Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

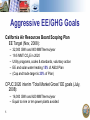

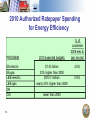

California Policy Perspectives on Efficiency and Climate Session: Taking Energy Efficiency to the Next Level New England Restructuring Roundtable Boston, MA October 30, 2009 Jeanne Clinton Climate Strategies Branch Manager California Public Utilities Commission [email protected] or (415) 703-1159 Per Capita Electricity Sales (not including self-generation) (kWh/person) 14,000 California w/out stds and programs 12,000 United States 8,000 6,000 California 4,000 2,000 2 2002 2000 1998 1996 1994 1992 1990 1988 1986 1984 1982 1980 1978 1976 1974 1972 1970 1968 1966 1964 1962 0 1960 kWh/person 10,000 2 CPUC EE Goals Through 2020 Goals set for CPUC-regulated utilities from 2004 through 2020, in accordance with best available data on energy efficiency potential. 35,000 30,000 25,000 20,000 15,000 10,000 5,000 0 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 • • 3 Does not take into account potential within Publicly-Owned Utility Service Areas Based primarily on existing technologies and rates of adoption California Targets for GHG Reduction From CARB Scoping Plan, Table 2 Recommended Reduction Measures Reductions Counted Towards 2020 Target Percentage of (MMTCO2E) 2020 Target REDUCTIONS FROM CAP AND TRADE PROGRAM 34.4 19.8% REDUCTIONS FROM COMPLEMENTARY MEASURES 112.3 64.5% California Light-Duty Vehicle Greenhouse Gas Standards 31.7 18.2% 15 8.6% 5 2.9% Vehicle Efficiency Measures 4.5 2.6% Goods Movement (Electrification at Ports, Efficiency) 3.7 2.1% Medium/Heavy Duty Vehicles (Aerodynamics, Hybridization) 1.4 0.8% 1 0.6% Low Carbon Fuel Standard Regional Transportation-Related GHG Targets* High Speed Rail Transportation Sector sub-total Energy Efficiency (Building/appliance standards, new programs, CHP, Solar Water Heating) Renewable Portfolio Standard (33% by 2010) 35.8% 26.3 15.1% 21.3 12.2% Million Solar Roofs 2.1 1.2% Industrial Measures (sources under cap-and-trade program) 0.3 0.2% Electric and Gas sub-sectors REDUCTIONS FROM UNCAPPED SOURCES/SECTORS High Global Warming Potential Gas Measures 28.7% 27.3 Sustainable Forests Industrial Measures (sources not covered under cap and trade; Oil and Gas, Transmission) 4 Recycling and Waste (landfill methane capture) TOTAL REDUCTIONS COUNTED TOWARDS 2020 TARGET 174 20.2 15.7% 11.6% 5 2.9% 1.1 0.6% 1 0.6% Aggressive EE/GHG Goals California Air Resources Board Scoping Plan EE Target (Nov, 2008): – – – – – 32,000 GWh and 800 MMTherms/year 19.5 MMT CO2E in 2020 Utility programs, codes & standards, voluntary action EE and solar water heating 15% of AB32 Plan (Cap and trade target is 20% of Plan) CPUC 2020 interim “Total Market Gross” EE goals (July, 2008): – 16,000 GWh and 620 MMTherms/year – Equal to nine or ten power plants avoided 5 The California Long Term Energy Efficiency Strategic Plan www.CaliforniaEnergyEfficiency.com Identifying Strategies to Fill in the “White Space” 45,000 Economic 40,000 Cumulative GWh Savings 35,000 Huffman Bill 30,000 BBEES 25,000 savings eligible to be partially claimed by IOUs T24+Fed Standards Current Goals (gross equivalent) 20,000 15,000 IOU Programs 10,000 Current Goals (net) 5,000 naturally-occurring 0 2008 7 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2010-12 IOU EE Portfolio Highlights • 12 Uniform Statewide Programs (by sector and segment) • Cal SPREE (Statewide Program for Residential Energy Efficiency): 20 percent savings for up to 130,000 homes • Commercial: Benchmarking all facilities touched by programs • Industrial: Continuous Energy Improvement • Zero Net Energy New Construction: $175 million launch • HVAC: Focus on state code compliance • Lighting: Phases down $ for basic Compact Fluorescent Lamps (CFLs); shifts emphasis to advanced lighting • Communities: $260 million for 64 local governments for own facilities and/or innovative approaches • Statewide Marketing, Education & Outreach: coordinated brand and implementation across 4 utilities 8 Definitional Challenges for Inter-Agency Collaboration – CAISO, CARB, CEC, CPUC • Baselines, electric & gas load forecasts, moving target of generation fuel mix/GHG profiles • Defining “additional” • Defining EE “embedded” in energy forecasts, versus a DSM “resource” • Modeling and assumptions for future resource quantitative potential, costs to acquire EE • Assigning payments; e.g. electric infrastructure, tariffs, subsidies for EVs to replace gasoline 9 Climate/EE Policy Issues Ahead for California and the U.S. • Demand-side strategies not part of Cap and Trade; no mechanism to sell GHG benefits from DSM. – Cap and trade places limits on sources of GHGs; demand-side strategies not directly integrated. – GHG emission price will make more DSM “cost-effective” – But “offsets” typically allowed outside the cap jurisdiction only • • • 10 Local Governments can influence building and transportation, but how pay for increased governance? Allowance auctions may provide EE funds to expand programs &/or creative allowance “retirement” EE Institutional challenge: Need broad vision, strong leadership, over sustained period – to overcome ”friction” of diffuse markets and action venues DSM Financing – Needs Focus, Attractive Terms, Exponential Growth California needs $8 - $25 billion in financing for EE hardware installation 2010 -2020 • Statewide Utility On-bill financing (OBF): – – • For commercial and institutional customers, w/ common caps and terms Initial $41.5 million new funds for OBF loan pool Municipal property-based financing (or “Property-Assessed Clean Energy Bonds “– PACE) – – • •11 The “salvation” for residential and rented/leased properties? California links to stimulus funded retrofit programs CPUC/State Treasurer’s office exploring collaboration to fund EE for state facilities Broader financing solutions report due 2010 Extra Slides 2008 Spending for Select Public Purpose RatepayerSupported DSM-type Activities (programs in $000s) PROGRAM TOTAL 2008 EE-electric EE-gas LIEE-electric LIEE-gas DR CSI NEM SGIP-electric SGIP-gas Low Emission Vehicles PIER RD&D RPS SUM TOTAL OF ALL PUBLIC PURPOSE SPENDING $ $ $ $ $ $ $ $ $ $ $ $ $ 622,133 136,537 91,214 66,788 141,640 323,098 76,444 14,744 67,637 87,937 112,771 1,740,943 IOU electric revenue requirement ($ millions) IOU sales revenue requirement ($ millions) IOU Combined electric and gas revenue requirement (millions) IOU service area estimated population (Millions) $ $ $ 26,328 10,166 36,494 27.2 % elec OR gas rev reqt 2.4% 1.3% 0.3% 0.7% 0.5% 1.2% 0.3% 0.1% 0.4% % of combined elec & gas rev reqt 2.08% $ $ 0.43% $ $ $ $ $ 0.25% $ $ 0.19% $ 0.24% $ $ 4.77% $ 2008 Data from Regulated California Electric and Gas Utility Ratepayer Costs, CPUC Report, February 2009 13 Per capita 22.87 5.02 3.35 2.46 5.21 11.88 2.81 0.54 2.49 3.23 4.15 64.01 2010 Authorized Ratepayer Spending for Energy Efficiency PROGRAM 2010 expected budgets EE-electric EE-gas LIEE-electric LIEE-gas DR CSI $1.03 billion 33% higher than 2008 $310.7 million nearly 50% higher than 2008 14 lower than 2008 % of combined 2008 elec & gas rev reqt 2.8% 0.9% CA’s 2010-2012 Investor-Owned Utility EE Portfolio Metrics • Savings Impacts Anticipated: – – – – • • • • • 15 6,965 GWH (3rd yr cum) 1,537 MW 150.3 MM Therms 3.07 million tons of CO2e emissions avoided (3rd yr cum) Equivalent of 3 large power plants $3.1 billion cost-effective efficiency portfolios $ 41 per capita per year (combined gas and electric) Supports 15,000 - 18,000 new jobs Performance metrics to track market transformation and programmatic progress, beyond energy savings EE Market-Place Challenges • Market strategies need to extend beyond utility programs, leverage private resources, capture economic value • Promote the business potential, capital investment opportunities • Mobilize bold action and create a "movement" for EE and other demand-side actions, behavior, investment: – Achieve deeper action – 20%, 40 %, 70% efficiency gains – Pull consumer and business demand; call on comparative benchmarks – Marketing to reflect understanding of market segments, motivations,... • Expand knowledgeable and trained providers who can successfully sell and deliver results • Innovate effective financing mechanisms – long amortization terms and transferable to successive owners/occupants (OBF, PACE, ...) 16