Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Fear of floating wikipedia , lookup

Economic bubble wikipedia , lookup

Modern Monetary Theory wikipedia , lookup

Nominal rigidity wikipedia , lookup

Nouriel Roubini wikipedia , lookup

Global financial system wikipedia , lookup

Business cycle wikipedia , lookup

Great Recession in Russia wikipedia , lookup

Austrian business cycle theory wikipedia , lookup

Monetary policy wikipedia , lookup

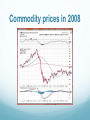

Lessons of the Great Depression and Great Recession for Current Policy Scott Sumner, Mercatus Center and Bentley University The consensus view “The worst financial crisis in the history of the United States and many other countries started in 1929. The Great Depression followed. The second-worst struck in the fall of 2008 and the Great Recession followed. Commentators have dwelt endlessly on the causes of these and other deep financial collapses. Less conspicuous has been the macroeconomists’ concern about why output and employment collapse after a financial crisis and remain at low levels for several or many years after the crisis.” (Robert Hall, JEP, 2010.) Timeline of Great Contraction August 1929: Depression Begins October 1929: Stock market crash November 1930: First (small) banking crisis Mid-1931: International exchange rate/banking crises Early 1933: Gold standard/banking crisis Mid-1929 to early 1933: NGDP falls by more than 50% Cause of Great Contraction Negative AD shock, caused by gold hoarding Gold demand rose for three reasons: 1. Private gold hoarding (devaluation fears) 2. Currency hoarding (currency had to be backed by gold) 3. Central bank gold hoarding (higher gold/currency ratios) Causal factors in the Great Depression The Relationship Between Detrended Industrial Production and Detrended (inverted) Real Wages, 1929-39, monthly. Effects of the Great Contraction NGDP is the resources available to repay individual, business and sovereign debt. A dramatic decline in NGDP growth will generally trigger a financial crisis. (E.g. Argentina 2001) The crisis will usually be misdiagnosed as a result of ”irresponsible lending” Irresponsible lending does often occur, but is generally just the tip of the iceberg. Business cycles and asset prices Two stock market crashes 1929 and 1987 stock market crashes compared The 1929 and 1987 stock market crashes were almost identical. In both cases stocks fell by about 20% in six weeks, and then by more than 20% in just one or two days. The 1929 crash was followed by the Great Depression. The 1987 crash was followed by a boom. Tight money caused financial distress Tight money (gold hoarding) caused NGDP to plummet. Because most debts are nominal, the sharp fall in NGDP led to financial distress (albeit far less than a similar crash would cause today.) Financial stress was a symptom of the Depression, but also led to gold hoarding that worsened the decline. Musical Chairs Model Falling NGDP creates two problems, financial distress and high unemployment. Both problems caused by nominal stickiness: Nominal debt contracts & nominal wage contracts. NGDP is the resources available to pay nominal debts, and nominal wages. When NGDP falls unexpectedly, there is too little nominal revenue for companies to maintain existing employment levels High unemployment. Recovery aborted by wage shocks, five times Four month (nonannualized!) growth rates for industrial production July May Nov. Nov. 1933 wage shock 1934 wage shock 1938 wage shock 1939 wage shock Before +57.4% +11.9% +15.8% +16.0% After -18.8% -15.0% +2.5% -6.5% What about the Great Recession? NGDP declined about 3%, which was about 8% below trend. The US banking system was far more fragile than in 1929 (Not entirely due to deregulation---system was also quite fragile in 1980. Moral hazard was also a problem.) Unlike with the Great Depression, financial stress began before the 2008 recession occurred. Real GDP: 2007-2010, (monthly estimates from Macroeconomics Advisors) Nominal GDP: 2007-2010 The “musical chairs model” Mishkin’s key lessons for monetary policy 1. It is dangerous always to associate the easing or the tightening of monetary policy with a fall or a rise in short-term nominal interest rates. 2. Other asset prices besides those on short-term debt instruments contain important information about the stance of monetary policy because they are important elements in various monetary policy transmission mechanisms. 3. Monetary policy can be highly effective in reviving a weak economy even if short term rates are already near zero. Real interest rates on Treasury bonds with a roughly 5 year maturity; July to November 2008 Commodity prices in 2008 The value of the dollar in late 2008 Other Asset Markets Stock prices crashed in late 2008 Commercial real estate prices started falling sharply about the same time as NGDP, and long after the subprime bubble Residential real estate prices in the heartland (Texas, etc.) had been stable during the 2006-08 subprime crash, and started falling in late 2008 along with NGDP TIPS spreads (i.e. inflation expectations) fell sharply. If you insist on using interest rates Friedman on low interest rates “Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy. . . . After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die.” (WSJ, Dec. 1997) Bernanke on monetary indicators The imperfect reliability of money growth as an indicator of monetary policy is unfortunate, because we don’t really have anything satisfactory to replace it. As emphasized by Friedman . . . nominal interest rates are not good indicators of the stance of policy . . . The real short-term interest rate . . . is also imperfect . . . Ultimately, it appears, one can check to see if an economy has a stable monetary background only by looking at macroeconomic indicators such as nominal GDP growth and inflation. The housing crash was mostly over before the unemployment rate began rising sharply. Jan. 2006: starts = 2,303,000, completions = 2,058,000, average = 2,180,000, U-rate = 4.7% April 2008: starts = 1,008,000, completions =1,014,000, average = 1,011,000, U-rate = 5.0% October 2009: starts = 527,000, completions = 745,000, average = 636,000. U-rate = 10.0% Kevin Erdmann on US real estate The US has multiple housing markets. “Closed access” (15% of population) “Contagion cities” (5% of population) Intermediate cities (Seattle, Washington DC) “Open Access” Most of the country. Fundamentals generally explain housing prices during bubble, except perhaps in the contagion areas. Housing construction was not abnormally high in 2006 Bubbles are difficult to spot . . . . . . especially in foreign countries Real housing prices Share of Treasury debt held by the Fed Why no recession in Australia? Australian growth did slow sharply after 2008, however: 1996/2 – 2006/2 Aus. NGDP growth = 6.54% 2006/2 – 2012/2 Aus. NGDP growth = 6.49% US growth slowed from 5.5% to 2.6% Eurozone growth slowed from 4% to 1.8% Two examples of fiscal austerity: The US NGDP (red line) and the Eurozone NGDP (blue line) Slow Eurozone NGDP growth depresses bond yields When the tide goes out . . . Bad loans: Subprime mortgages, Greek sovereign debt Declining NGDP growth causes crisis to spread beyond reckless borrowers. (ordinary mortgages, business loans, Spanish sovereign debt.) European double dip recession causes second European debt crisis. Think outside the box “Tell me,” the great twentieth-century philosopher Ludwig Wittgenstein once asked a friend, “why do people always say it was natural for man to assume that the sun went around the Earth rather than that the Earth was rotating?” His friend replied, “Well, obviously because it just looks as though the Sun is going around the Earth.” Wittgenstein responded, “Well, what would it have looked like if it had looked as though the Earth was rotating?” Imaginary conversation Wittgenstein: Tell me, why do people always say it’s natural to assume the Great Recession was caused by the financial crisis of 2008? Friend: Well, obviously because it looks as though the Great Recession was caused by the financial crisis of 2008. Wittgenstein: Well, what would it have looked like if it had been caused by Fed and ECB policy errors, which allowed nominal GDP to fall at the sharpest rate since 1938, especially during a time when banks were already stressed by the subprime fiasco, and when the resources for repaying nominal debts come from nominal income?