Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Commodity market wikipedia , lookup

Futures contract wikipedia , lookup

Black–Scholes model wikipedia , lookup

Futures exchange wikipedia , lookup

Employee stock option wikipedia , lookup

Greeks (finance) wikipedia , lookup

Option (finance) wikipedia , lookup

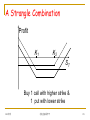

Financial Derivative Reference: 1. John Hull著,张陶伟译,《期权、期货 及其它衍生产品》,第三版,华夏出版社。 2. John Hull著,张陶伟译,《期权期货入 门》 2005年秋 北航金融系李平 1 Chapter 1 Introduction 2005年秋 北航金融系李平 2 Outline 2005年秋 1. Derivatives 2. Forward Contracts 3. Futures Contracts 4. Options 5. Types of Traders 6. Other Derivatives 北航金融系李平 3 1. Derivatives The Nature of Derivatives A derivative is an instrument whose value depends on the values of other more basic underlying variables. 2005年秋 北航金融系李平 4 Examples of Derivatives Forward Contracts Futures Contracts Swaps Options 2005年秋 北航金融系李平 5 Derivatives Markets Exchange-traded markets 2005年秋 CBOT (Chicago Board of Trade), 1848, grain CME (Chicago Mercantile Exchange), 1919, futures CBOE (Chicago Board Options Exchange), 1973, options Traditionally exchanges have used the openoutcry system, but increasingly they are switching to electronic trading Contracts are standard there is virtually no credit risk 北航金融系李平 6 Over-the-counter (OTC) 2005年秋 A computer- and telephone-linked network of dealers at financial institutions, corporations, and fund managers Contracts can be non-standard and there is some small amount of credit risk 北航金融系李平 7 Ways Derivatives are Used 2005年秋 To hedge risks To speculate (take a view on the future direction of the market) To lock in an arbitrage profit To change the nature of a liability To change the nature of an investment without incurring the costs of selling one portfolio and buying another 北航金融系李平 8 2. Forward Contracts A forward contract is an agreement to buy or sell an asset at a certain future time for a certain price (the delivery price) It can be contrasted with a spot contract which is an agreement to buy or sell immediately It is traded in the OTC market Forward contracts on foreign exchange are very popular 2005年秋 北航金融系李平 9 Foreign Exchange Quotes for GBP on Aug 16, 2001 Spot Bid 1.4452 Offer 1.4456 1-month forward 1.4435 1.4440 3-month forward 1.4402 1.4407 6-month forward 1.4353 1.4359 12-month forward 1.4262 1.4268 2005年秋 北航金融系李平 10 Terminology 2005年秋 The party that has agreed to buy has what is termed a long position The party that has agreed to sell has what is termed a short position 北航金融系李平 11 Example On August 16, 2001 the treasurer of a corporation enters into a long forward contract to buy £1 million in six months at an exchange rate of 1.4359 This obligates the corporation to pay $1,435,900 for £1 million on February 16, 2002 What are the possible outcomes? 2005年秋 北航金融系李平 12 Profit from a Long Forward Position Profit K 2005年秋 Price of Underlying at Maturity, ST 北航金融系李平 13 Profit from a Short Forward Position Profit K 2005年秋 Price of Underlying at Maturity, ST 北航金融系李平 14 Forward Price The forward price for a contract is the price agreed today for the delivery of the asset at the maturity date. When move through time the delivery price for the forward contract does not change, but the forward price is likely to do so. 2005年秋 北航金融系李平 15 1) Gold: An Arbitrage Opportunity? Suppose that: The spot price of gold is US$300 The 1-year forward price of gold is US$340 The 1-year US$ interest rate is 5% per annum Is there an arbitrage opportunity? (We ignore storage costs and gold lease rate)? 2005年秋 北航金融系李平 16 2) Gold: Another Arbitrage Opportunity? Suppose that: - The spot price of gold is US$300 - The 1-year forward price of gold is - US$300 The 1-year US$ interest rate is 5% per annum Is there an arbitrage opportunity? 2005年秋 北航金融系李平 17 The Forward Price of Gold If the spot price of gold is S and the forward price for a contract deliverable in T years is F, then F = S (1+r )T where r is the 1-year (domestic currency) risk-free rate of interest. In our examples, S = 300, T = 1, and r =0.05 so that F = 300(1+0.05) = 315 2005年秋 北航金融系李平 18 3. Futures Contracts Agreement to buy or sell an asset for a certain price at a certain time Similar to forward contract Whereas a forward contract is traded OTC, a futures contract is traded on an exchange 2005年秋 北航金融系李平 19 Examples of Futures Contracts 2005年秋 Agreement to: buy 100 oz. of gold @ US$300/oz. in December (COMEX) sell £62,500 @ 1.5000 US$/£ in March (CME) sell 1,000 brl. of oil @ US$50/brl. in April (NYMEX) 北航金融系李平 20 4. Options 2005年秋 A call option is an option to buy a certain asset by a certain date for a certain price (the strike price) A put is an option to sell a certain asset by a certain date for a certain price (the strike price) 北航金融系李平 21 Terminology Strike price (Exercise price) Expiration date (maturity) American/European option 2005年秋 北航金融系李平 22 Exchanges Trading Options Chicago Board Options Exchange American Stock Exchange Philadelphia Stock Exchange Pacific Stock Exchange European Options Exchange Australian Options Market and many more (see list at end of book) 2005年秋 北航金融系李平 23 Long Call on Microsoft Profit from buying a European call option on Microsoft: option price = $5, strike price = $60 30 Profit ($) 20 10 30 0 -5 2005年秋 40 50 Terminal stock price ($) 60 70 北航金融系李平 80 90 24 Short Call on Microsoft Profit from writing a European call option on Microsoft: option price = $5, strike price = $60 Profit ($) 5 0 70 30 40 50 60 -10 80 90 Terminal stock price ($) -20 -30 2005年秋 北航金融系李平 25 Long Put on IBM Profit from buying a European put option on IBM: option price = $7, strike price = $90 30 Profit ($) 20 10 0 -7 2005年秋 Terminal stock price ($) 60 70 80 90 100 110 120 北航金融系李平 26 Short Put on IBM Profit from writing a European put option on IBM: option price = $7, strike price = $90 Profit ($) 7 0 60 70 Terminal stock price ($) 80 90 100 110 120 -10 -20 -30 2005年秋 北航金融系李平 27 Payoffs from Options K = Strike price, ST = Price of asset at maturity Payoff from a long position in the European call: Max(ST-K,0) Payoff from a short position in the European call: -Max(ST-K,0) Payoff from a long position in the European putl: Max(K-ST,0) Payoff from a long position in the European call: -Max(K-ST,0) 2005年秋 北航金融系李平 28 Payoffs from Options Payoff Payoff K K ST Payoff ST Payoff K K 2005年秋 ST ST 北航金融系李平 29 5. Types of Derivative Traders • Hedgers: use derivatives to reduce the risk that they face from potential future movements in a market variable • Speculators: use derivatives to bet on the future direction of a market variable • Arbitrageurs: lock in a riskless profit by simultaneously entering into two or more transactions 2005年秋 北航金融系李平 30 Hedging Examples (1) A US company will pay £10 million for imports from Britain in 3 months and decides to hedge using a long position in a forward contract The price is locked, but the outcome may be worse 2005年秋 北航金融系李平 31 Hedging Examples (2) An investor owns 1,000 Microsoft shares currently worth $73 per share. A two-month put with a strike price of $65 costs $2.50. The investor decides to hedge by buying 10 contracts The difference between the use of forward and options for hedging: 2005年秋 Forward: fix the price Option: provide insurance 北航金融系李平 32 Speculation Example An investor with $4,000 to invest feels that Cisco’s stock price will increase over the next 2 months. The current stock price is $20 and the price of a 2month call option with a strike of 25 is $1 Two possible alternative strategies: buy calls and shares. The use of futures and options for speculation: 2005年秋 Both obtain leverage The potential loss and gain are different 北航金融系李平 33 Arbitrage Example A stock price is quoted as £100 in London and $172 in New York The current exchange rate is 1.7500 What is the arbitrage opportunity? Arbitrage opportunities can’t last for long. 2005年秋 北航金融系李平 34 6. Other Derivatives Plain vanilla/ standard derivatives Exotics Credit derivatives: creditworthiness of a company Weather derivatives: average temperature Insurance derivatives: dollar value of insurance claim Electricity derivatives: spot price of electricity 2005年秋 北航金融系李平 35 Chapter 2 Mechanics of Futures Markets 2005年秋 北航金融系李平 36 Futures Contracts CBOT, CME Available on a wide range of underlying assets Exchange traded Specifications need to be defined: What can be delivered, Where it can be delivered, When it can be delivered Settled daily 2005年秋 北航金融系李平 37 Delivery Closing out a futures position involves entering into an offsetting trade Most contracts are closed out before maturity If a contract is not closed out before maturity, it usually settled by delivering the assets underlying the contract. When there are alternatives about what is delivered, where it is delivered, and when it is delivered, the party with the short position chooses. A few contracts (for example, those on stock indices and Eurodollars) are settled in cash 2005年秋 北航金融系李平 38 Price and Position Limits Many futures exchanges set limits on daily price changes and holdings. Limits are set to prevent excessive volatility and market manipulation. Limits are often removed in the last month of the contract. 2005年秋 北航金融系李平 39 Convergence of Futures to Spot Futures Price Spot Price Futures Price Spot Price Time (a) 2005年秋 Time (b) 北航金融系李平 40 Margin Requirement Initial Margin - funds deposited to provide capital to absorb losses, generally 5%-15%. Maintenance Margin - an established value below which a trader’s margin may not fall. Marking to market When the maintenance margin is reached, the trader will receive a margin call from her broker to add variation margin to reach the level of initial margin. 2005年秋 北航金融系李平 41 Margin Requirement (cont.) 清算所(clearing house): track all the transactions to calculate the positions 经纪人也需在清算所存入保证金(clearing margin) 。但数额小于等于客户交给经纪人的保证 金 变动保证金必须以现金支付,初识保证金中的一 部分可以以生息债券存入。 1990年7月某经纪公司对国际货币市场合约初始保 证金和维持保证金的要求如下表。 2005年秋 北航金融系李平 42 Margin Requirement (cont.) 合约 初始保证金 英镑 $2 800 $2 100 马克 $1 800 $1 400 瑞士法郎 $2 700 $2 000 日元 $2 700 $2 000 加拿大元 $1 000 $800 澳大利亚元 $2 000 $1 500 2005年秋 维持保证金 北航金融系李平 43 Margin Calculation An investor takes a long position in 2 December gold futures contracts on June 4 2005年秋 contract size is 100 oz. futures price is US$400 initial margin requirement is US$2,000/contract (US$4,000 in total, 5%) maintenance margin is US$1,500/contract (US$3,000 in total) 北航金融系李平 44 Margin Calculation (cont.) Day Futures Price (US$) Daily Gain (Loss) (US$) Cumulative Gain (Loss) (US$) 400.00 2005年秋 Margin Account Margin Balance Call (US$) (US$) 4,000 5-Jun 397.00 . . . . . . (600) . . . (600) . . . 13-Jun 393.30 . . . . . . (420) . . . (1,340) . . . 2,660 + 1,340 = 4,000 . . . . . < 3,000 19-Jun 387.00 . . . . . . (1,140) . . . (2,600) . . . 2,740 + 1,260 = 4,000 . . . . . . 26-Jun 392.30 260 (1,540) 5,060 北航金融系李平 3,400 . . . 0 . . . 0 45 Example An investor enters into two long futures contracts on frozen orange juice. Each contract is for the delivery of 15,000 pounds. The current futures price is 160 cents per pound, the initial margin is $6,000 per contract, and the maintenance margin is $4,500 per contract. What price change would lead to a margin call? Under what circumstances could $2,000 be withdrawn from the margin account? Falls by 10 cents and rises by 6.67 cents 2005年秋 北航金融系李平 46 Newspaper quotes Open interest: the total number of contracts outstanding equal to number of long positions or number of short positions One trading older Settlement price: the price just before the final bell each day used for the daily settlement process Volume of trading: the number of trades in 1 day 2005年秋 北航金融系李平 47 Patterns of Futures Prices Normal market: price increase as the time to maturity increase, wheat in CBT Inverted market: Sugar-World Mixed pattern: crude oil Normal backwardation (现货溢价): futures price below the expected spot price Contango (期货溢价) 2005年秋 北航金融系李平 48 Orders 买卖期货合约的两种主要指令 限价指令(limit orders):以预先讲明的价格买卖, 如,以US$0.5323/DM或更低的价格买入两份马克 期货合约 市价指令(market orders):以交易所可得的最优价 格买卖,如,在市场上买入两份期货合约,价格 为交易所可得的最低价格 2005年秋 北航金融系李平 49 Forward Contracts vs Futures Contracts FORWARDS FUTURES Private contract between 2 parties Exchange traded Non-standard contract Standard contract Usually 1 specified delivery date Settled at maturity Settled daily No daily price change limit 交割率为90% 2005年秋 Range of delivery dates Have daily price change limit 交割率不到5% 北航金融系李平 50 Foreign Exchange Quotes Futures exchange rates are quoted as the number of USD per unit of the foreign currency Forward exchange rates are quoted in the same way as spot exchange rates. This means that GBP, EUR, AUD, and NZD are USD per unit of foreign currency. Other currencies (e.g., CAD and JPY) are quoted as units of the foreign currency per USD. 2005年秋 北航金融系李平 51 Chapter 3 Determination of Forward and Futures Prices 2005年秋 北航金融系李平 52 Consumption Assets vs Investment Investment assets are assets held by significant numbers of people purely for investment purposes (Examples: gold, silver) Consumption assets are assets held primarily for consumption (Examples: copper, oil) 2005年秋 北航金融系李平 53 Conversion Formulas Define Rc : continuously compounded rate Rm: same rate with compounding m times per year Rm Rc m ln 1 m Rm m e Rc / m 1 2005年秋 北航金融系李平 54 Example 1. Consider an interest rate that is quoted as 10% per annum with semiannual compounding. What is the equivalent rate with continuous compounding? 2 ln(1 0.1 / 2) 0.09758 2005年秋 北航金融系李平 55 Example (cont.) 2. A deposit account pays 12% per annum with continuous compounding, but interest is actually paid quarterly. How much interest will be paid each quarter on a $10,000 deposit? 100000.1218/4=304.55 2005年秋 北航金融系李平 56 Forward vs Futures Prices Forward and futures prices are usually assumed to be the same. When interest rates are uncertain they are, in theory, slightly different. 2005年秋 北航金融系李平 57 Notation S0 : Spot price today F0 : Futures or forward price today T: Time until delivery date r: Risk-free interest rate for maturity T 2005年秋 北航金融系李平 58 An Arbitrage Opportunity? Suppose that: The spot price of gold is US$300 The 1-year futures price of gold is US$340 The 1-year US$ interest rate is 5% per annum Is there an arbitrage opportunity? (We ignore storage costs and gold lease rate) 2005年秋 北航金融系李平 59 Another Arbitrage Opportunity? Suppose that: 2005年秋 The spot price of gold is US$300 The 1-year futures price of gold is US$300 The 1-year US$ interest rate is 5% per annum Is there an arbitrage opportunity? What if the 1-year futures price of gold is US$315? 北航金融系李平 60 The Futures Price of Gold If the spot price of gold is S0 and the futures price for a contract deliverable in T years is F0, then F0 = S0 (1+r )T where r is the 1-year (domestic currency) risk-free rate of interest. In our examples, S0 = 300, T = 1, and r =0.05 so that F0 = 300(1+0.05) = 315 2005年秋 北航金融系李平 61 For investment asset For any investment asset that provides no income and has no storage costs F0 = S0(1 + r )T If r is compounded continuously F0 = S0erT 2005年秋 北航金融系李平 62 For Investment Asset Providing Known Cash Income stocks paying known dividends, coupon bond 2005年秋 北航金融系李平 63 Example: An Arbitrage Opportunity? Consider a long forward contract to purchase a coupon-bearing bond whose current price is $900 The forward contract matures in one year and the bond matures in 5 years, so the forward contract is to purchase a 4-year bond in one year Coupon payments of $40 are expected after 6 months and 12 months The 6-month and 1-year risk-free interest rates (continuous compounding) are 9% per annum and 10% per annum, respectively 2005年秋 北航金融系李平 64 An Arbitrage Opportunity? (cont.) If the forward price $930 An arbitrageur can borrow $900 to buy the bond and short a forward contract Since 40e-0.090.5=$38.24, so, of the $900, $38.24 is borrowed at 9% per annum for six months The remaining $861.76 is borrowed at 10% per annum for one year 2005年秋 北航金融系李平 65 An Arbitrage Opportunity? (cont.) The amount owing at the end of the year is $861.76e0.11=$952.39 The second coupon provides $40, and $930 is received from the bond selling under the forward contract The net profit is $40+ $930 - $952.39=$17.61 2005年秋 北航金融系李平 66 An Arbitrage Opportunity? (cont.) If the forward price $905 An investor who holds the bond can sell it and enter a forward contract of the $900 realized from selling the bond, $38.24 is invested at 9% per annum for 6 months so that it grows to $40 The remaining $861.76 is invested at 10% per annum for one year and grows to $952.39 2005年秋 北航金融系李平 67 An Arbitrage Opportunity? (cont.) The net gain is $952.39 -$40- $905 =$7.39 When will no arbitrage exist? $912.39 2005年秋 北航金融系李平 68 Generalization When an Investment Asset Provides a Known Dollar Income F0 = (S0 – I )erT where I is the present value of the income In our example 2005年秋 北航金融系李平 69 For investment asset (cont.) When an Investment Asset Provides a Known Yield F0 = S0 e(r–q )T where q is the average yield during the life of the contract (expressed with continuous compounding) 2005年秋 北航金融系李平 70 Example 1. Consider a 10-month forward contract on a stock with a price of $50. The risk-free interest rate (continuous compounded) is 8% per annum for all maturities. Assume that dividends of $0.75 per share are expected after three months, six months and nine months. What is the forward price? 51.14 2005年秋 北航金融系李平 71 Example (cont.) 2. Consider a six-month futures contract on an asset that is expected to provide income equal to 2% of the asset price once during the six-month period. The risk-free rate of interest (continuous compounded) is 10% per annum. The asset price is $25. What is the futures price? 25e(0.1-0.0396)/2=25.77 2005年秋 北航金融系李平 72 For Stock Index Futures Can be viewed as an investment asset paying a dividend yield The investment asset is the portfolio of stocks underlying the index The dividend paid are the dividends that would be received by the holder of the portfolio It is usually assumed that the dividends provide a known yield rather than a known cash income 2005年秋 北航金融系李平 73 For Stock Index Futures (cont.) The futures price and spot price relationship is therefore F0 = S0 e(r–q )T where q is the dividend yield on the portfolio represented by the index 2005年秋 北航金融系李平 74 For Stock Index Futures (cont.) 2005年秋 In practice, the dividend yield on the portfolio underlying the index varies week by week throughout the year. The chosen value of q should represent the average annualized dividend yield during the life of the contract. 北航金融系李平 75 Example The risk-free interest rate is 9% per annum with continuously compounding The dividend on the stock index varies throughout the year. In February, May, August and November, dividends are paid at a rate of 5% per annum. In other months, dividends are paid at a rate of 2% per annum. The value of the index on July 31, 2002 is 300. What is the futures price for a contract deliverable on December 31, 2002? 307.34 2005年秋 北航金融系李平 76 Index arbitrage If F0 > S0 e(r–q )T , profits can be made by buying the stocks underlying the index and shorting futures contract; If F0 < S0 e(r–q )T , profits can be made by shorting or selling the stocks underlying the index and taking a long position in futures contract. 2005年秋 北航金融系李平 77 Forward and Futures on Currencies A foreign currency is analogous to a security providing a dividend yield The continuous dividend yield is the foreign risk-free interest rate It follows that if rf is the foreign riskfree interest rate F0 S0e 2005年秋 ( r rf ) T 北航金融系李平 78 Example Suppose that the two-year interest rate in Australia and the United States are 5% and 7%, respectively, The spot exchange rate between the Australian dollar and the US dollar is US$0.62/AUD. What is two-year forward exchange rate? 0.6453 2005年秋 北航金融系李平 79 Another example You observe that British pound March 93 futures contract settled at $1.5372/pound and the June 93 futures contract settled at $1.5276/pound. What is the implied interest rate difference for this period between pound and dollar? FJun93 1 ln r r f 0.0249 T2 T1 FMar93 2005年秋 北航金融系李平 80 Futures on Commodities Storage cost for investment asset is regarded as negative income, so F0 = (S0+U )erT where U is the present value of the storage costs. Alternatively, F0 = S0 e(r+u )T where u is the storage cost per annum as a percent of the spot price. 2005年秋 北航金融系李平 81 Example Consider a one-year futures contract on gold. Suppose that it costs $2 per once per year to store gold, with the payment being made at the end of the year. Assume that the spot price is $450, and the risk-free rate is 7% per annum with continuous compounding. Then the futures price is 484.63 2005年秋 北航金融系李平 82 Consumption Assets One keep the commodity for consumption, so he won’t sell the commodity and buy futures, which influence the arbitrage argument. F0 S0 e(r+u )T or F0 (S0+U )erT 2005年秋 北航金融系李平 83 The convenience yield The convenience yield on the consumption asset ability to profit from temporary local shortages ability to immediately keep a production process running The convenience yield, y, is defined so that F0 eyT= S0 e(r+u )T Or 2005年秋 F0 = S0 e(r+u-y )T 北航金融系李平 84 Cost of Carry Cost of carry refers to the cost and benefit of holding the asset, including: interest rate paid to finance the asset storage costs dividends or other income 2005年秋 北航金融系李平 85 Cost-of-Carry (cont.) Non-divident-paying stock (no storage cost and no income): c =r Stock index: c =r-q Currency: c =r-rf Commodities: c =r+u 2005年秋 北航金融系李平 86 Cost-of-Carry and futures price For an investment asset F0 = S0ecT For a consumption asset F0 = S0e(c-y)T 2005年秋 北航金融系李平 87 Futures Prices & Expected Future Spot Prices Suppose k is the expected return required by investors on an asset We can invest F0e–r T now to get ST back at maturity of the futures contract This shows that F0 = E (ST )e(r–k )T 88 Valuing a Forward Contract Suppose that K is delivery price in a forward contract F0 is forward price that would apply to the contract today The value of a long forward contract, ƒ, is ƒ = (F0 – K )e–rT Similarly, the value of a short forward contract is (K – F0 )e–rT 2005年秋 北航金融系李平 89 Example A long forward contract on a non-dividend paying stock was entered into some time ago. It currently has six months to maturity. The risk-free interest rate (with continuous compounding) is 10% per annu, the stock price is $25 and delivery price is $24. What is the value of the forward contract? $2.17 2005年秋 北航金融系李平 90 Chapter 4 Hedging Strategies Using Futures 2005年秋 北航金融系李平 91 Long & Short Hedges long futures hedge: involves a long position in futures, appropriate when you know you will purchase an asset in the future and want to lock in the price short futures hedge: involves a short position in futures, appropriate when you know you will sell an asset in the future & want to lock in the price 2005年秋 北航金融系李平 92 Example of short hedge On May 15, X has contracted to sell 1 million barrels of oil on August 15 at the spot price of that day May 15 quotes: S1= $19.00 /barrel, F1= $18.75 /barrel Hedging actions: Contract size: 1000 barrels On May 15, short 1000 August oil futures On August 15, close out futures position 2005年秋 北航金融系李平 93 Example (cont.) August 15: S2= F2=$17.50 /barrel, X receives $17.50 per barrel per contract Gains from futures=F1-F2 =$(18.75 - 17.50) = $1.25 per barrel Price realized=$17.50+ $1.25 =$18.75= F1+( S2- F2) Alternatively if S2=$19.50 /barrel 2005年秋 北航金融系李平 94 Basis Risk Basis is the difference between spot & futures prices Basis risk arises because of the uncertainty about the basis when the hedge is closed out 2005年秋 The asset to be hedged may not be the same as the asset underlying the futures The hedger is uncertain about the precise date of buying or selling the asset 北航金融系李平 95 Choice of Contract Choose a delivery month that is as close as possible to, but later than, the end of the life of the hedge When there is no futures contract on the asset being hedged, choose the contract whose futures price is most highly correlated with the asset price. 2005年秋 北航金融系李平 96 Long Hedge Suppose that F1 : Initial Futures Price F2 : Final Futures Price S2 : Final Asset Price b2 : Basis at time t2 You hedge the future purchase of an asset by entering into a long futures contract Cost of Asset=S2 –(F2 – F1) = F1 + Basis 2005年秋 北航金融系李平 97 Example 2 It is June 8 and a company knows that it will need to purchase 20,000 barrels of crude oil at some time in October or November. Oil futures contracts are currently traded for delivery every month on NYMEX and the contract size is 1,000 barrels. The company therefore decides to take a long position in 20 December contracts for hedging (Assuming that the hedge ratio is 1). 2005年秋 北航金融系李平 98 Example 2 (cont.) The futures price on June 8 is F1=$18 /barrel. The company finds that it is ready to purchase the crude oil on November 10. It therefore closes out its futures contract on that date. The pot price and futures price on November 10 are S2=$20 and F2=$ 19.10 per barrel. The gain on the futures contract is 19.1018=$1.10 per barrel. The effective price paid is 20-1.10=$18.90 2005年秋 北航金融系李平 99 Short Hedge Suppose that F1 : Initial Futures Price F2 : Final Futures Price S2 : Final Asset Price You hedge the future sale of an asset by entering into a short futures contract Payoff Realized=S2+ (F1 –F2) = F1 + Basis 2005年秋 北航金融系李平 100 Basis risk Since F1 is known at t1, hedging risk is the basis risk b2 when asset to be hedged is different from asset underlying futures Effective price at t2 is (S2 + F1 - F2) = F1 +(S2* - F2) + (S2 - S2*) where S2* is the spot price of the asset underlying the futures contract The term (S2 - S2*) arises due to the difference between the two assets 2005年秋 北航金融系李平 101 Optimal Hedge Ratio Hedge ratio: the ratio of the position taken in futures contract to the size of the exposure Optimal hedge ratio: proportion of the exposure that should optimally be hedged is (extra1) sS h r sF * where sS and sF are the standard deviations of dS and dF, the change in the spot price and futures price during the hedging period, r is the coefficient of correlation between dS and dF. 2005年秋 北航金融系李平 102 Example 2 (cont.) If the company decides to use a hedge ratio of 0.8, how does the decision affect the way in which the hedge is implemented and the result? If the hedge ratio is 0.8, the company takes a long position in 16 NYM December oil futures contracts on June 8 and closes out its position on November 10. 2005年秋 北航金融系李平 103 Example 2 (cont.) The gain on the futures position is (19.10-18)16,000=17,600 The effective cost of the oil is therefore 20,00020-17,600=382,400 or $19.12 per barrel. (This compares with $18.90 per barrel when the hedge ratio is 1.) 2005年秋 北航金融系李平 104 Hedging Using Index Futures To hedge the risk in a portfolio the number of index futures contracts that should be used is P A where P is the value of the portfolio, is its beta, and A is the value of the index underlying one futures contract 105 Example 3 Value of S&P 500 is 1,000 Value of Portfolio is $5 million Beta of portfolio is 1.5 What position in futures contracts on the S&P 500 is necessary to hedge the portfolio? (Example3) 2005年秋 北航金融系李平 106 Chapter 6 Swaps 2005年秋 北航金融系李平 107 Outline A swap is an agreement to exchange cash flows at specified future times according to certain specified rules Contents: Two plain vanilla swap: 2005年秋 How swaps are defined How they are be used How they can be valued Interest-rate swap, fixed-for-fixed currency swap 北航金融系李平 108 1. An Example of a “Plain Vanilla” Interest Rate Swap 2005年秋 An agreement by Microsoft to receive 6-month LIBOR & pay a fixed rate of 5% per annum every 6 months for 3 years on a notional principal of $100 million Next slide illustrates cash flows 北航金融系李平 109 Cash Flows to Microsoft ---------Millions of Dollars--------LIBOR FLOATING 2005年秋 FIXED Net Date Rate Cash Flow Cash Flow Cash Flow Mar.5, 2001 4.2% Sept. 5, 2001 4.8% +2.10 –2.50 –0.40 Mar.5, 2002 5.3% +2.40 –2.50 –0.10 Sept. 5, 2002 5.5% +2.65 –2.50 +0.15 Mar.5, 2003 5.6% +2.75 –2.50 +0.25 Sept. 5, 2003 5.9% +2.80 –2.50 +0.30 Mar.5, 2004 6.4% +2.95 –2.50 +0.45 北航金融系李平 110 Typical Uses of an Interest Rate Swap Converting a liability from fixed rate to floating rate floating rate to fixed rate 2005年秋 Converting an investment from fixed rate to floating rate floating rate to fixed rate 北航金融系李平 111 Intel and Microsoft (MS) Transform a Liability 5% 5.2% Intel MS LIBOR+0.1% LIBOR 2005年秋 北航金融系李平 112 Financial Institution is Involved 4.985% 5.015% 5.2% Intel F.I. MS LIBOR+0.1% LIBOR 2005年秋 LIBOR 北航金融系李平 113 Intel and Microsoft (MS) Transform an Asset 5% 4.7% Intel MS LIBOR-0.25% LIBOR 2005年秋 北航金融系李平 114 Financial Institution is Involved 4.985% 5.015% 4.7% F.I. Intel MS LIBOR-0.25% LIBOR 2005年秋 LIBOR 北航金融系李平 115 The Comparative Advantage Argument AAACorp wants to borrow floating BBBCorp wants to borrow fixed Fixed 2005年秋 Floating AAACorp 10.00% 6-month LIBOR + 0.30% BBBCorp 11.20% 6-month LIBOR + 1.00% 北航金融系李平 116 The Swap 9.95% 10% AAA BBB LIBOR+1% LIBOR 2005年秋 北航金融系李平 117 The Swap when a Financial Institution is Involved 9.93% 9.97% 10% F.I. AAA BBB LIBOR+1% LIBOR 2005年秋 LIBOR 北航金融系李平 118 Reason for the Comparative Advantage The 10.0% and 11.2% rates available to AAACorp and BBBCorp in fixed rate markets are 5-year rates The LIBOR+0.3% and LIBOR+1% rates available in the floating rate market are six-month rates The spread reflects the probability of default 2005年秋 北航金融系李平 119 Swaps & Forwards A swap can be regarded as a convenient way of packaging forward contracts The “plain vanilla” interest rate swap in our example consisted of 6 FRAs The value of the swap is the sum of the values of the forward contracts underlying the swap 2005年秋 北航金融系李平 120 Valuation of an Interest Rate Swap A swap is worth zero to a company initially. This means that it costs nothing to enter into a swap At a future time its value is liable to be either positive or negative 2005年秋 北航金融系李平 121 Valuation of an Interest Rate Swap (cont.) 2005年秋 Interest rate swaps can be valued as the difference between the value of a fixed-rate bond and the value of a floating-rate bond Alternatively, they can be valued as a portfolio of forward rate agreements (FRAs) 北航金融系李平 122 Valuation in Terms of Bonds Vswap=Bfl-Bfix (or, Bfix-Bfl) The fixed rate bond is valued in the usual way The floating rate bond is valued by noting that it is worth par immediately after the next payment date 2005年秋 北航金融系李平 123 Example 1 Suppose that a financial institution pays 6-month LIBOR and receives 8% per annum (with semiannual compounding) on a swap with a notional principle of $100 and the remaining payment dates are in 3, 9 and 15 months. The swap has a remaining life of 15months. The LIBOR rates with continuous compounding for 3-month, 9-month and 15-month maturities are 10%, 10.5% and 11%, respectively. The 6-month LIBOR rate at the last payment date was 10.2% (with semiannual compounding). 2005年秋 北航金融系李平 124 Valuation in Terms of FRAs Each exchange of payments in an interest rate swap is an FRA The FRAs can be valued on the assumption that today’s forward rates are realized 2005年秋 北航金融系李平 125 2. An Example of a fixed-forfixed Currency Swap An agreement to pay 11% on a sterling principal of £10,000,000 & receive 8% on a US$ principal of $15,000,000 every year for 5 years 2005年秋 北航金融系李平 126 Exchange of Principal 2005年秋 In an interest rate swap the principal is not exchanged In a currency swap the principal is exchanged at the beginning and the end of the swap 北航金融系李平 127 The Cash Flows Year 2001 2002 2003 2004 2005 2006 2005年秋 Dollars Pounds $ £ ------millions-----–15.00 +10.00 +1.20 –1.10 +1.20 –1.10 +1.20 –1.10 +1.20 –1.10 +16.20 -11.10 北航金融系李平 128 Typical Uses of a Currency Swap 2005年秋 Conversion from a liability in one currency to a liability in another currency 北航金融系李平 Conversion from an investment in one currency to an investment in another currency 129 Comparative Advantage Arguments for Currency Swaps General Motors wants to borrow AUD Qantas wants to borrow USD USD AUD General Motors 5.0% 12.6% Qantas 13.0% 7.0% 130 Valuation of Currency Swaps 2005年秋 Like interest rate swaps, currency swaps can be valued either as the difference between 2 bonds or as a portfolio of forward contracts Valuation in Terms of Bonds: Vswap=BD-S0 BF (or, S0BF -BD ) 北航金融系李平 131 Example 2 Suppose that the term structure of interest rates is flat in both Japan and United States. The Japanese rate is 4% per annum and the U.S. rate is 9% per annum (both with continuous compounding). A financial institution enters into a currency swap in which it receives 5% per annum in yen and pays 8% per annum in dollars once a year. The principles in the two currencies are $10 million and 1,200 million yen. The swap will last for another three years and the current exchange rate is 110yen=$1. 2005年秋 北航金融系李平 132 Example 3 Company X wishes to borrow U.S. dollars at a fixed rate of interest and company Y wishes to borrow Japanese Yen at a fixed rate of interest. The companies have been quoted the following interest rates. Yen Dollars Company X 5.0% 9.6% Company Y 6.5% 10.0% Design a swap that will net a bank, acting as intermediary, 50bp per annum and make the swap equally attractive to the two companies. 2005年秋 北航金融系李平 133 Example 4 A $100 million interest swap has a remaining life of 10 months. Under the terms of the swap, 6-month LIBOR is exchanged for 12% per annum (semiannual compounding). The average of the bid-offer rate being exchanged for 6-month LIBOR in swaps of all maturities is currently 10% per annum with continuous compounding. The 6-month LIBOR rate was 9.6% per annum two months ago. What is the current value of the swap to the party paying floating? 2005年秋 北航金融系李平 134 Chapter 7 Mechanics of Options Markets 2005年秋 北航金融系李平 135 Types of Options A call is an option to buy A put is an option to sell A European option can be exercised only at the end of its life An American option can be exercised at any time 2005年秋 北航金融系李平 136 Types of options (cont.) Stock options: American in U.S. Index options:traded on CBOE 2005年秋 An option is to buy or sell 100 times the index value Options on S&P500 are European Options on S&P100 are American Settled in cash 北航金融系李平 137 Types of options (cont.) Futures option 2005年秋 期货到期日比期权到期日稍晚 和期货合约在同一交易所交易 When a call is exercised, the holder get a long position in the underlying futures plus a cash amount equal to the excess of the futures price over the strike price 北航金融系李平 138 Types of options (cont.) Foreign currency option 2005年秋 Traded on Philadelphia Stock Exchange 以外币的本币价格表示:如英镑买入期权 的价格为$ 0.035/£ 北航金融系李平 139 Specification of Exchange-Traded Options 2005年秋 Expiration date Strike price European or American Call or Put (option class) 北航金融系李平 140 Terminology Moneyness : At-the-money option In-the-money option Out-of-the-money option 2005年秋 北航金融系李平 141 Terminology (continued) 2005年秋 Option class (call or put) Option series Intrinsic value Time value 北航金融系李平 142 Dividends & Stock Splits 2005年秋 Suppose you own N options with a strike price of K : No adjustments are made to the option terms for cash dividends When there is an n-for-m stock split, the strike price is reduced to mK/n the no. of options is increased to nN/m Stock dividends are handled in a manner similar to stock splits 北航金融系李平 143 Dividends & Stock Splits (continued) 2005年秋 Consider a call option to buy 100 shares for $20/share How should terms be adjusted: for a 2-for-1 stock split? for a 25% stock dividend? 200 share, $10/share 125 share, $16/share 北航金融系李平 144 Position limits and Exercise limits 2005年秋 Position limits: the maximum number of option contracts that an investor can hold on one side of the market (long call and short put are considered to be on the same side of the market) Exercise limits: the maximum number of contracts that can be exercised by any investor in any period of five consecutive trading days 北航金融系李平 145 Newspaper quotes Market Makers 2005年秋 Most exchanges use market makers to facilitate options trading A market maker quotes both bid and ask prices when requested The market maker does not know whether the individual requesting the quotes wants to buy or sell 北航金融系李平 146 Margins Margins are required when options are sold When a naked call (put) option is written the margin is the greater of: 1 2 A total of 100% of the proceeds of the sale plus 20% of the underlying share price less the amount (if any) by which the option is out of the money A total of 100% of the proceeds of the sale plus 10% of the underlying share price (exercise price) When writing covered calls, no margin is required 2005年秋 北航金融系李平 147 Margins (cont.) Example: An investor writes four naked call options on a stock. The option price is $5, the strike price is $40, and the stock price is $38. What is the margin requirement? $4240 2005年秋 北航金融系李平 148 Warrants, Executive Stock Options and convertible bonds Are call options that are written by a company on its own stock When they are exercised, the company issues more of its own stock and sells them to the option holder for the strike price The exercise leads to an increase in the number of the company’s stock outstanding 2005年秋 北航金融系李平 149 Warrants Warrants are call options coming into existence as a result of a bond issue They are added to the bond issue to make the bond more attractive to investors Once they are created, they sometimes trade separately from the bonds 宝钢权证 2005年秋 北航金融系李平 150 Executive Stock Options Call option issued by a company to executives to motivate them to act in the best interests of the company’s shareholders Usually at-the-money when issued Can’t be traded Often last for 10 or 15 years 2005年秋 北航金融系李平 151 Convertible Bonds 2005年秋 Convertible bonds are regular bonds that can be exchanged for equity at certain times in the future according to a predetermined exchange ratio Is a bond with an embedded call option on the company’s stock 北航金融系李平 152 Chapter 8 Properties of Stock Option Prices 2005年秋 北航金融系李平 153 Outline The relationship between the option price and the underlying stock price (by arbitrage argument) Whether an American option should be exercised early 2005年秋 北航金融系李平 154 Notation c : European call option price p : European put option price S0 : Stock price today K : Strike price T : Life of option s: Volatility of stock price 2005年秋 C : American Call option price P : American Put option price ST :Stock price at option maturity D : Present value of dividends during option’s life r : Risk-free rate for maturity T with cont. comp. 北航金融系李平 155 Effect of Variables on Option Pricing Variable S0 K T s r D 2005年秋 c + – ? + + – p – +? + – + 北航金融系李平 C + – + + + – P – + + + – + 156 American vs European Options An American option is worth at least as much as the corresponding European option Cc Pp C max( c, S K ) P max( p, K S ) 2005年秋 北航金融系李平 157 Upper bounds for option prices c S0 , C S0 p Ke 2005年秋 rT , PK 北航金融系李平 158 Lower bound for European calls on non-dividend-paying stocks Portfolio A: one European call & an amount of cash equal to Ke-rT Portfolio B: one share c(t) max(S(t) –Ke 2005年秋 北航金融系李平 –rT, 0) 159 Calls: An Arbitrage opportunity? Suppose that c(t) = 3 S(t) = 20 T=1 r = 10% K = 18 D=0 Is there an arbitrage opportunity? S(t) –Ke –rT=3.71>3=c,buy call, short stock. If the inflow ($17) is invested for one year at 10% per Annum, it will be $18.79. 2005年秋 北航金融系李平 160 Lower bound for European puts on non-dividend-paying stocks Portfolio A: one European put & one share Portfolio B: an amount of cash equal to Ke-rt p(t) max( Ke-rT–S(t),0) 2005年秋 北航金融系李平 161 Puts: An Arbitrage opportunity? Suppose that p(t)= 1 S(t) = 37 T = 0.5 r =5% K = 40 D =0 Is there an arbitrage opportunity? Ke-rT–S(t)=2.01>1=p, 借$38,为期6个月,用 借款购买卖权和股票, 6个月后借款为$38.96。 2005年秋 北航金融系李平 162 Put-call parity for nondividend-paying stocks Portfolio A: One European call on a stock + an amount of cash equal to Ke-rT Portfolio B: One European put on the stock + one share Both are worth MAX(ST , K ) at the maturity of the options They must therefore be worth the same today c(t) + Ke -rT = p(t) + S(t) 2005年秋 北航金融系李平 163 Arbitrage Opportunities 2005年秋 Suppose that c(t)= 3 S(t)= 31 T = 0.25 (3-m) r = 10% K =30 D=0 What are the arbitrage possibilities when p(t) = 2.25 ? p(t) = 1 ? 北航金融系李平 164 When p(t)=2.25 c(t)+Ke-rt=32.26, p(t)+S(t)=33.25 Portfolio B is overpriced. The arbitrage strategy: buy the call, short both the stock and the put. Generating a positive cash flow of 2.25+31-3=30.25 After three months, this amount grows to 31.02 2005年秋 北航金融系李平 165 Continue If S(T)>K, exercise the call If S(T) K, the put is exercised In either case, the investor ends up buying one share for $30 to close the short position. The net profit: 31.02-30 continue 2005年秋 北航金融系李平 166 When p(t)=1 2005年秋 c(t)+Ke-rt=32.26, p(t)+S(t)=32 Portfolio A is overpriced. The arbitrage strategy: short the call, buy both the stock and the put. Initial investment: 1+31-3=$29 北航金融系李平 167 Continue The initial investment is financed at 10%. A repayment of $29.73 is required at the end of three months. Either the call or put is exercised, the stock will be sold for $30. The net profit: 30-29.73 2005年秋 北航金融系李平 168 Early Exercise for American options 2005年秋 Usually there is some chance that an American option will be exercised early An exception is an American call on a non-dividend paying stock This should never be exercised early 北航金融系李平 169 An Extreme Situation For an American call option: S(t) = 50; T = 1m; K = 40; D = 0 Should you exercise immediately? What should you do if 1. 2. 2005年秋 You want to hold the stock for one month? You do not feel that the stock is worth holding for the next 1 month? 北航金融系李平 170 Reasons For Not Exercising a Call Early--No Dividends Case 1: should keep the option and exercise it at the end of the month. 2005年秋 We delay paying the strike price, earn the interest No income is sacrificed (no dividend) Holding the call provides insurance against stock price falling below strike price 北航金融系李平 171 Reasons For Not Exercising a Call Early--No Dividends (cont.) Case 2: Better action: sell the option The option will be bought by another investor who does want to hold the stock. Such investors must exist, otherwise the current stock price would not be $50. The price obtained for the option will be greater than its intrinsic value of $10. 2005年秋 北航金融系李平 172 More formal argument C c S0–Ke –rT>S0–K If it is optimal to exercise early, C=S0–K 2005年秋 北航金融系李平 173 Should Puts Be Exercised Early? 2005年秋 A put option should be exercised early if it is deep in the money. An extreme case: S(t)= 0; K = $10; D = 0 The profit of exercise now: $10, and can also get interest. If wait, the profit will be less than 10. 北航金融系李平 174 The Impact of Dividends on Lower Bounds Portfolio A: one European call & an amount of cash equal to Ke-rT+D Portfolio B: one share c S0 D Ke p D Ke 2005年秋 rT 北航金融系李平 rT S0 175 Impact on Put-Call Parity European options; D > 0 c + D + Ke -rT = p + S0 American options; D = 0 S 0 K C P S 0 Ke rT American options; D > 0 S 0 D K C P S 0 Ke 2005年秋 北航金融系李平 rT 176 Chapter 9 Trading Strategies Involving Options 2005年秋 北航金融系李平 177 Three Alternative Strategies Take a position in the option and the underlying Take a position in 2 or more options of the same type (A spread) Combination: Take a position in a mixture of calls & puts (A combination) 2005年秋 北航金融系李平 178 Positions in an Option & the Underlying Long a stock & short a call = writing a covered call (a) Short a stock & long a call = reverse of a covered call Long a stock & long a put = protective put (b) Short a stock & short a put= reverse of a protective put 2005年秋 北航金融系李平 179 Profit Profit K K ST ST (b) (a) Profit Profit K ST (c) 2005年秋 K ST (d) 北航金融系李平 180 Bull Spread Using Calls Profit S K1 2005年秋 K2 T Buy lower & sell higher call 北航金融系李平 181 Continue Bull spread created from calls requires an initial investment Profit from a bull spread Example: K1=30, c1=3, K2=35, c2=1 Construct a bull and give the profit. 2005年秋 北航金融系李平 182 Bull Spread Using Puts Profit K1 K2 ST Buy lower & sell higher put 2005年秋 北航金融系李平 183 Continue Bull spread created from puts brings a cash inflow to investors A bull spread strategy limits the upside potential as well as the downside risk 2005年秋 北航金融系李平 184 Bear Spread Using Calls Profi t K1 K2 ST Buy higher & sell lower call 2005年秋 北航金融系李平 185 Bear Spread Using Puts Profit K1 K2 ST Buy higher & sell lower put 2005年秋 北航金融系李平 186 Butterfly Spread Using Calls Profit K1 K2 K3 ST Buy 1 high & 1 low, sell 2 middle 2005年秋 北航金融系李平 187 Butterfly Spread Strategy Generally K2 is close to the current stock price When it is appropriate? Payoff Example: K1=55, c1=10, K2=60, c2=7, K2=65, c2=5, S0=61 2005年秋 北航金融系李平 188 Butterfly Spread Using Puts Profit K1 2005年秋 K2 北航金融系李平 K3 ST 189 Calendar Spread Using Calls Profit ST K Buy longer & sell shorter (maturity) 2005年秋 北航金融系李平 190 Calendar Spread Using Puts Profit ST K 2005年秋 北航金融系李平 191 A Straddle Combination Profit K ST Buy a call & a put 2005年秋 北航金融系李平 192 Continue Payoff structure When it is appropriate? Example: 2005年秋 S0=69, expect a significant move in the future, K=70, c=4, p=3 北航金融系李平 193 Strip & Strap Profit Profit K ST K Strap Strip Buy 1 call & 2 puts 2005年秋 ST Buy 2 calls & 1 put 北航金融系李平 194 A Strangle Combination Profit K1 K2 ST Buy 1 call with higher strike & 1 put with lower strike 2005年秋 北航金融系李平 195 Example 1 Suppose that put options with strike prices $30 and $35 cost $4 and $7, respectively. How can these two options can be used to create (a) a bull spread (b) a bear spread? Show the profit for both spreads. 2005年秋 北航金融系李平 196 Example 2 Call options on a stock are available with strike prices of $15, $17.5 and $20 and expiration dates in three months. Their prices are $4, $2 and $0.5 respectively. Explain how these options can be used to create a butterfly spread. What is the pattern of profits from this spread? 2005年秋 北航金融系李平 197 Example 3 A call with a strike price of $50 costs $2. A put with a strike price of $45 costs $3. Explain how a strangle can be created from these two options. What is the pattern of profits from the strangle? 2005年秋 北航金融系李平 198 Example 4 An investor believes that there will be a big jump in a stock price, but is uncertain to the direction. Identify six different strategies the investor can follow and explain the differences between them. 2005年秋 北航金融系李平 199 Chapter 10 Binomial Model 2005年秋 北航金融系李平 200 A Simple Example A stock price is currently $20 In three months it will be either $22 or $18 Stock Price = $22 Stock price = $20 Stock Price = $18 2005年秋 北航金融系李平 201 A Call Option A 3-month call option on the stock has a strike price of 21. Stock Price = $22 Option Price = $1 Stock price = $20 Option Price=? Stock Price = $18 Option Price = $0 2005年秋 北航金融系李平 202 Setting Up a Riskless Portfolio Consider the Portfolio: long shares short 1 call option 22 – 1 20-c 18 Portfolio is riskless when 22 – 1 = 18 or = 0.25 2005年秋 北航金融系李平 203 Valuing the Portfolio (Risk-Free Rate is 12%) The riskless portfolio is: long 0.25 shares short 1 call option The value of the portfolio in 3 months is 22´0.25 – 1 = 4.50 The value of the portfolio today is (noarbitrage argument) 4.5e – 0.12´0.25 = 4.3670 2005年秋 北航金融系李平 204 Valuing the Option 2005年秋 The portfolio that is long 0.25 shares short 1 option is worth 4.367 today. The value of the shares today is 5.000 (= 0.25´20 ) The value of the option is therefore 0.633 (= 5.000 – 4.367 ) 北航金融系李平 205 Generalization A derivative lasts for time T and is dependent on a stock S0u ƒu S0 ƒ 2005年秋 S0d ƒd 北航金融系李平 206 Generalization (continued) Consider the portfolio that is long shares and short 1 derivative S0– f S0 u – ƒu S0d – ƒd The portfolio is riskless when S0u – ƒu = S0d – ƒd or ƒu f d S0 u S0 d 2005年秋 北航金融系李平 207 Generalization (continued) 2005年秋 Value of the portfolio at time T is S0u – ƒu Value of the portfolio today is (S0u – ƒu )e–rT Another expression for the portfolio value today is S0 – f Hence ƒ = S0 – (S0u – ƒu )e–rT 北航金融系李平 208 Generalization (continued) Substituting for we obtain ƒ = [ p ƒu + (1 – p )ƒd ]e–rT where e d p ud rT 2005年秋 北航金融系李平 209 Risk-Neutral Valuation ƒ = [ p ƒu + (1 – p )ƒd ]e-rT The variables p and (1 – p ) can be interpreted as the risk-neutral probabilities of up and down movements The value of a derivative is its expected payoff in a risk-neutral world discounted at the risk-free rate S0 ƒ 2005年秋 S 0u ƒu S 0d ƒd 北航金融系李平 210 Irrelevance of Stock’s Expected Return When we are valuing an option in terms of the underlying stock the expected return on the stock is irrelevant 2005年秋 北航金融系李平 211 Original Example Revisited S0 ƒ S0u = 22 ƒu = 1 S0d = 18 ƒd = 0 One way is to use the formula e rT d e 0.120.25 0.9 p 0.6523 ud 1.1 0.9 2005年秋 Alternatively, since p is a risk-neutral probability 20e0.12 ´0.25 = 22p + 18(1 – p ); p = 0.6523 北航金融系李平 212 Valuing the Option S0u = 22 ƒu = 1 S0 ƒ S0d = 18 ƒd = 0 The value of the option is e–0.12´0.25 [0.6523´1 + 0.3477´0] = 0.633 2005年秋 北航金融系李平 213 A Two-Step Example 24.2 22 19.8 20 18 16.2 2005年秋 Each time step is 3 months 北航金融系李平 214 Valuing a Call Option D 22 24.2 3.2 B 20 1.2823 2005年秋 2.0257 A E 19.8 0.0 F 16.2 0.0 18 C 0.0 Value at node B = e–0.12´0.25(0.6523´3.2 + 0.3477´0) = 2.0257 Value at node A = e–0.12´0.25(0.6523´2.0257 + 0.3477´0) = 1.2823 北航金融系李平 215 A Put Option Example; K=52 60 50 4.1923 A E 48 4 B 1.4147 40 D 72 0 C 9.4636 F 2005年秋 北航金融系李平 32 20 216 What Happens When an Option is American Procedure: work back through the tree from the end to the beginning, testing at each node to see whether early exercise is optimal. The value at the final nodes is the same as for the European. At earlier nodes the value is the greater of 2005年秋 The value given as an European; The payoff from early exercise. 北航金融系李平 217 An American Put Option Example; K=52 D 60 50 5.0894 A B 1.4147 40 48 4 E C 12.0 F 2005年秋 72 0 北航金融系李平 32 20 218 Examples 1. S0=$40, T=1m, ST=$42 or $38, r=8% per annum (cont comp), what is the value of a 1-m European call with K=$39? Use both of the no-arbitrage argument and the risk-neutral argument. 1.69 2005年秋 北航金融系李平 219 Examples 2. S0=$100. Over each of the next two sixmonth periods it is expected to go up by 10%, or go down by 10%, r=8% per annum (cont comp), what are the value of a one-year European call and a one-year European put with K=$100? Verify the put-call parity. 1.92, 9.61 2005年秋 北航金融系李平 220 Examples 3. S0=$25, T=2m, ST=$23 or $27, r=10% per annum (cont comp), what is the value of a derivative that pays off ST2 at the end of two months? 639.3 2005年秋 北航金融系李平 221 Chapter 11 Model of the Behavior of Stock Prices 2005年秋 北航金融系李平 222 Categorization of Stochastic Processes 2005年秋 Discrete time; discrete variable Discrete time; continuous variable Continuous time; discrete variable Continuous time; continuous variable 北航金融系李平 223 Modeling Stock Prices 2005年秋 We can use any of the four types of stochastic processes to model stock prices 北航金融系李平 224 Markov Processes In a Markov process future movements in a variable depend only on where we are, not the history of how we got where we are We assume that stock prices follow Markov processes 2005年秋 北航金融系李平 225 Weak-Form Market Efficiency This asserts that it is impossible to produce consistently superior returns with a trading rule based on the past history of stock prices. In other words technical analysis does not work. A Markov process for stock prices is clearly consistent with weak-form market efficiency 2005年秋 北航金融系李平 226 Example of a Discrete Time Continuous Variable Model 2005年秋 A stock price is currently at $40 At the end of 1 year it is considered that it will have a probability distribution of f(40,10) where f(m,s) is a normal distribution with mean m and standard deviation s. 北航金融系李平 227 Questions What is the probability distribution of the stock price at the end of 2 years? ½ years? ¼ years? dt years? Taking limits we have defined a continuous variable, continuous time process 2005年秋 北航金融系李平 228 Variances & Standard Deviations In Markov processes changes in successive periods of time are independent This means that variances are additive Standard deviations are not additive 2005年秋 北航金融系李平 229 Variances & Standard Deviations (continued) In our example it is correct to say that the variance is 100 per year. It is strictly speaking not correct to say that the standard deviation is 10 per year. 2005年秋 北航金融系李平 230 A Wiener Process We consider a variable W whose value changes continuously The change in a small interval of time dt is dW The variable W follows a Wiener process if 1. d W d t where is a random drawing from f (0,1) 2. The values of dW for any 2 different (nonoverlapping) periods of time are independent 2005年秋 北航金融系李平 231 Properties of a Wiener Process 2005年秋 Mean of [W(T ) – W(0)] is 0 Variance of [W(T ) – W(0)] is T Standard deviation of [W(T ) – W(0)] is 北航金融系李平 T 232 Taking Limits . . . What does an expression involving dW and dt mean? It should be interpreted as meaning that the corresponding expression involving dW and dt is true in the limit as dt tends to zero 2005年秋 北航金融系李平 233 Generalized Wiener Processes A Wiener process has a drift rate (i.e. average change per unit time) of 0 and a variance rate of 1 In a generalized Wiener process the drift rate and the variance rate can be set equal to any chosen constants 2005年秋 北航金融系李平 234 Generalized Wiener Processes The variable X follows a generalized Wiener process with a drift rate of a and a variance rate of b2 if dX=adt+bdW 2005年秋 北航金融系李平 235 Generalized Wiener Processes d X ad t b d t Mean change in X in time T is aT Variance of change in X in time T is b2T Standard deviation of change in X in time T is b T 2005年秋 北航金融系李平 236 The Example Revisited A stock price starts at 40 and has a probability distribution of f(40,10) at the end of the year If we assume the stochastic process is Markov with no drift then the process is dS = 10dW If the stock price were expected to grow by $8 on average during the year, so that the yearend distribution is f(48,10), the process is dS = 8dt + 10dW 2005年秋 北航金融系李平 237 Ito Process In an Ito process the drift rate and the variance rate are functions of time dX=a(X,t)dt+b(X,t)dW The discrete time equivalent d X a( X , t )d t b( X , t ) d t is only true in the limit as dt tends to zero 2005年秋 北航金融系李平 238 Why a Generalized Wiener Process is not Appropriate for Stocks For a stock price we can conjecture that its expected percentage change in a short period of time remains constant, not its expected absolute change in a short period of time We can also conjecture that our uncertainty as to the size of future stock price movements is proportional to the level of the stock price 2005年秋 北航金融系李平 239 An Ito Process for Stock Prices The well-known Geometric Brownian Motion dS mSdt sSdW where m is the expected return, s is the volatility. The discrete time equivalent is dS mSdt sS dt 2005年秋 北航金融系李平 240 Monte Carlo Simulation We can sample random paths for the stock price by sampling values for Suppose m= 0.14, s= 0.20, and dt = 0.01, then dS 0.0014S 0.02 S 2005年秋 北航金融系李平 241 Monte Carlo Simulation – One Path Period 2005年秋 Stock Price at Random Start of Period Sample for Change in Stock Price, S 0 20.000 0.52 0.236 1 20.236 1.44 0.611 2 20.847 -0.86 -0.329 3 20.518 1.46 0.628 4 21.146 -0.69 -0.262 北航金融系李平 242 Ito’s Lemma If we know the stochastic process followed by X, Ito’s lemma tells us the stochastic process followed by some function f (X, t ) Since a derivative security is a function of the price of the underlying and time, Ito’s lemma plays an important part in the analysis of derivative securities 2005年秋 北航金融系李平 243 Taylor Series Expansion A Taylor’s series expansion of f(X, t) gives f f 2f 2 d f dX d t ½ (d X ) 2 x t x 2f 2f d Xd t ½ 2 (d t ) 2 x t t 2005年秋 北航金融系李平 244 Ignoring Terms of Higher Order Than dt In ordinary calculus we have f f df dx dt x t In stochastic calculus this becomes f f 2f df dX dt ½ (d X ) 2 x t x2 because dX has a component which is of order 2005年秋 dt 北航金融系李平 245 Substituting for dX Suppose dx a ( x, t )dt b( x, t )dz so that d X = ad t +b d t Then ignoring terms of higher order than d t f f 2f 2 2 d f d X d t ½ b dt 2 x t x 2005年秋 北航金融系李平 246 The 2dt Term Since f (0,1) E ( ) 0 E ( 2 ) [ E ( )] 2 1 E ( 2 ) 1 It follows that E ( 2dt ) dt The variance of d t is proportional to d t 2 and can be ignored. Hence f f 12f 2 d f d x d t b dt 2 x t 2 x 2005年秋 北航金融系李平 247 Taking Limits Taking limits Substituting We obtain 2005年秋 f f 2f 2 df dX dt b dt x t x2 dX a dt b dW 2 f f f f 2 df a b dt b dW 2 x t x x This is Ito' s Lemma 北航金融系李平 248 Application of Ito’s Lemma to a Stock Price Process The stock price process is d S m S dt s S dW For a function f of S and t 2 f f f f 2 2 df mS ½ s S dt s S dW 2 S t S S 2005年秋 北航金融系李平 249 Examples 1. The forward price of a stock for a contract maturing at time T f S e r (T t ) df ( m r ) f dt sf dW 2. f ln S 2 s dt s dW df m 2 2005年秋 北航金融系李平 250 The lognormal property From Example 2, ln ST ln S 0 ~ f (( m s2 2 )T , s T ) or, ln ST ~ f (ln S 0 ( m s2 2 )T , s T ) Since the logarithm of ST is normal, ST is lognormally distributed 2005年秋 北航金融系李平 251 The Lognormal Distribution (cont.) E ( ST ) S0 e mT 2 2 mT var ( ST ) S0 e (e s2T 1) Example Consider a stock with an initial price of $40, an expected return of 16% per annum, and a volatility of 20% per annum, then the probability distribution of the stock price, ST, in six months’ time is given by The confidence interval for the stock price in six month with the probability of 95% is 2005年秋 北航金融系李平 253 Continuously Compounded Return ST S0 e T or 1 ST = ln T S0 or s2 f m , 2 2005年秋 s T 北航金融系李平 254 The Expected Return The expected value of the stock price is S0emT The expected return on the stock is m – s2/2 Eln( ST / S0 ) m s / 2 2 ln E ( ST / S0 ) m 2005年秋 北航金融系李平 255 The Volatility The volatility of an asset is the standard deviation of the continuously compounded rate of return in 1 year As an approximation it is the standard deviation of the percentage change in the asset price in 1 year 2005年秋 北航金融系李平 256 Estimating Volatility from Historical Data 1. 2. Take observations S0, S1, . . . , Sn at intervals of t years Calculate the continuously compounded return in each interval as: Si ui ln Si 1 3. 4. Calculate the standard deviation, s , of the ui´s The historical volatility estimate is: sˆ s t 2005年秋 北航金融系李平 257 Chapter 12-13 Black-Scholes Model 2005年秋 北航金融系李平 258 1. Black-Scholes Formula The Concepts Underlying Black-Scholes: The option price and the stock price depend on the same underlying source of uncertainty We can form a portfolio consisting of the stock and the option which eliminates this source of uncertainty The portfolio is instantaneously riskless and must instantaneously earn the risk-free rate 2005年秋 北航金融系李平 259 The Derivation of the BlackScholes Differential Equation d S mS d t sS d W f ƒ 2 ƒ 2 2 ƒ d ƒ mS ½ 2 s S d t sS d W t S S S We set up a portfolio consisting of 1 : derivative f + : shares S 2005年秋 北航金融系李平 260 The Derivation of the Black-Scholes Differential Equation (cont.) The value of the portfolio is given by ƒ ƒ S S The change in its value in time d t is given by ƒ d d ƒ dS S 2005年秋 北航金融系李平 261 The Derivation of the Black-Scholes Differential Equation (cont.) The return on the portfolio must be the risk - free rate. Hence d r d t We substitute for d ƒ and d S in these equations to get the Black - Scholes differenti al equation : ƒ ƒ 2 2 ƒ rS ½s S rƒ 2 t S S 2 2005年秋 北航金融系李平 262 The Differential Equation Any security whose price is dependent on the stock price satisfies the differential equation The particular security being valued is determined by the boundary conditions of the differential equation For European call option, the boundary condition is fT=max(0, ST-K) 2005年秋 北航金融系李平 263 Risk-Neutral Valuation The variable m does not appear in the Black-Scholes equation The equation is independent of all variables affected by risk preference The solution to the differential equation is therefore the same in a risk-free world as it is in the real world This leads to the principle of risk-neutral valuation 2005年秋 北航金融系李平 264 Applying Risk-Neutral Valuation 1. Assume that the expected return from the stock price is the risk-free rate r 2. Calculate the expected payoff from the option 3. Discount at the risk-free rate f0 e rT Eˆ ( fT ) where Ê is the expectation under a risk-neutral probability measure P̂ 2005年秋 北航金融系李平 265 The Black-Scholes Formulas c S 0 N (d1 ) K e rT N (d 2 ) p K e rT N (d 2 ) S 0 N (d1 ) 2 ln( S 0 / K ) (r s / 2)T where d1 s T ln( S 0 / K ) (r s 2 / 2)T d2 d1 s T s T 2005年秋 北航金融系李平 266 Implied Volatility The implied volatility of an option is the volatility for which the Black-Scholes price equals the market price There is a one-to-one correspondence between prices and implied volatilities Traders and brokers often quote implied volatilities rather than dollar prices 2005年秋 北航金融系李平 267 2. Dividends European options on dividend-paying stocks are valued by substituting the stock price less the present value of dividends into BlackScholes Only dividends with ex-dividend dates during life of option should be included The “dividend” should be the expected reduction in the stock price expected 2005年秋 北航金融系李平 268 European Options on Stocks Providing Dividend Yield (cont.) We get the same probability distribution for the stock price at time T in each of the following cases: 1. The stock starts at price S0 and provides a dividend yield = q 2. The stock starts at price S0e–q T and provides no income We can value European options by reducing the stock price to S0e–q T and then behaving as though there is no dividend 2005年秋 北航金融系李平 269 Prices for European Options on Stocks Providing Dividend Yield c S0e qT N (d1 ) Ke rT N (d 2 ) p Ke rT N (d 2 ) S0e qT N (d1 ) ln( S0 / K ) (r q s 2 / 2)T where d1 s T ln( S0 / K ) (r q s 2 / 2)T d2 s T 2005年秋 北航金融系李平 270 3. Valuing European Index Options We can use the formula for an option on a stock paying a dividend yield 2005年秋 Set S0 = current index level Set q = average dividend yield expected during the life of the option 北航金融系李平 271 4. The Foreign Interest Rate We denote the foreign interest rate by rf When a U.S. company buys one unit of the foreign currency it has an investment of S0 dollars The return from investing at the foreign rate is rf S0 dollars This shows that the foreign currency provides a “dividend yield” at rate rf 2005年秋 北航金融系李平 272 Valuing European Currency Options A foreign currency is an asset that provides a “dividend yield” equal to rf We can use the formula for an option on a stock paying a dividend yield: Set S0 = current exchange rate Set q = rƒ 2005年秋 北航金融系李平 273 Formulas for European Currency Options c S 0e p Ke r f T rT N (d1 ) Ke rT N (d 2 ) N (d 2 ) S0e where d1 d2 2005年秋 r f T N (d1 ) ln( S0 / K ) (r r f s 2 / 2)T s T ln( S0 / K ) (r r f s 2 / 2)T s T 北航金融系李平 274 Alternative Formulas Using F0 S0 e ( r rf ) T c e rT [ F0 N (d1 ) KN (d 2 )] p e rT [ KN ( d 2 ) F0 N ( d1 )] ln( F0 / K ) s 2T / 2 d1 s T d 2 d1 s T 2005年秋 北航金融系李平 275 5. Mechanics of Call Futures Options When a call futures option is exercised the holder acquires 1. A long position in the futures 2. A cash amount equal to the excess of the futures price over the strike price 2005年秋 北航金融系李平 276 Mechanics of Put Futures Option When a put futures option is exercised the holder acquires 1. A short position in the futures 2. A cash amount equal to the excess of the strike price over the futures price 2005年秋 北航金融系李平 277 The Payoffs If the futures position is closed out immediately: Payoff from call = F0 – K Payoff from put = K – F0 where F0 is futures price at time of exercise 2005年秋 北航金融系李平 278 Put-Call Parity for Futures Options Consider the following two portfolios: 1. European call on futures + Ke-rT of cash 2. European put on futures + long futures + cash equal to F0e-rT They must be worth the same at time T so that c+Ke-rT=p+F0 e-rT 2005年秋 北航金融系李平 279 Binomial Tree Model A derivative lasts for time T and is dependent on a futures price F0 ƒ F0u ƒu F0d ƒd 2005年秋 北航金融系李平 280 Binomial Tree Model (cont.) Consider the portfolio that is long futures and short 1 derivative F0u F0 – ƒu F0d F0 – ƒd The portfolio is riskless when ƒu f d F0u F0d 2005年秋 北航金融系李平 281 Binomial Tree Model (cont.) 2005年秋 Value of the portfolio at time T is F0u –F0 – ƒu Value of portfolio today is – ƒ Hence ƒ = – [F0u –F0 – ƒu]e-rT 北航金融系李平 282 Binomial Tree Model (cont.) Substituting for we obtain ƒ = [ p ƒu + (1 – p )ƒd ]e–rT where 1 d p ud 2005年秋 北航金融系李平 283 Pricing by Binomial Tree Model ƒ = [ p ƒu + (1 – p )ƒd ]e–rT where 1 d p ud 2005年秋 北航金融系李平 284 Valuing European Futures Options We can use the formula for an option on a stock paying a dividend yield Set S0 = current futures price (F0) 2005年秋 Set q = domestic risk-free rate (r ) Setting q = r ensures that the expected growth of F in a risk-neutral world is zero 北航金融系李平 285 Growth Rates For Futures Prices A futures contract requires no initial investment In a risk-neutral world the expected return should be zero The expected growth rate of the futures price is therefore zero The futures price can therefore be treated like a stock paying a dividend yield of r 2005年秋 北航金融系李平 286 Black’s Formula The formulas for European options on futures are known as Black’s formulas c e rT F0 N (d1 ) K N (d 2 ) p e rT K N (d 2 ) F0 N (d1 ) ln( F0 / K ) s 2T / 2 where d1 s T ln( F0 / K ) s 2T / 2 d2 d1 s T s T 2005年秋 北航金融系李平 287 Summary of Key Results We can treat stock indices, currencies, and futures like a stock paying a dividend yield of q For stock indices, q= average dividend yield on the index over the option life For currencies, q= rƒ For futures, q= r 2005年秋 北航金融系李平 288 Chapter 14 The Greek Letters 2005年秋 北航金融系李平 289 The problem to the option writer: managing the risk Each Greek letter measures a different dimension to the risk in an option position The aim of a trader: manage the Greek letters so that all risks are acceptable 2005年秋 北航金融系李平 290 An Example A bank has sold for $300,000 a European call option on 100,000 shares of a nondividend paying stock S0 = 49, K = 50, r = 5%, s = 20%, T = 20 weeks (0.3846y), m = 13% The Black-Scholes value of the option is $240,000 The bank get $60,000 more than the theoretical value, but it is faced the problem of hedging the risk. 2005年秋 北航金融系李平 291 Naked & Covered Positions Naked position: Take no action, works well when ST <50, otherwise (e.g. ST=60), lose (60-50)* 100,000 Covered position Buy 100,000 shares today works well when exercised (ST >50), otherwise (e.g. ST=40), lose (59-40)* 100,000 Neither strategy provides a satisfactory hedge, most traders employ Greek letters. 2005年秋 北航金融系李平 292 Delta () Delta is the rate of change of the option price with respect to the underlying Option price Slope = B A 2005年秋 北航金融系李平 Stock price 293 Example S=100, c=10, =0.6 An investor sold 20 calls, this position could be hedged by buying 0.6*2000=1200 shares The gain (lose) on the option position will be offset by the lose (gain) on the stock position Delta of a call on a stock (0.6) delta of the short option position (-2000*0.6) delta of the long share position 2005年秋 北航金融系李平 294 Delta Hedging This involves maintaining a delta neutral portfolio--- =0 In Black-Scholes model, -1: option + : shares set up a delta neutral portfolio 2005年秋 北航金融系李平 295 Delta Hedging (cont.) The delta of a European call on a nondividend-paying stock: =N (d 1)>0 Short position in a call should be hedged by a long position on shares The delta of a European put is = - N (-d 1) =N (d 1) – 1<0 Short position in a put should be hedged by a short position on shares 2005年秋 北航金融系李平 296 Delta Hedging (cont.) The variation of delta w.r.t the stock price The hedge position must be frequently rebalanced In the example, when S increase from $100 to $110, the delta will increase from 0.6 to 0.65, then an extra 0.05*2000=100 shares should be purchased to maintain the hedge 2005年秋 北航金融系李平 297 Delta for other European options 2005年秋 Call on asset paying yield q =e-qt N (d 1) For put = e-qt [N (d 1) -1] For index option, foreign currency options and futures options Delta of a portfolio wi i S i 北航金融系李平 298 Gamma (G) c G 2 S S 2 2005年秋 Gamma is always positive (for buyer), negative for writer If gamma is large, delta is highly sensitive to the stock price, then it will be quite risky to leave a delta-neutral portfolio unchanged. 北航金融系李平 299 Gamma Addresses Delta Hedging Errors Caused By Curvature Call price C’’ C’ C Stock price S 2005年秋 北航金融系李平 S ’ 300 Making a portfolio gamma neutral 2005年秋 The gamma of the underlying asset is 0, so it can’t be used to change the gamma of a portfolio. What is required is an instrument such as an option which is not linearly dependent on the underlying asset. 北航金融系李平 301 Gamma hedging Suppose the gamma of a delta-neutral portfolio is G, the gamma of a traded option is GT, then the gamma of a new portfolio with the number of wT options added is wT GT + G In order that the new portfolio is gamma neutral, the number of the options should be wT= - G/GT 2005年秋 北航金融系李平 302 Gamma hedging (cont.) Including the traded option will change the delta of the portfolio, so the position in the underlying asset has to be changed to maintain delta neutral. The portfolio is gamma neutral only for a short period of time. As time passes, gamma neutrality can be maintained only when the position in the option is adjusted so that it is always equal to - G/GT. 2005年秋 北航金融系李平 303 An example Suppose that a portfolio is delta neutral and has a gamma of –3000. The delta and gamma of a particular traded call are 0.62 and 1.5. The portfolio can be made gamma neutral by including in the portfolio a long position of 2000(=-[-3000/1.5]). 2005年秋 北航金融系李平 304 Example (cont.) The delta of the new portfolio will change from 0 to 2000*0.62=1240. A quantity of 1240 of the underlying asset must be sold from the portfolio to keep it delta neutral. 2005年秋 北航金融系李平 305 Theta (Q) Theta of a derivative is the rate of change of the value with respect to the passage of time with all else remain the same, often referred to as the time decay of the option In practice, when theta is quoted, time is measured in days so that theta is the change in the option value when one day passes. Theta is usually negative for an option, since as time passes, the option tends to be less valuable. 2005年秋 北航金融系李平 306 Vega (n) c n s If n is the vega of a portfolio and nT is the vega of a traded option, a position of –n/nT in the traded option makes the portfolio vega neutral. If a hedger requires a portfolio to be both gamma and vega neutral, at least two traded derivatives dependent on the underlying asset must be used. 2005年秋 北航金融系李平 307 Rho (r) c r r For currency options there are 2 rhos For a European call r r KTe rT N (d 2 ) r r Te f 2005年秋 rf T SN (d1 ) 北航金融系李平 308 Hedging in Practice Traders usually ensure that their portfolios are delta-neutral at least once a day. Zero gamma and zero vega are less easy to achieve because of the difficulty of finding suitable options. Whenever the opportunity arises, they improve gamma and vega As portfolio becomes larger hedging becomes less expensive 2005年秋 北航金融系李平 309 Chapter 19 Exotic Options 2005年秋 北航金融系李平 310 Packages Asian options Options to exchange one asset for another Binary options Rainbow options Lookback options Barrier options 2005年秋 Compound options Nonstandard American options Forward start options Chooser options Shout options 北航金融系李平 311 Packages Portfolios of standard options, forward contract, cash and the underlying asset Examples: bull spreads, bear spreads, straddles, etc Often structured to have zero cost One popular package is a range forward contract 2005年秋 北航金融系李平 312 Range forward contract Popular in foreign-exchange markets Long/short-range forward = a short/long put with the low strike price + a long/short call with the high strike price The prices of the call and the put are equal when the contract is initiated A long-range forward guarantees the underlying asset be purchased for a price between two strikes at the maturity When K1 and K2 are moved closer, the price becomes more certain 2005年秋 北航金融系李平 313 Payoff from a long range forward Profit S K1 2005年秋 北航金融系李平 K2 T 314 Asian Options Payoff related to the average price of the underlying during some period Payoffs: 2005年秋 max(Save – K, 0) (average price call), max(K – Save , 0) (average price put) max(ST – Save , 0) (average strike call), max(Save – ST , 0) (average strike put) 北航金融系李平 315 Asian Options (cont.) Average price options are less expensive and sometimes are more appropriate than regular options Average strike call (put) can guarantee that the average price paid (received) for an asset in frequent trading over a period of time is not greater (less) than the final price 2005年秋 北航金融系李平 316 Exchange Options Option to exchange one asset for another For example, an option to give up Japanese yen worth UT at time T and receive in return Australian dollars worth VT Payoff= max(VT – UT, 0) 2005年秋 北航金融系李平 317 Binary Options Cash-or-nothing call: Cash-or-nothing put: 2005年秋 Pays off a fixed amount Q if ST > K, otherwise pays off 0, Value = e–rT Q N(d2) Pays off a fixed amount Q if ST < K, otherwise pays off 0, Value = e–rT Q N(-d2) 北航金融系李平 318 Binary Options (cont.) Asset-or-nothing call: pays off ST (an amount equal to the asset price) if ST > K, otherwise pays off 0. Value = S0 N(d1) Asset-or-nothing put: 2005年秋 pays off ST (an amount equal to the asset price) if ST < K, otherwise pays off 0. Value = S0 N(-d1) 北航金融系李平 319 Rainbow options Options involving two or more risky assets The most popular rainbow option--Basket Options: whose payoff is dependent on the value of a portfolio of assets (stocks, indices, currencies) 2005年秋 北航金融系李平 320 Lookback Options Payoff from an European lookback call: ST – Smin Allows buyer to buy stocks at the lowest observed price in some interval of time Payoff from a lookback put: Smax– ST 2005年秋 Allows buyer to sell stocks at the highest observed price in some interval of time 北航金融系李平 321 Barrier Options Option comes into existence only if the asset price hits barrier before option maturity ‘In’ options Option dies if the asset price hits barrier before option maturity 2005年秋 ‘Out’ options 北航金融系李平 322 Barrier Options (cont.) barrier level above the asset price barrier level below the asset price 2005年秋 ‘Up’ options ‘Down’ options Option may be a put or a call Eight possible combinations 北航金融系李平 323 Barrier Options (cont.) Up-and-in call Up-and-in put Down-and-in call Down-and-in put 2005年秋 Up-and-out call Up-and-out put Down-and-out call Down-and-out put 北航金融系李平 324 Compound Option Option to buy / sell an option Two strikes and two maturities 2005年秋 Call on call Put on call Call on put Put on put 北航金融系李平 325 Non-Standard American Options Exercisable only on specific dates--Bermudan option Early exercise allowed during only part of life Strike price changes over the life Exm: a seven-year warrant issued by a corporation on its own stocks 2005年秋 北航金融系李平 326 Chooser Option “As you like it” option Option starts at time 0, matures at T2 At T1 (0 < T1 < T2) buyer chooses whether it is a put or call The value of the chooser option at time T1: Max(c,p) where c and p are the values of the call and put underlying the chooser option. 2005年秋 北航金融系李平 327 Chooser Option If the call and the put underlying the chooser option are both European and have the same strike price K, then put-call parity implies that max( c, p) max( c, c Ke r (T2 T1 ) S1 ) c max(0, Ke r (T2 T1 ) S1 ) Thus the chooser option is a package of 2005年秋 A call option with strike price K and maturity T2 A put option with strike price Ke r (T2 T1 ) and maturity T1 北航金融系李平 328 Shout Options A European call option where the holder can ‘shout’ to the writer once during the option life The final payoff of a call is the maximum of The usual European option payoff, max(ST – K, 0), or Intrinsic value at the time of shout, St – K Example: K=50, St=60, when ST<60, the payoff is 10; when ST>60, the payoff is Similar to a lookback option, but is cheaper 2005年秋 北航金融系李平 329 Forward Start Options Option starting at a future time, used in employee incentive schemes Usually be at the money at the time they start 2005年秋 北航金融系李平 330 Example: Standard Oil’s Bond It is a bond issued by Standard Oil The holder receives no interest. At the maturity the company promised to pay $1000 plus an additional amount based on the price of oil at that time. The additional amount was equal to the product of 170 and the excess (if any) of the price of oil at maturity over $25. The maximum additional amount paid was $2250 (which corresponds to a price of $40) 2005年秋 北航金融系李平 331 Standard Oil’s Bond Show that this bond is a combination of a regular bond, a long position in call options on oil with a strike price of $25 and a short position in call options on oil with a strike price of $40. Relationship between a spread option 2005年秋 北航金融系李平 332