales and marketing organization and an increase in customer service staff • an increase of approximately $10.0 million in general administrative and medical affairs expenses. Major Cost Component S,G and A 2003~2004: S, G and A expenses increased by $15.7 million, as a result of an increase of • approximately $12.0 million in general administrative and medical affairs expenses primarily due to higher headcount-related expenses; and • an increase of approximately $3.6 million in sales force expenses primarily due to the creation of a sales operations group. Major Cost Component S,G and A • On a decreasing trend as a % of total revenue A Good Sign… Company Performance Overview —Balance Sheet (2000~2004) In Millions 2000 2001 2002 2003 2004 Cash and Equivalents 161.4 47.1 85.5 267.5 135.2 Cash Per Share 1.09 0.31 0.53 1.65 0.82 Intangibles 0.0 0.0 6.0 6.2 150.2 Total Assets 346.7 354.0 327.3 791.3 1107.3 Long Term Debt 12.3 11.0 0.0 400.0 400.0 Total Liabilities 51.2 43.6 50.6 481.3 629.8 # of Outstanding Shares 148.0 151.2 160.4 162.8 165.1 Total Equity 295.5 310.4 276.7 310.1 477.4 D/E 0.17 0.14 0.18 1.55 1.32 Consists of only common shares Arrange 400M convertible notes (due in five years) in 2003. The notes can be converted to 16,511,840 shares anytime. In substance, these are equities. 500.0 400.0 Company Performance Overview —Cash Flow Statement (2000~2004) Increase due to the issuance of the convertible notes Growth due to significant increase in products sales 300.0 200.0 Operating Investing Financing Free CF 100.0 0.0 2,000 -100.0 -200.0 -300.0 2,001 2,002 2,003 2,004 2005 RESULTS Company Performance Overview 2005 (Up to September 30) Nine-Month Period Ended September 30 2005 2004 % Change THALOMID $ 281,972 $ 222,498 26.7 % Focalin 3,129 3,698 (15.4%) ALKERAN 30,803 12,025 156.2% Other 1,024 712 43.8% Total net product sales 316,928 238,933 32.6% Collaborative agreements and other revenue 35,829 15,420 132.4% Royalty revenue 34,846 17,741 96.4% Total revenue $ 387,603 $ 272,094 42.5% R&D 138,413 116,520 18.8% COG 53,999 43,655 23.7% S, G and A 126,114 79,408 58.8% Net Income 59,728 30,517 95.7% Net product sales: Company Performance Overview 2005 --Key Ratios Company Amex Biotech S&P 500 Current P/E Ratio 116.0 20.2 18.1 Price/Sales Ratio 21.36 3.39 1.44 Price/Book Value 17.72 4.42 2.79 Price/Cash Flow Ratio 92.50 15.00 11.80 Return On Equity 16.2 21.9 15.8 Return On Assets 7.9 10.9 2.8 Return On Capital 9.5 17.8 7.6 • These ratios are based on latest 12 months' results The Biotech Stock Picking System – Successful Product(s) – Solvency – Quantity of Pipeline – Quality of Pipeline – Management – Collaborations – R&D Recommendation 1. Very high risk 2. High growth potential BUY