Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Securitization wikipedia , lookup

Investment fund wikipedia , lookup

Land banking wikipedia , lookup

Financialization wikipedia , lookup

Greeks (finance) wikipedia , lookup

Investment management wikipedia , lookup

Business valuation wikipedia , lookup

Continuous-repayment mortgage wikipedia , lookup

International asset recovery wikipedia , lookup

Financial economics wikipedia , lookup

Present value wikipedia , lookup

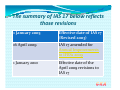

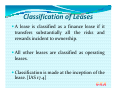

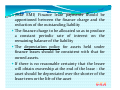

Overview of IFRS Presented by: CA. Rishi Khator FCA, CPA, CIFRS E-Mail – [email protected] Scope All leases Other than -- For minerals, oil, natural gas, and similar regenerative resources and licensing agreements for films, videos, plays, manuscripts, patents, copyrights, and similar items. [IAS 17.2] Property held by lessees that is accounted for as investment property for which the lessee uses the fair value model set out in IAS 40. Cont…. Investment property provided by lessors under operating leases (see IAS 40). Biological assets held by lessees under finance leases (see IAS 41). Biological assets provided by lessors under operating leases (see IAS 41). Definitions 1. A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time. 2. A finance lease is a lease that transfers substantially all the risks and rewards incident to ownership of an asset. 3. An operating lease is a lease other than a finance lease. 4. A non-cancellable lease is a lease that is cancellable only: (a) upon the occurrence of some remote contingency; or (b) with the permission of the lessor; or (c) if the lessee enters into a new lease for the same or an equivalent asset with the same lessor; or (d) upon payment by the lessee of an additional amount such that, at inception, continuation of the lease is reasonably certain. 4. The inception of the lease is the earlier of the date of the lease agreement and the date of a commitment by the parties to the principal provisions of the lease. 5. The lease term is the non-cancellable period for which the lessee has agreed to take on lease the asset together with any further periods for which the lessee has the option to continue the lease of the asset, with or without further payment, which option at the inception of the lease it is reasonably certain that the lessee will exercise. 6. Minimum lease payments are the payments over the lease term that the lessee is, or can be required, to make excluding contingent rent, costs for services and taxes to be paid by and reimbursed to the lessor, together with: (a) in the case of the lessee, any residual value guaranteed by or on behalf of the lessee; or (b) in the case of the lessor, any residual value guaranteed to the lessor: (i) by or on behalf of the lessee; or (ii) by an independent third party financially capable of meeting this guarantee. 7. However, if the lessee has an option to purchase the asset at a price which is expected to be sufficiently lower than the fair value at the date the option becomes exercisable that, at the inception of the lease, is reasonably certain to be exercised, the minimum lease payments comprise minimum payments payable over the lease term and the payment required to exercise this purchase option. 8. Fair value is the amount for which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm’s length transaction. 9. Economic life is either: (a) the period over which an asset is expected to be economically usable by one or more users; or (b) the number of production or similar units expected to be obtained from the asset by one or more users. 10. Useful life of a leased asset is either: (a) the period over which the leased asset is expected to be used by the lessee; or (b) the number of production or similar units expected to be obtained from the use of the asset by the lessee. 11. Residual value of a leased asset is the estimated fair value of the asset at the end of the lease term. 12. Guaranteed residual value is: (a) in the case of the lessee, that part of the residual value which is guaranteed by the lessee or by a party on behalf of the lessee (the amount of the guarantee being the maximum amount that could, in any event, become payable); and (b) in the case of the lessor, that part of the residual value which is guaranteed by or on behalf of the lessee, or by an independent third party who is financially capable of discharging the obligations under the guarantee. 13. Unguaranteed residual value of a leased asset is the amount by which the residual value of the asset exceeds its guaranteed residual value. 14. Gross investment in the lease is the aggregate of the minimum lease payments under a finance lease from the standpoint of the lessor and any unguaranteed residual value accruing to the lessor. 15. Unearned finance income is the difference between: (a) the gross investment in the lease; and (b) the present value of (i) the minimum lease payments under a finance lease (ii) any unguaranteed residual value accruing to the lessor, at the interest rate implicit in the lease. 16. Net investment in the lease is the gross investment in the lease less unearned finance income. 17. The interest rate implicit in the lease is the discount rate that, at the inception of the lease, causes the aggregate present value of (a) the minimum lease payments under a finance lease from the standpoint of the lessor; and (b) any unguaranteed residual value accruing to the lessor, to be equal to the fair value of the leased asset. 18. The lessee’s incremental borrowing rate of interest is the rate of interest the lessee would have to pay on a similar lease or, if that is not determinable, the rate that, at the inception of the lease, the lessee would incur to borrow over a similar term, and with a similar security, the funds necessary to purchase the asset. 19. Contingent rent is that portion of the lease payments that is not fixed in amount but is based on a factor other than just the passage of time (e.g., percentage of sales, amount of usage, price indices, market rates of interest). Service Concession Arrangements Defined (IFRIC-12) 1. An arrangement whereby a government or other public sector body contracts with a private operator to develop (or upgrade), operate and maintain 2. Grantor's infrastructure assets such as roads, bridges, tunnels, airports, energy distribution networks, prisons or hospitals. 3. The grantor controls or regulates what services the operator must provide using the assets, to whom, and at what price, and also controls any significant residual interest in the assets at the end of the term of the arrangement. Objective of IFRIC 12 • How certain aspects of existing IASB literature are to be applied to service concession arrangements. Types of Service Concession Arrangements • IFRIC 12 draws a distinction between two types of service concession arrangement. Type 1 1. Operator receives a financial asset, 2. An unconditional contractual right to receive a specified or determinable amount of cash or another financial asset from the government in return 3. For constructing or upgrading a public sector asset, and then operating and maintaining the asset for a specified period of time. 4. Includes guarantees by the government to pay for any shortfall between amounts received from users of the public service and specified or determinable amounts. Type 2 1. Operator receives an intangible asset 2. A right to charge for use of a public sector asset 3. It constructs or upgrades and then must operate and maintain for a specified period of time. 4. A right to charge users is not an unconditional right to receive cash because the amounts are contingent on the extent to which the public uses the service. General 1. IFRIC 12 allows for the possibility that both types of arrangement may exist within a single contract: 2. To the extent that the government has given an unconditional guarantee of payment for the construction of the public sector asset, The operator has a financial asset; 3. To the extent that the operator has to rely on the public using the service in order to obtain payment, the operator has an intangible asset. Accounting – Financial asset model 1. The operator recognises a financial asset to the extent that it has an unconditional contractual right to receive cash or another financial asset from or at the direction of the grantor for the construction services. 2. The operator has an unconditional right to receive cash if the grantor contractually guarantees to pay the operator (a) specified or determinable amounts or (b) the shortfall, if any, between amounts received from users of the public service and specified or determinable amounts, even if payment is contingent on the operator ensuring that the infrastructure meets specified quality or efficiency requirements. 3. The operator measures the financial asset at fair value. Accounting – Intangible asset model 1. The operator recognises an intangible asset to the extent that it receives a right (a licence) to charge users of the public service. 2. A right to charge users of the public service is not an unconditional right to receive cash because the amounts are contingent on the extent that the public uses the service. 3. The operator measures the intangible asset at fair value. Accounting Operating revenue • The operator of a service concession arrangement recognises and measures revenue in accordance with IASs 11 and 18 for the services it performs. Accounting by the Government (Grantor) 1. IFRIC 12 does not address accounting for the government side of service concession arrangements. 2. However, the International Public Sector Accounting Standards Board (IPSASB) has started its own project on service concession arrangements, which will give serious consideration to accounting by grantors. 3. The principles applied in IFRIC 12 will be considered as part of the project. Effective Date IFRIC 12 is effective for annual periods beginning on or after 1 January 2008. Earlier application is permitted. LEASES (IAS-17) October 1980 Exposure Draft E19 Accounting for Leases September 1982 IAS 17 Accounting for Leases 1 January 1984 Effective Date of IAS 17 (1982) 1994 IAS 17 (1982) was reformatted April 1997 Exposure Draft E56, Leases December 1997 IAS 17 Leases 1 January 1999 18 December 2003 Effective Date of IAS 17 (1997), Leases Revised version of IAS 17 issued by the IASB The summary of IAS 17 below reflects those revisions 1 January 2005 Effective date of IAS 17 (Revised 2003) 16 April 2009 IAS 17 amended for Annual Improvements to IFRSs 2009 1 January 2010 Effective date of the April 2009 revisions to IAS 17 RELATED INTERPRETATIONS IFRIC 4 Determining arrangement contain lease whether an IFRIC 12 Service Concession Arrangements SIC 15 Operating Leases - Incentives SIC 27 Evaluating the Substance of Transactions in the Legal Form of a Lease SUMMARY OF IAS 17 Objective of IAS 17 Prescribe, for lessees and lessors, in respect of finance and operating leases. Appropriate accounting policies Disclosures Classification of Leases A lease is classified as a finance lease if it transfers substantially all the risks and rewards incident to ownership. All other leases are classified as operating leases. Classification is made at the inception of the lease. [IAS 17.4] Situations that would normally lead to a lease being classified as a finance lease include the following: [IAS 17.10] the lease transfers ownership of the asset to the lessee by the end of the lease term; the lessee has the option to purchase the asset at a price which is expected to be sufficiently lower than fair value at the date the option becomes exercisable and at the inception of the lease, it is reasonably certain that the option will be exercised; the lease term is for the major part of the economic life of the asset, even if title is not transferred; at the inception of the lease, the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset; and the lease assets are of a specialised nature such that only the lessee can use them without major modifications being made. If the lessee is entitled to cancel the lease, the lessor's losses associated with the cancellation are borne by the lessee; gains or losses from fluctuations in the fair value of the residual fall to the lessee (for example, by means of a rebate of lease payments); and the lessee has the ability to continue to lease for a secondary period at a rent that is substantially lower than market rent. Land and Building Elements would normally be considered separately. The minimum lease payments are allocated between the land and buildings elements in proportion to their relative fair values. The land element is normally classified as an operating lease unless title passes to the lessee at the end of the lease term. The buildings element is classified as an operating or finance lease by applying the classification above in IAS 17. [IAS 17.15] However, separate measurement of the land and buildings elements is not required if the lessee's interest in both land and buildings is classified as an investment property and the fair value model is adopted. Accounting by Lessees The following principles should be applied in the financial statements of lessees: Finance Lease At commencement of the lease term should be recorded as an asset and a liability at the lower of the fair value of the asset and the present value of the minimum lease payments Discounted at the interest rate implicit in the lease, if practicable, or else at the enterprise's incremental borrowing rate (Like EMI) Finance lease payments should be apportioned between the finance charge and the reduction of the outstanding liability The finance charge to be allocated so as to produce a constant periodic rate of interest on the remaining balance of the liability The depreciation policy for assets held under finance leases should be consistent with that for owned assets. If there is no reasonable certainty that the lessee will obtain ownership at the end of the lease - the asset should be depreciated over the shorter of the lease term or the life of the asset Operating Lease Lease payments recognised as an expense in the income statement over the lease term On a straight-line basis, unless another systematic basis is more representative of the time pattern of the user's benefit. Incentives – SIC 15 (July 1999) For operating Lease Incentives (e.g. rent free period or contribution to relocation cost) for the agreement of a new or renewed Be recognised by the lessee as a reduction of the rental expense over the lease term, Accounting by Lessors The following principles should be applied in the financial statements of lessors: Finance Lease At commencement record a finance lease in the balance sheet as a receivable, At an amount equal to the net investment in the lease; [IAS 17.36] Recognise finance income based on a pattern reflecting a constant periodic rate of return on the lessor's net investment outstanding in respect of the finance lease; Operating Lease Assets held be presented in the balance sheet of the lessor according to the nature of the asset. Lease income should be recognised over the lease term on a straight-line basis, unless another systematic basis is more representative Incentives – SIC 15 (July 1999) For operating Lease Incentives for the agreement of a new or renewed Recognised as a reduction of the rental income over the lease term Manufacturers or dealer lessors Include selling profit or loss in the same period as they would for an outright sale. Artificially low rates of interest are charged, selling profit should be restricted to that which would apply if a commercial rate of interest were charged. [IAS 17.42] Initial Direct Cost Incurred by lessors in negotiating leases must be recognised over the lease term. They may no longer be charged to expense when incurred. This treatment does not apply to manufacturer or dealer lessors where such cost recognition is as an expense when the selling profit is recognised. QUESTIONS AND ANSWERS FROM 1-5 Sale and Leaseback Transactions Finance Lease For a sale and leaseback transaction that results in a finance lease, any excess of proceeds over the carrying amount is deferred and amortised over the lease term. Operating lease At fair value - the profit or loss should recognised immediately; Sale price < fair value - profit or loss should be recognised immediately, except if a loss is compensated for by future rentals at below market price, Sale price > fair value - the excess over fair value should be deferred and amortised over the period of use; and Fair value < Carrying amount - a loss equal to the difference should be recognised immediately E.g. FV – Rs.100, CA – Rs.90, SP Rs.110 Please refer Case Study – 1 Disclosure: Lessees - Finance Lease [IAS 17.31] Carrying amount of asset; Reconciliation between total minimum lease payments and their present value; Amounts of minimum lease payments at balance sheet date and the present value thereof, for: the next year; years 2 through 5 combined; beyond five years; Contingent rent recognised as an expense; total future minimum sublease income under noncancellable subleases; and general description of significant leasing arrangements, including contingent rent provisions, renewal or purchase options, and restrictions imposed on dividends, borrowings, or further leasing. Disclosure: Lessees - Operating Lease [IAS 17.35] amounts of minimum lease payments at balance sheet date under noncancellable operating leases for: the next year; years 2 through 5 combined; beyond five years; total future minimum sublease income under noncancellable subleases; lease and sublease payments recognised in income for the period; contingent rent recognised as an expense; and general description of significant leasing arrangements, including contingent rent provisions, renewal or purchase options, and restrictions imposed on dividends, borrowings, or further leasing Disclosure: Lessors - Finance Lease [IAS 17.47] reconciliation between gross investment in the lease and the present value of minimum lease payments; gross investment and present value of minimum lease payments receivable for: the next year; years 2 through 5 combined; beyond five years; unearned finance income; unguaranteed residual values; accumulated allowance for uncollectible lease payments receivable; contingent rent recognised in income; and general description of significant leasing arrangements. Disclosure: Lessors - Operating Lease [IAS 17.56] amounts of minimum lease payments at balance sheet date under noncancellable operating leases in the aggregate and for: the next year; years 2 through 5 combined; beyond five years; contingent rent recognised as in income; and general description of significant leasing arrangements. IFRIC-4 An entity can enter into an arrangement, comprising a transaction or a series of related transactions that does not take the legal form of a lease but conveys a right to use an asset in return for a payment or series of payments. Examples of arrangements in which one entity (the supplier) may convey such a right to use an asset to another entity (the purchaser), often together with related services, include: Cont. outsourcing arrangements arrangements in the telecommunications industry, in which suppliers of network capacity enter into contracts to provide purchasers with right to capacity take-or-pay and similar contracts, in which purchasers must make specified payments regardless of whether they take delivery of the contracted products or services. Scope Of IFRIC 4 This interpretation does not apply to arrangements that are: or contain, leases excluded from the scope of IAS 17 (AC 105) Leases public-to-private service concession arrangements within the scope of IFRIC 12 (AC 445) Service Concession Arrangements. Issues How to determine whether an arrangement is, or contains, a lease as defined in IAS 17 (AC 105) Leases When the assessment or a reassessment of whether an arrangement is, or contains, a lease should be made If an arrangement is, or contains, a lease, how the payments for the lease should be separated from payments for any other elements in the arrangement. SIC-27 SIC 27 addresses issues that may arise when an arrangement between an enterprise and an investor involves the legal form of a lease. Accounting for arrangements between an enterprise and an investor should reflect the substance of the arrangement. All aspects of the arrangement should be evaluated to determine its substance, ISSUES ARE A SERIES OF TRANSACTIONS LINKED? ISTHE ARRANGEMENT IN SUBSTANCE A LEASE UNDER IAS 17 (AC 105)? WHERE ARRANGEMENT IN SUBSTANCE NOT A LEASE: _ do separate investment account and lease payment obligations that might exist represent assets and liabilities of the entity? _ how does the entity account for other obligations resulting from the arrangement? _ how does the entity account for a fee it might receive from an investor. Classification of leases of land Latest Development Prior to amendment, IAS 17 Leases generally required a lease of land with an indefinite useful life to be classified as an operating lease. This was inconsistent with the general principles of the Standard, Following the amendment, leases of land are classified as either ‘finance’ or ‘operating’ using the general principles of IAS 17. The amendment is particularly significant for jurisdictions where property rights are obtained under long-term leases and the substance of those leases differs little from buying a property. Entities will need to reassess existing leases. Effective Jan.1, 2010