Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

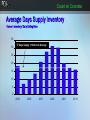

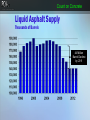

Count on Concrete Cement Outlook: 2009 Ed Sullivan, Chief Economist PCA CCoun Count on Concrete Key Questions How deep will retrenchment go ? How long will it last ? What recovery to expect? CCoun Count on Concrete Portland Cement Consumption Thousand Metric Tons Declines Continue Through 2010. One Year Later than Previously Expected CCoun Count on Concrete Portland Cement Consumption - Annual Change, Thousand Tons Peak (2005)-to-Trough (2010) Decline: 41 MMT (Worst in History) CCoun Count on Concrete Capacity Expansion Thousand Metric Tons Stated Capacity Expansions Potential Increases From Specification Changes CCoun Count on Concrete Market Imbalances - Changes in Cement Consumption Tons + Capacity Expansion Tons 25,000,000 20,000,000 15,000,000 2007 1974 1991 10,000,000 1981 2002 5,000,000 0 -5,000,000 -10,000,000 1980-82 1990-91 2000-01 2007-2010 -15,000,000 1970 1973-74 1980 1990 2000 2010 CCoun Import Volume Thousand Metric Tons Count on Concrete CCoun Count on Concrete Capacity Adjustments * Thousand Metric Tons Capacity Adjustments Due to Delayed Expansions and Plant Closures * Adjustments Include Five Delays in Plant Commissioning and Seven Plant Closures CCoun Count on Concrete Average Days Supply Inventory Cement Inventory/ Daily Selling Rate 35 30 17 Days Supply = Historical Average 25 20 15 10 5 0 2003 2005 2007 2009 2011 2013 CCoun Capacity Utilization Rates Clinker Production/Clinker Capacity Count on Concrete Count on Concrete Economic Outlook It is a Recession, and going to last longer than previously expected CCoun Count on Concrete Economic Outlook: Five Factors Sub-Prime Mortgage Payments Financial Crisis Energy/ Inflation Defaults Structural Global Realities Write-Downs Credit Cards Gasoline Prices Risk Aversion Defaults Tight Lending Standards Home Price Declines Reliance on Home Equity Gone Heating Prices Tight Lending Standards Fertilizer/Biofuels hit Ag Prices Commercial, Consumer, homeowner capital access reduced Supply Side Costs Ingrained Cost of Business Global Adds Weakness to Dollar Labor Markets Slower Economic Growth State Deficits Slower Job Revenues Slow One Million Job Loss in 2008 Housing Recovery Delayed Nonresidential Declines State Fiscal Crisis Looming Public Declines Entitlement Programs Continue Deficits Drag on Recovery Offsets Possible Federal Stimulus Package CCoun Count on Concrete Economic Adversity 2006 Sub-Prime Energy Financial Crisis Inflation Labor Markets State Deficits 2007 2008 2009 2010 CCoun Count on Concrete Net Job Creation (Loss) - Annual Change, Thousand Net Jobs Job Loss 2008 = 1.4 Million Job Loss 2009 = 1.9 Million Unemployment Peaks at 7.5% Mid-2009 CCoun Count on Concrete Economic Growth Outlook Percent Change, GDP Growth Rate Tax Rebate Bump CCoun Count on Concrete Count on Concrete Economic Policy Impacts CCoun Count on Concrete Left to Itself…Adverse Economic Momentum will Accelerate….Leading to Potentially the Worst economic Downturn in Post-War Era… The Effectiveness of Policy Will Determine the Character of the Economy during the Two Years CCoun Count on Concrete Transmission Mechanism: Simple/Effective $700 Billion Increased Liquidity Banks Stronger Stronger Economy Averts Economic Meltdown: But May have Muted Impact in Stimulating Economy CCoun Count on Concrete Transmission Mechanism: Longer/Weaker $700 Billion Increased Liquidity Banks Stronger Reduced Risk Aversion Compromises Liquidity Lending Risk Increases Further Write downs Economy Weakens Stronger Economy Longer Financial Adjustment Period Than Many Expect: Begins late 2009 CCoun Count on Concrete Policy Assessments Rebate impact of spring has dissipated. Stimulatory impact of rate cuts waning and not as effective as historical measures. Issue not level of interest rates Financial bailout is a stop gap measure not a true stimulus policy. Economic adversity gains momentum in absence of a major fiscal policy initiative. First half 2009 action. $150 Billion. Infrastructure – Higher “Multipiers” Will increased Federal spending work in the face of large cuts in state and local spending? Aid to States Count on Concrete Residential Outlook Recovery Delayed CCoun Single Family Housing– United States 000 Starts Count on Concrete CCoun Count on Concrete Residential Cement Consumption - Annual Change, Thousand Tons Peak (2005)-to-Trough (2010) Decline: 19 MMT = 63% of Total Decline CCoun Count on Concrete Future Weakness Residential Weakness is largely over. Most of Future Weakness Tied to Nonresidential & Public Cement Consumption. CCoun Count on Concrete Nonresidential Construction CCoun Count on Concrete Nonresidential: Portland Cement Consumption Thousand Metric Tons Declines Continue Through 2010. Colorado Nonresidential Cement Consumption 2007: +7.8% 2008: +6.5% 2009:-22.0% 2010: -11.3% 2011: +4.6% Recovery Could be Strong CCoun Count on Concrete Nonresidential Cement Consumption - Annual Change, Thousand Tons Peak (2005)-to-Trough (2010) Decline: 5 MMT CCoun Count on Concrete Public Construction CCoun Count on Concrete Fiscal 2009 Revenue Outlook District of Columbia Pessimistic Concerned Source: National Conference of State Legislatures Stable Optimistic CCoun Count on Concrete Public Cement Consumption - Annual Change, Thousand Tons Peak (2005)-to-Trough (2010) Decline: 12 MMT Count on Concrete Mid-Term Recovery 2011-2013 CCoun Count on Concrete Portland Cement Consumption Thousand Metric Tons Declines Continue Through 2010. One Year Later than Previously Expected CCoun Count on Concrete The “V” Economic Recovery: 2008 Sub-Prime Drag Abates Bank Lending Aversion Improves Stimulus Gains Employment Traction Lending Risk Declines: Credit Easing Energy Stimulus State Deficits Improve Pent-Up Demand Released 2009 2010 2011 CCoun Count on Concrete Single Family Housing– United States 000 Starts Pent-Up Demand Interest Rates low, Decline in Home Price, Job Recovery Translate into Improved Affordability Excess Inventories Worked Off CCoun Count on Concrete Nonresidential Long Term Trend Million Real $, 1996 CCoun Count on Concrete Current: Gasoline Prices Vs Asphalt Prices Per Barrel Price Per Barrel CCoun Count on Concrete Gasoline - Asphalt Margin Per Barrel Differential - Net Threshold of $14 Per Barrel Price Differential Per Barrel Threshold Differential = $14 per barrel Estimated on a Ten Year Payoff for Coker Investment CCoun Count on Concrete Announced New Coker Installations Cumulative: Thousands of Barrels Per Day CCoun Count on Concrete Liquid Asphalt Supply Thousands of Barrels 44 Million Barrel Decline by 2011 CCoun Count on Concrete Projected: Initial Bid Concrete Vs Asphalt Paving Costs Per Two Lane Road Mile - Urban Asphalt Concrete Parity Achieved in Fiscal 2009 CCoun Count on Concrete Projected: Life Cycle Concrete Vs Asphalt Paving Costs Per Two Lane Road Mile - Urban Asphalt Concrete Concrete Advantages Materialize in Fiscal 2009 CCoun Count on Concrete Portland Cement Consumption Thousand Metric Tons 140,450 120,450 100,450 80,450 60,450 40,450 20,450 450 1998 2000 2002 2004 2006 2008 2010 2012 Count on Concrete Cement Outlook: 2009 Ed Sullivan, Chief Economist PCA