Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Syndicated loan wikipedia , lookup

Moral hazard wikipedia , lookup

Financial economics wikipedia , lookup

Financial literacy wikipedia , lookup

Interest rate ceiling wikipedia , lookup

Public finance wikipedia , lookup

Shadow banking system wikipedia , lookup

Global financial system wikipedia , lookup

Interbank lending market wikipedia , lookup

Financial Crisis Inquiry Commission wikipedia , lookup

Systemic risk wikipedia , lookup

Systemically important financial institution wikipedia , lookup

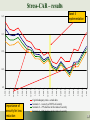

Methods and tools of macroprudential analysis the central bank’s perspective Piotr Szpunar 1 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 2 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 3 What is financial stability? Definition used by the NBP: • „…a situation when the system performs all its functions in a continuous and effective way, even when unexpected and adverse disturbances occur on a significant scale” Financial Stability Report, page 3. Lack of Financial Stability Disturbance in the provision of financial intermediation services Negative impact on the real sector 4 Why should one look after financial stability? • Financial stability is A PUBLIC GOOD • Financial system prone to market failures • Financial system as a transmitter of monetary policy of the central bank • Stable financial system as a necessary condition for smooth functioning of the payment system • Significant public costs of a financial crisis that results from a severe system instability 5 What do we look at? • Financial systems – Institutions (not only banks) – Markets – Infrastructure P(X) • Tail events – Low probability – High impact X • Ideally – forward-looking financial stability analysis: identify today the risks that can materialize in the future and suggest policy countermeasures when necessary • Necessary to coordinate with macroeconomic analysis 6 Financial system in the economy Real sector shocks Savings/Investment intermediation through e.g. investment funds; market interest rates Households and enterprises Lending, deposits insurance: Economic function Consumption smoothing, Savings/ Investment intermediation Domestic financial markets Financial market trading Financial institutions: banks, insurers, asset managers Infrastructure: systems, regulations… Foreign financial market shocks 7 A „universe” of financial stability analysis Infrastructure Macroeconomic shocks Investment funds Current situation of the banking sector Other financial institutions Insurers Assessment of potential loss & ability to withstand shocks Pension funds 8 Financial Stability in transition economies • Short history of the system in its current form – Short time-series and breaks: difficult to build models – Some financial products newly introduced • Bank-dominated financial sector main focus on banks • High share of foreign capital in the banking sector • Important non-bank institutions: – Insurance companies – Pension funds and investment funds (with investment risk borne by clients) • Important markets – FX – Treasury bonds – Equity market (but directly not important for banks due to small scale of investment in equities) 9 9 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 10 Macroprudential policy • In general terms, the ultimate goal of macroprudential policy should be safeguarding financial stability • At the operational level, the main objectives of macroprudential oversight should be prevention and mitigation of systemic risk • Prevention of risks: – (1) analysis of the financial system – (2) early identification of risks – (3) remedial action • The risk mitigation may be interpreted as making financial system more robust and resilient. 11 Who should be in charge of macroprudential analysis? • Macroprudential versus Microprudential approach Mitigating systemic risks and preventing financial crises Micro-prudential approach Macro-prudential approach (individual institution’s risks) (systemic risk) Supervision authority Central Bank 12 12 Who should be in charge of macroprudential analysis? • Key role of central banks due to: – Independence – Analytical capacity for systemic risk analysis – Data sources – not only on financial firms but also on the real economy – providing broader view – Monetary policy – Market intelligence • CB being a market participant – Close cooperation with banks – Bank of banks – lender of last resort 13 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 14 How to analyze financial stability? National Bank of Poland’s approach Slowdown in EMU Fall in prices real estate market Large portfolio of household credits from the period of lenient lending policy Crisis contagion into EM High share of FX loans Strict monetary policy due to high inflation Higher share of funding via market Credit losses Worsening standing of parent entities Higher share of foreign and parent entities funding Higher funding costs High divident payments Higher cost and volatility of deposits Lower interest income Limited capital resources Capital adequacy Profits Implications For the real economy Lending 15 Banking sector – what to look at? Financial market shocks Macroeconomic shocks and imbalances Shocks Vulnerabilities Current situation of banks Channels of impact Assessment of potential loss & ability to withstand shocks Banks’ income, capital, funding Lending and other functions of the financial system Real Economy Impact on welfare of society 16 Banking sector – what to look at? Shocks Vulnerabilities Channels of impact Banks’ income, capital, funding Lending and other functions of the financial system Real Economy Strengths and high-risk areas in the financial system Examples: - Lending policy and loan portfolio structure - Capital position - Exposures to market risk - Asset prices: real estate, shares… - Common exposures (macro vs micro perspective) - Funding structure Tools: indicators of financial system „health”, e.g. IMF’s Financial Soundness Indicators as a starting point (only!) 17 Banking sector – what to look at? Shocks Vulnerabilities Channels of impact Banks’ income, capital, funding Lending and other functions of the financial system Real Economy Potential shocks to financial stability Examples: - Macroeconomic imbalances – e.g. inflation, current account deficit, fiscal deficit – which may lead to weaker future economic growth - Indebtedness of real economy - Materialisation of risk factors for industries with significant bank debt - Tensions in financial markets - Commodity prices Tools: macroeconomic analysis 18 Banking sector – what to look at? Shocks Shock impact, transmission and amplification Vulnerabilities Channels of impact Banks’ income, capital, funding Lending and other functions of the financial system Real Economy - Which institutions are influenced? - What are the consequences of shocks? - What mechanisms can exacerbate the impact of shocks ? (e.g. liquidity squeeze on money markets can also worsen the situation of borrowers with floating-rate debt) - What are interlinkages with other financial institutions? 19 Banking sector – what to look at? Shocks Impact on banks’ financial position Vulnerabilities - Can institutions withstand the shocks? - What is their capital, liquidity and profit position after the shock? Channels of impact Banks’ income, capital, funding Tools: stress tests Lending and other functions of the financial system Real Economy 20 Banking sector – what to look at? Shocks Banks’ capacity to lend and risk appetite Vulnerabilities Channels of impact Banks’ income, capital, funding Lending and other functions of the financial system Real Economy - Would banks change their lending policy as a result of shocks? - Does their capital and funding position allow to continue to provide lending? Tools: Most often expert assessments. Macroeconomic models with detailed financial sector modules are not common yet. 21 Banking sector – what to look at? Shocks Impact on consumption, investment, unemployment, economic growth… Vulnerabilities Channels of impact Banks’ income, capital, funding Tools: expert assessments in cooperation with macroeconomic analysts; e.g. residual adjustments in macro forecasting models Lending and other functions of the financial system Real Economy 22 Indicators of financial system health • Backward-looking - based on accounting data • Distributions matter – Aggregate data useful but loss of some information – Sector-wide trends or individual bank events – But do not replicate off-site examination • What is behind the numbers – – – – Quantitative benchmarks usually not very useful Try to understand the economic process Look at a number of indicators simultaneously Qualitative information also important 23 Products of financial stability analysis • Financial Stability Reports – Main assessment of financial stability – Published every six months – Detailed analysis, including stress tests – Discussed and accepted by NBP Management Board – Main recipients • • • • NBP Management Board Monetary Policy Council FSA Interested public • Senior Loan Officer Survey • Ad-hoc work 24 FSR structure • Summary assessment of risk • Economic environment of financial institutions – Macroeconomic trends – Financial market developments – Real estate market trends • Banking sector – – – – – – Earnings Credit risk, including analysis of borrowers’ financial position Market risk Liquidity risk, including box on payment system developments Capital and stress tests Market assessment • Non-bank financial institutions 25 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 26 What is a stress test (in general)? • „A rough estimate of how the value of a portfolio changes when there are large changes to some of its risk factors”* • Now a standard tool in risk management in financial institutions… althought the current crisis shows that it was probably not used enough * source: „Financial Sector Assessment, A Handbook”, IMF & World Bank, 2005 27 What is a macro stress test? • An attempt to (quantitatively) evaluate the resillience of a financial system to large but plausible shocks (low probability, high impact events) – What types of risk have the greatest influence? – What could be the impact of previously identified vulnerabilities and imbalances? – Are there common vulnerabilities across institutions that can undermine financial stability? 28 How to measure the impact? • Usually expressed as impact on indicators of financial system health, e.g. – Capital adequacy – Loan losses – etc… • No universal measure of financial stability developed as yet… • … so judgment plays a great role in the interpretation of results 29 Macro stress tests – some „labels” „ad-hoc” Shocks to FSIs are assumed by analysts „model-based” „single factor” „sensitivity” Impact on FSIs is based on econometric models A single risk factor is shocked – can be a macro variable or simply an FSI „scenario” Possibly multiple risk factors, comovements from macro model or historical experience 30 Macro stress tests – some „labels” „bottom-up” „top-down” Calculations done “in-house”, without engaging financial institutions Calculations performed by financial institutions, assumptions supplied by CB/supervisors These are done by the NBP 31 Ad-hoc sensitivity stress tests • Why to perform ad-hoc sensitivity simulations given the presence of more sophisticated macro stress-tests? 1. 2. 3. 4. Isolation of the impact of specific risk factors Ceteris paribus kind of analysis Prioritization of risk factors based on their isolated impact Opportunity to take advantage of data sources not included in macro stress-tests Results easier to communicate No need to specify joint distribution of risk factors which may be very challenging 5. 6. 32 Ad-hoc sensitivity stress tests • Ad-hoc nature – no specific macroeconomic scenario – no assigned probability of occurrence – scenarios chosen as (quite) extreme but plausible, based mostly on common sense, past crises can provide guidance • Tracking changes in results over time is important 33 Examples of ad-hoc stress-tests 1. Take a measure of risk in the financial system 2. Create a shock scenario, often on ad-hoc basis 3. Find the impact of shock on your measure of risk 4. Try to translate the measure of risk to FSIs (capital, earnings) 34 Example – households’ income buffer • Shock scenario – 30% zloty depreciation – Increase of interest rates on loans by 400 basis points • Results – example FSR December 2010: 30% zloty depreciation 400 bp interest rates increase Increase in the share of households with negative income buffer Increase in the share of loans extended to households with negative income buffer Increase in the share of households with negative income buffer Increase in the share of loans extended to households with negative income buffer 1.2 1.5 3.2 3.7 35 Example - „Stress-CAR” • What impact can the existing portfolio of impaired loans have on capital adequacy of banks? • What if value of loan security held for classified loans changes? (e.g. fire sale, overly optimistic valuation) 36 Stress - CAR 3 scenarios for changes in value of collateral Assumption: Only collateral can be recovered for impaired loans Losses Change in capital adequacy 37 Stress-CAR – results Basel II implementation 16% 14% 12% 10% Importance of security for loss reduction 3-2010 12-2009 9-2009 6-2009 3-2009 12-2008 9-2008 6-2008 3-2008 12-2007 9-2007 6-2007 3-2007 12-2006 9-2006 6-2006 3-2006 12-2005 9-2005 6-2005 8% Capital adequacy ratio - actual data Scenario 1 - recovery of 100% of security Scenario 2 - 25% decline in the value of security Scenario 3 - 50% decline in the value of security 38 Stress-CAR – results 60% 50% 40% 30% 20% Actual data above 16% Capital adequacy ratio Scenario 1 Scenario 2 12% - 16% 8% - 9% 6% - 8% 4% - 6% 0% - 4% below 0 0% 10% - 12% 10% 9% - 10% Share in commercial bank assets . of banks in range • Distribution of banks’ assets by „stressed” capital adequacy ratio Scenario 3 39 Macro stress test Decide on the source of shocks – ”story” Build macroeconomic stress scenario Calculate change in banks’ financial result relative to baseline scenario Calculate the changes in capital adequacy of individual banks Expert input Expert analysis Ad-hoc shocks Macro model Historical crisis Econometric models e.g. recent macro forecast 40 Constructing a macro stress test scenario – possible approaches • Market forecasts – Take the most pessimistic forecast from surveys of market participants – Easy to communicate, but is it really extreme? • Statistical – Look at fancharts of GDP growth and take an extreme pessimistic path (e.g. 5% probability) or look at residuals of forecasting model and choose an extreme shock from the distribution of residuals – Hard to communicate • Expert scenario – What is pessimistic and economically consistent? – Open to criticism of subjectivity • Historical scenario – What did the previous downturn look like? – Is it relevant? 41 Macro stress tests - December 2010 scenarios • Scenarios 12-2008 3-2009 6-2009 9-2009 12-2009 3-2010 6-2010 9-2010 12-2010 3-2011 6-2011 9-2011 12-2011 3-2012 6-2012 9-2012 12-2012 GDP (y/y) % – Baseline: October projection NBP Shock scenarios (red lines) – Shock I: longer period of low on the back of October projections of GDP economic growth in highly 9 developed countries could lead to a 8 7 fall in Poland's real GDP, further 6 increased by a hypothetical pro5 cyclical response of fiscal policy – 4 GDP ca. 4.5 pp lower than baseline 3 – Shock II: shock scenario I combined 2 with fall in foreign investor 1 confidence and additional shock for 0 the Polish economy resulting in outflows of capital from Polish GDP y/y 2010 2011 2012 market of government bonds – GDP Baseline 3,5% 4,3% 4,2% ca. 5.75 pp lower than baseline Shock I 3,4% 2,4% 2,0% – Horizon – end of 2012, as in NBP Shock II 3,4% 2,1% 1,1% macroeconomic projection 42 Calculation of impact on banks • Macro scenarios fed into panel data models to obtain forecasts of loan losses and net interest income for individual banks • Costs and non-interest income assumed constant in relation to assets • Calculation of changes in capital adequacy • Comparison with baseline scenario 43 Building blocks Macro scenarios Credit risk cost forecast Net interest income forecast Banks’ earnings Change in capital adequacy ratios and estimates of recapitalisation needs Additional assumptions Contagion effects 44 Stress tests December 2010 Results Actual data 2009Q4 2010Q3 Result Impairment charges (PLN bn) Baseline, per year over 2010Q42012Q4 Shock scenario 1 per year over 2010Q42012Q4 Shock scenario 2 per year over 2010Q42012Q4 11.0 2.2 5.1 6.5 - Enterprise loans 1.2 1.2 2.5 2.9 - Household loans 8.8 1.0 2.6 3.6 Charges as % of loans 1.9% 0.4% 0.8% 1.1% Charges as % of loans 1.2% 0.2% 0.5% 0.6% 22.0 19.9 15.9 14.8 Net earnings 9.9 14.2 8.4 5.9 Recapitalisation needs – amount of capital injection needed to keep all banks above 8% CAR n/a 0.1 0.25 0.5 Net interest income 45 commercial banks analysed 45 Stress tests December 2010 Results Distribution of commercial banks assets by capital adequacy ratio 99.3% 100.0% Share in banking sector's assets 100% 98.8% 90% 94.1% 80% 70% 60% 50% 40% Banks which need recapitalization 30% 20% 10% 0% 0.1% 0.1% 0.1% 0% 0.6% 0.6% 0.0% 0% <0% 0%-6% 5.2% 0.5% 0.6% 0.0% 6%-8% >8% Capital adequacy ratio First shock scenario- end of 2012 Baseline scenario- end of 2012 Second shock scenario - end of 2012 Actual data as at 30.09.2010 Data for 45 commercial banks was analyzed 46 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 47 How to use the results of the analysis? • Let us come back to the main objective of macroprudential policy - prevention and mitigation of systemic risk: (1) analysis of the financial system (2) early identification of risks (3) remedial action ? • Given proper identification of risks how can we mitigate them? 48 How to use the results of the analysis? • What so far has proved inefficient in safeguarding financial stability? – Central banks had in many cases proper information and analysis on potential systemic risks but also very limited set of tools for conducting macroprudential policy – Supervision authorities had wider set of tools but limited information on the sources of systemic risks and focus on microprudential aspect • A need of establishing one body provided with responsibility/mandate for macroprudential policy and adequate powers • Better coordination of various policies - use of microprudential instruments for macroprudential purposes needed • Need for cross-border coordination – Particularly vital for emerging economies with high share of foreign capital in the financial sector 49 How to use the results of the analysis? • Macro objective, but both macro & (mainly) micro tools Macroprudential objective Macro tools e.g. -counter cyclical buffers Micro tools e.g. -supervisory regulations -supervisory recommendations Moral suasion 50 Agenda • • • • • • Financial stability – general remarks Macroprudential analysis and the role of central banks How to conduct macroprudential analysis ? Stress-testing – types of stress tests and methods How to use the results ? The European context – the ESRB 51 Tasks of the ESRB • Definition and gathering of all the relevant information for the assessment of systemic risks in the EU, including on financial institutions, markets and infrastructures • Identification and prioritisation of systemic risks in the EU • Issuance of risk warnings when systemic risks are significant • Issuance of recommendations to contain the identified risks • Monitoring of the follow-up to warnings and recommendations • International coordination with the IMF, FSB, and third parties 52 52 Structure of the ESRB SECRETARIAT (Staffed by employees of the European Central Bank) Analytical, statistical, administrative and logistical support to ESRB STEERING COMMITTEE • • • Prepares meetings of the General Board Reviews documents to be discussed Monitors progress of the ESRB’s ongoing work ADVISORY SCIENTIFIC COMMITTEE 15 external experts (academics, representatives of SMEs or trade-unions, providers or consumers of financial services) with a wide range of skills and experiences GENERAL BOARD Main decision-making body Voting members include: • President and Vice-President of the ECB • Governors of EU national central banks • Member of European Commission • 3 Chairpersons of the European Supervisory Authorities (for banking, securities & markets, insurance) ADVISORY TECHNICAL COMMITTEE Representatives of national central banks, national supervisory authorities, European Supervisory Authorities 53 ESRB warnings and recommendations 1) Aimed at containing significant systemic risks, as identified by the ESRB 2) Can be be addressed to the EU as a whole, individual countries, European Supervisory Authorities or national supervisors (not individual financial institutions) 3) Recommendations include a specified timeline for policy response 4) The addressees of recommendations should report to the ESRB their actions or justify any inaction; the ESRB can decide that recommendations have not been complied with or that the justification for inaction is not appropriate 5) The ESRB can decide to publish its recommendations on a case-by-case basis, as a tool to foster compliance 54 Thank you for your attention! 55