Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

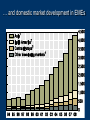

CAPITAL FLOWS AND MACROPRUDENTIAL REGULATION José Antonio Ocampo Columbia University CHARACTERISTICS OF CAPITAL FLOWS IMF WEO: Capital flows are erratic (fickle) Volatility has increased over time and is higher for EMEs than for AEs Flows towards EMEs are highly sensitive to monetary policy in AEs, and to risk perception Different types of flows differ in terms of volatility and persistence (though differences have narrowed down) Recent surge is peculiar because of pace rather than level Bank and portfolio flows are highly sensitive to interest/risk mix 3.5 Bank and other 3 Net portfolio debt Net portfolio equity 2.5 Net FDI 2 1.5 1 0.5 0 -0.5 -1 Low interest, low risk Low interest, high risk High interest, low risk High interest, high risk Debt portfolio flows are the distinctive feature of the recent surge in Latin America Emerging Asia Emerging Latin America 4.5 4.5 4 4 3.5 3.5 3 3 2.5 2.5 2 2 1.5 1.5 1 1 0.5 0.5 0 0 -0.5 1991–97 2004–07 FDI Portfolio equity Portfolio debt 2010 Q1-Q3 Bank and others -0.5 1991–97 2004–07 FDI Portfolio equity Portfolio debt 2010 Q1-Q3 Bank and other Volatility has increased, particularly for FDI. Persistence is low and has declined. Volatility FDI Portfolio equity Portfolio debt Bank and other FDI Portfolio equity Portfolio debt Bank and other 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 -0.1 1991 2009 2008 2007 2006 2005 2004 0 2003 0 2002 0.1 2001 0.5 2000 0.2 1999 1 1998 0.3 1997 1.5 1996 0.4 1995 2 1994 0.5 1993 2.5 1992 0.6 1991 3 1990 0.7 1990 Persistence 3.5 Some additional features Integration into global financial markets is a integration into a market that is segmented by risk categories. The riskier segments behave in a clearly pro-cyclical way. Segmentation has declined due to reserve accumulation and development of domestic bond markets… … but these achievements of EMEs have become a double-edge sword, as they attract capital flows. EMEs markets are relatively small A small portfolio decision in AEs has major effects on EMEs Sprea ds Yi el ds 1-Jul-10 1-Jan-10 1-Jul-09 1-Jan-09 1-Jul-08 1-Jan-08 1-Jul-07 1-Jan-07 1-Jul-06 1-Jan-06 1-Jul-05 1-Jan-05 1-Jul-04 1-Jan-04 1-Jul-03 1-Jan-03 1-Jul-02 1-Jan-02 1-Jul-01 1-Jan-01 1-Jul-00 1-Jan-00 1-Jul-99 1-Jan-99 1-Jul-98 1-Jan-98 Riskier markets are pro-cyclical, but segmentation has declined Emerging Markets' Spreads and Yields, 1998-2010 22.0 20.0 18.0 16.0 14.0 12.0 10.0 8.0 6.0 4.0 2.0 0.0 Due to massive reserve accumulation … Foreign exchange reserves (% of GDP) 25% 50% High income, excluding Japan Japan 45% Middle-income, excluding China Low-income 20% 40% China 35% 15% 30% 25% 10% 20% 15% 5% 10% 5% 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 1983 1982 0% 1981 0% … and domestic market development in EMEs Capital markets in EMEs are small compared to AEs Domestic + International Domestic debt securities (Sept. 2010) USA 13.6% 11.1% USA Other advanced Other advanced EMEs EMEs 33.9% 37.9% 48.5% 55.0% The current surge: explanations and paradoxes The problem has not been QEs, which has been unable to increase the money supply in the US… … but the interest rate differentials, which will continue to be with us due to: Reduced risk perception regarding EMEs Two-speed world economy Two paradoxes: “Self-insurance” is good for financial stability but increases the flood of capital Domestic financial market development has the same effect Monetary base expansion in the US has led to increasing reserves deposited in the Fed US Monetary base and non-borrowed reserves (billion dollars) 3,000 2,500 2,000 1,500 1,000 500 Monetary base Non-borrowed reserves Jan-11 Sep-10 May-10 Jan-10 Sep-09 May-09 Jan-09 Sep-08 May-08 Jan-08 Sep-07 May-07 Jan-07 Sep-06 May-06 Jan-06 Sep-05 May-05 Jan-05 Sep-04 May-04 -500 Jan-04 0 The two speed world economy, which has its mirror in monetary policies 10.0% 8.0% 6.0% 4.0% 2.0% -4.0% -6.0% Developed Developing 1971-2002 2003-2012 2010 2005 2000 1995 1990 1985 1980 1975 -2.0% 1970 0.0% Major implications Stability of EMEs and free capital movements may just be inconsistent objectives. With structural imbalances in the world economy, interest rate arbitrage is a source of instability So, global (i.e., not only national) capital account regulations may be necessary to manage persistent incentives to interest-rate arbitrage. What remains of the advantages of capital mobility / liberalization? Allow countries with limited savings to attract financing for productive investment … if countries can manage to run stable current account deficits; and, in any case, most financing does not lead to investment. Foster the diversification of investment risk Certainly for source countries; for recipient countries, there are increased risks Contributes to the development of financial markets This is partly correct, so long as funds are stable Access to global capital markets is good, but capital account liberalization has unclear benefits. THE POLICY DEBATE The central policy issues (1) Medium-term cycles, not short-term volatility are the most difficult to manage. The reasons are simple: Capital flows directly generate pro-cyclical effects They also reduce the room of maneuver for countercyclical macroeconomic policies Fiscal policy can always be counter-cyclical, but: Pro-cyclical financing reduces the room of maneuver for counter-cyclical fiscal policies. Austerity during crises generates pressures to spend during the recovery, thus a pro-cyclical dynamics of a political economy character. The medium-term cycle Financial flows to LA (% of GDP) 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% -2.0% -3.0% -4.0% Inflows Net 2010 2008 2006 2004 2002 2000 1998 1996 1994 1992 1990 1988 1986 1984 1982 -1.0% 1980 0.0% The central policy issues (2) Monetary/exchange rate autonomy: with free capital movements, countries may be just choose where they want the instability of capital flows to be reflected in the domestic economy. Exchange rate flexibility has real costs: It can easily lead to overvaluation and a risky growth pattern. It increases the risk of producing tradables = it is a tax on international specialization (Kindleberger) These two issues explain the revealed preference for intermediate exchange rate regimes. But the essential instrument, heavy counter-cyclical reserve accumulation, also has costs. Exchange rate regimes: recent Latin American experience (1) Coefficient of variation of the real exhange rate, 2004-2011 0.0% Argentina Brazil Chile Colombia Guatemala Mexico Peru Uruguay Bolivia Costa Rica Dom. Rep. Honduras Nicaragua Paraguay Venezuela Ecuador El Salvador Panama 3.0% 6.0% 9.0% 12.0% 15.0% 18.0% 21.0% Exchange rate regimes: recent Latin American experience (2) Real appreciation: May 2011 vs. average 2004-11 -10.00 -5.00 0.00 Argentina Brazil Chile Colombia Guatemala Mexico Peru Uruguay Bolivia Costa Rica Dom. Rep. Honduras Nicaragua Paraguay Venezuela Ecuador El Salvador Panama 5.00 10.00 15.00 20.00 25.00 30.00 The central policy issues (3) Counter-cyclical policies require many more instruments, indeed more instruments than objectives, including an acceptable level and stability of the real exchange rate. Counter-cyclical prudential and capital account regulations are essential ingredients of such policies (macroprudential framework). Thus, they are not measures of “last resort”. They are essential ingredients of the policy package. This is particularly true of capital account regulations, as they target the major direct source of shocks. Macroprudential regulations There is a continuum between three types of regulations: Strict counter-cyclical prudential regulations (capital, provisions and/or liquidity) Foreign-exchange related prudential measures Capital-account regulations (capital management techniques, capital flow management measures) Their use should be based on certain criteria: Consistency with characteristics of financial system. Effectiveness. But this may imply that simple quantity-based regulations (prohibitions, quantitative limits) may be better, and that selective policies may be preferable. Some operate as “speed bumps” and must be dynamically strengthened. Institutional capacity: it is better to have permanent regimes that are managed in a counter-cyclical way. CAPITAL FLOWS AND MACROPRUDENTIAL REGULATION José Antonio Ocampo Columbia University