Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Capital control wikipedia , lookup

Bretton Woods system wikipedia , lookup

Foreign exchange market wikipedia , lookup

Nouriel Roubini wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Fixed exchange-rate system wikipedia , lookup

Exchange rate wikipedia , lookup

Business Cycles in the Open Economy

Mundell‐Fleming with Fixed Exchange Rates

Andrew Rose, Global Macroeconomics 10

1

Three Important Assumptions

Three Important Assumptions

• Prices are Sticky

Prices are Sticky

– Business Cycle Model, Short Run

• Capital

Capital is Internationally Mobile

is Internationally Mobile – No No

Substantial Barriers to Private Capital Flows

– Rich countries, some emerging markets (but only Ri h

i

i

k (b

l

recently)

• Nominal Exchange Rates fixed

N i lE h

R

fi d by Central Bank

b C

lB k

– Some economies, though more have fixed in past

Andrew Rose, Global Macroeconomics 10

2

Add Net Exports to Real Economy (IS)

Add Net Exports to Real Economy (IS)

• Recall that net exports (NX≡X‐M; current account) Recall that net exports (NX≡X M; current account)

determined by:

1. Domestic output Y, raises imports (M)

2 Foreign output Y* (assumed to be exogenous, since 2.

Foreign output Y* (assumed to be exogenous since

foreign), raises exports (X)

3. Real exchange rate (eP/P*), “competitiveness” affects both X and M

Andrew Rose, Global Macroeconomics 10

3

Add Net Exports to Real Economy (IS)

Add Net Exports to Real Economy (IS)

• Thus

Thus IS now: Y IS now: Y = A(G,i,Y) + NX(,Y,Y

A(G,i,Y) + NX(,Y,Y*))

– A is domestic absorption

Andrew Rose, Global Macroeconomics 10

4

Financial Equilibrium (LM):

What is a Fixed Exchange Rate?

h

d

h

?

• Nominal

N i l exchange rate fixed, so real exchange h

t fi d

l

h

rate (=eP/P*)

(

/ ) fixed in short run

• Fixed Exchange Rate Regime authorities take either side of FX transaction in unlimited quantity

Andrew Rose, Global Macroeconomics 10

5

Fixed Exchange Rate Regime

Fixed Exchange Rate Regime

• The

Th “Authorities”: Government

“A th iti ” G

t chooses

h

t fi

to fix exchange rate (or not); Central Bank enacts policy

– Fix: Authorities promise to use international reserves to take either side of any FX transaction in any size at k

h

d f

fixed exchange rate (or within bands)

– Hence fix may affect IR, HPM, thus money supply

Andrew Rose, Global Macroeconomics 10

6

Financial Equilibrium

Financial Equilibrium

• LM looks same but not under complete control of Central Bank

– Recall M=μ*HPM; HPM=(IR+CBC); IR used to fix exchange rate

Andrew Rose, Global Macroeconomics 10

7

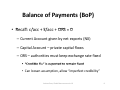

Balance of Payments (BoP)

Balance of Payments (BoP)

• Recall: c/acc + k/acc + ORS = 0

R ll /

k/

ORS 0

– Current Account given by net exports (NX)

Current Account given by net exports (NX)

– Capital Account – private capital flows

– ORS – authorities must keep exchange rate fixed

• “Credible Fix” is expected to remain fixed

“Credible Fi ” is e pected to remain fi ed

• Can loosen assumption, allow “imperfect credibility”

Andrew Rose, Global Macroeconomics 10

8

Capital Mobility 1

Capital Mobility 1

• Assume capital can flow freely without (serious) ssu e cap ta ca o

ee y t out (se ous)

restrictions between the small open (home) economy and large (“center” or “anchor”) neighbor(US/EMU)

hb ( /

)

• Assume domestic & foreign bonds “perfect substitutes,” identical in liquidity, maturity, taxes, b tit t ” id ti l i li idit

t it t

risk…

– Can also easily add country risk premium

Can also easily add country risk premium

• Also assume nominal exchange rate is fixed and p

yf

(

)

expected to stay fixed (“credible fix”)

Andrew Rose, Global Macroeconomics 10

9

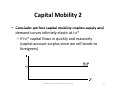

Capital Mobility 2

Capital Mobility 2

• Conclude:

Conclude: perfect capital mobility implies supply and perfect capital mobility implies supply and

demand curves infinitely elastic at i=i*

– If i>i* capital flows in quickly and massively p

q

y

y

(capital account surplus since we sell bonds to foreigners)

Andrew Rose, Global Macroeconomics 10

10

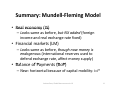

Summary: Mundell‐Fleming

Summary: Mundell

Fleming Model

Model

• Real economy (IS)

Real economy (IS)

– Looks same as before, but NX added (foreign income and real exchange rate fixed)

• Financial markets (LM)

– Looks same as before, though now money is endogenous (international reserves used to defend exchange rate, affect money supply) • Balance of Payments (BoP)

B l

fP

(B P)

– New: horizontal because of capital mobility: i=i*

Andrew Rose, Global Macroeconomics 10

11

Formally

• IS: Y = A(G,i,Y) + NX(,Y,Y*) IS Y A(G i Y) + NX( YY*)

where A= {1/(1 ‐ c(1‐t))}*[C0 + cTr + I0 – bi + G0],

and ,Y* exogenous

• LM: Ms/P = L(i, Y)

where M

where

Ms = HPM = (IR + CBC)

= HPM = (IR + CBC)

• BoP: c/acc + k/acc + ORS = 0

Andrew Rose, Global Macroeconomics 10

12

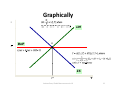

Graphically

i

LM

i*

BoP

A

IS

Y*

Andrew Rose, Global Macroeconomics 10

Y

13

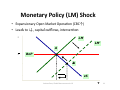

Monetary Policy (LM) Shock

Monetary Policy (LM) Shock

• Expansionary Open Market Opera on (CBC↑)

• Leads to i↓, capital ou

d

↓

l

llows, interven on

i

LM

LM'

A

i*

BoP

B

IS

Andrew Rose, Global Macroeconomics 10

Y

14

Enduring Effect

Enduring Effect

• Note that central bank can only change N t th t

t lb k

l h

composition

p

of high‐powered money since it g p

y

defends fixed exchange rate (IR↓) to offset capital outflow (HPM and Ms unchanged)

Andrew Rose, Global Macroeconomics 10

15

Key Concept: Mundell’s Incompatible/Holy Trinity

bl / l

• The

The following are individually desirable but following are individually desirable but

mutually incompatible:

1 Independent

1.

Independent national monetary policy national monetary policy

(“Monetary Sovereignty”)

2 Perfect capital mobility

2.

Perfect capital mobility

3. Fixed/stable exchange rates

• Different

Different countries make different countries make different “sacrifices”

sacrifices and choices also change over time

Andrew Rose, Global Macroeconomics 10

16

Fiscal Policy

Fiscal Policy

•

G↑ (debt‐financed) leads to capital inflows, IR↑, HPM↑, Ms↑ and Y↑

IS'

i

B

LM

IS

LM'

A

i*

BoP

C

Y

Andrew Rose, Global Macroeconomics 10

17

Enduring Effect

Enduring Effect

• Highly potent (no “crowding out” since Hi hl

t t( “

di

t” i

interest rates given from abroad)

g

)

• Changes composi on of output (G↑, NX↓)

– Can explain “twin deficits” of government, c/acc

Andrew Rose, Global Macroeconomics 10

18

Foreign (Interest Rate) Shock

Foreign (Interest Rate) Shock

• Foreign (large country) interest rate rise (i

Foreign (large country) interest rate rise (i*↑)

↑)

– BoP schedule shifts up

LM’

LM

LM

B

A

IS

Andrew Rose, Global Macroeconomics 10

19

Foreign Shocks, Continued

Foreign Shocks, Continued

• Role in crises/regime switch

Role in crises/regime switch

– Mexico 1994, EMS 1992

– Decline in Northern rates 2001, 2007

Decline in Northern rates 2001, 2007‐8

8

• Sterilization of reserve flows: offsetting change in international reserves with equal and opposite

international reserves with equal and opposite change in central bank credit

– As

As IR falls, CBC rises 1:1

IR falls, CBC rises 1:1

– HPM unchanged

– Only possible temporarily

yp

p

y

Andrew Rose, Global Macroeconomics 10

20

Notes

• Can

Can generalize (im

generalize (im‐)) potency of potency of

monetary/fiscal shocks to all financial/real shocks

• Can allow for imperfect capital mobility with upwards sloping BoP (must raise interest rates upwards sloping BoP

(must raise interest rates

above foreign to attract inflows)

– One way to model a “large” country

O

t

d l “l

”

t

Andrew Rose, Global Macroeconomics 10

21

Key Takeaways

Key Takeaways

• Credible

Credible fixes constrain monetary policy

fixes constrain monetary policy

• Real shocks have large effects during fixes

• Mundell’s

d ll’ Trilemma: tradeoffs between open il

d ff b

capital markets, stable exchange rates, and monetary sovereignty

i

Andrew Rose, Global Macroeconomics 10

22