Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Land banking wikipedia , lookup

Financial economics wikipedia , lookup

Modified Dietz method wikipedia , lookup

Pensions crisis wikipedia , lookup

Adjustable-rate mortgage wikipedia , lookup

Greeks (finance) wikipedia , lookup

Public finance wikipedia , lookup

Annual percentage rate wikipedia , lookup

Interest rate ceiling wikipedia , lookup

Interest rate swap wikipedia , lookup

Financialization wikipedia , lookup

Mark-to-market accounting wikipedia , lookup

Shareholder value wikipedia , lookup

Business valuation wikipedia , lookup

History of pawnbroking wikipedia , lookup

Continuous-repayment mortgage wikipedia , lookup

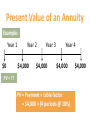

Accounts Payable Amounts owed for the purchase of inventory, goods, or services on credit Discount payment terms offered to encourage early payment Promissory Note I promise to pay $1,000 plus 12% annual interest on December 31, 2012. Date: January 1, 2012 Coffee Inc. Signed: Hot _________ S.J.Devona Total repayment = $1,120 $1,000 + ($1,000 × 12%) Discounted Promissory Note In exchange for $880 received today, I promise to pay $1,000 on December 31, 2012. Date: January 1, 2012 Coffee, Inc. Signed: Hot _________ Effective interest rate on note = 13.6% ($120 interest/$880 proceeds) Balance Sheet Presentation of Discounted Notes Discount transferred to interest expense over life of note 1/1/12 Notes Payable $1,000 Less: Discount on Notes Payable 120 Net Liability $ 880 12/31/12 $1,000 - 0 $1,000 Current Maturities of Long-Term Debt Principal repayment on borrowings due within one year of balance sheet date Due in upcoming year Taxes Payable Record expense when incurred, not when paid 12/31/11 Record 2011 tax expense 3/15/12 Taxes Paid LO2 Other Accrued Liabilities Includes any amount that has been incurred due to the passage of time but has not been paid as of the balance sheet date Examples: Salaries and Wages Interest Other Accrued Liabilities IFRS and Current Liabilities The U.S. and international standards are generally similar but there are important differences. Differences: International accounting standards require companies to present classified balance sheets with liabilities as either current or long term. An unclassified balance sheet based on the order of liquidity is acceptable only when it provides more reliable information. U.S. standards do not require a classified balance sheets. U.S. standards permit companies to list liabilities in order by size or by order of liquidity. Current Liabilities on the Statement of Cash Flows Operating Activities Net income Increase in current liability Decrease in current liability Investing Activities Financing Activities Increase in notes payable Decrease in notes payable xxx + – + – LO3 Contingent Liabilities Obligation involving existing condition Outcome not known with certainty Dependent upon some future event Actual amount is estimated LO4 Contingent Liabilities Accrue estimated amount if: • Liability is probable • Amount can be reasonably estimated Typical Contingent Liabilities Product Warranties and Guarantees Premium or coupon offers Lawsuits Recording Contingent Liabilities Probable liability has been incurred? YES Amount reasonably estimable? YES Disclosing Contingent Liabilities IF not probable but reasonably possible OR amount not estimable Disclose in Financial Statement notes Contingent Assets Contingent gains and assets are not recorded but may be disclosed in financial statement notes Conservatism principle applies IFRS and Contingencies International standards use the term “provision” for those items that must be reported on the balance sheet International standards have a lower threshold for those items that must be reported so thus more items will be recorded on the balance sheet. International standards require the amount of the recorded liability be discounted (recorded at present value). The term “contingent liability” is only used for those items that are footnoted but not for those liabilities reported on the balance sheet. Time Value of Money Prefer payment at the present time rather than in the future due to the interest factor Applicable to both personal and business decisions Simple Interest I=P×R×T LO5 Example of Simple Interest Given following data: principal amount annual interest rate term of note = $ 3,000 = 10% = 2 years Calculate interest on the note. P × R × T $3,000 × .10 × 2 = $ 600 Compound Interest Interest is calculated on principal plus previously accumulated interest • Interest on interest Compound interest amount always higher than simple interest due to interest on interest Compound Interest Periods Year 1 5% + 5% semiannually 10% annually Year 2 5% + 5% semiannually 10% annually 4 periods @ 5% semiannual interest Example of Interest Compounding Period Principal Amount at Beginning of Year 1 $3,000 $150 $3,150 2 3,150 158 3,308 3 3,308 165 3,473 4 3,473 174 3,647 Interest at Accumulated 5% per Period at End of Period Compound Interest Computations Present value of a single amount Future value of a single amount Present value of an annuity Future value of an annuity Future Value of Single Amount Known amount of single payment or investment + Interest = Future Value Future Value of a Single Amount Example: If you invest $2,000 today @ 10% compound interest, what will it be worth 2 years from now? Invest $2,000 Year 1 Future Value = ? Year 2 + Interest @ 10% per year Future Value of a Single Amount Example – Using Tables Year 1 PV = $2,000 Year 2 FV = $2,420 FV = Present value × table factor = $2,000 × (2 periods @ 10%) = $2,000 × 1.210 = $2,420 Present Value of Single Amount Known amount of single payment in future Present Value Discount Present Value of a Single Amount Example: If you will receive $2,000 in two years, what is it worth today (assuming you could invest at 10% compound interest)? Present Value = ? $2,000 Year 1 Year 2 Discount @ 10% Present Value of a Single Amount Example – Using Tables PV = $1,653 Year 1 Year 2 PV = Future value × table factor = $2,000 × (2 periods @ 10%) = $2,000 × 0.82645 = $1,653 (rounded) FV = $2,000 Future Value of an Annuity Periods 1 $0 2 $3,000 3 $3,000 4 $3,000 $3,000 + Interest Future Value = ? Future Value of an Annuity Example: Year 1 $0 Year 2 $3,000 $3,000 Year 3 $3,000 Year 4 $3,000 FV = ?? FV = Payment × table factor = $3,000 × (4 periods @ 10%) Future Value of an Annuity Example: Year 1 $0 Year 2 $3,000 Year 3 $3,000 Year 4 $3,000 PV = Payment × table factor = $3,000 × (4 periods @ 10%) = $3,000 × 4.641 = $13,923 $3,000 FV = $13,923 Present Value of an Annuity Periods 1 $0 2 $4,000 3 $4,000 Discount Present Value = ? 4 $4,000 $4,000 Present Value of an Annuity Example: Year 1 $0 Year 2 $4,000 Year 3 $4,000 Year 4 $4,000 PV = ?? PV = Payment × table factor = $4,000 × (4 periods @ 10%) $4,000 Present Value of an Annuity Example: Year 1 $0 Year 2 $4,000 Year 3 $4,000 PV = $12,679 PV = Payment × table factor = $4,000 × (4 periods @ 10%) = $4,000 × 3.16987 = $12,679 (rounded) Year 4 $4,000 $4,000 Solving for Unknowns Example Assume that you have just purchased a new car for $14,419. Your bank has offered you a 5-year loan, with annual payments of $4,000 due at the end of each year. What is the interest rate being charged on the loan? Year 1 Year 2 Year 3 Year 4 Year 5 $0 $4,000 $4,000 $4,000 $4,000 $4,000 Discount PV = $14,419 LO7 Solving for Unknowns Example Year 1 $0 Year 2 $4,000 Year 3 $4,000 Year 4 $4,000 Year 5 $4,000 PV = $14,419 PV = Payment × table factor Rearrange equation to solve for unknown Table factor = PV/payment $4,000 Solving for Unknowns Example Year 1 $0 Year 2 Year 3 $4,000 $4,000 Year 4 $4,000 Year 5 $4,000 PV = $14,419 Table factor = PV/payment = $14,419/$4,000 = 3.605 $4,000 Present Value of Annuity of $1 (n) 1 2 3 4 5 6 7 8 2% 0.980 1.942 2.884 3.808 4.713 5.601 6.472 7.325 4% 0.962 1.886 2.775 3.630 4.452 5.242 6.002 6.733 6% 0.943 1.833 2.673 3.465 4.212 4.917 5.582 6.210 8% 10% 0.926 0.909 1.783 1.736 2.577 2.487 3.312 3.170 3.993 3.791 4.623 4.355 5.206 4.868 5.747 5.335 12% 0.893 1.690 2.402 3.037 3.605 4.111 4.564 4.968 15% 0.870 1.626 2.283 2.855 3.352 3.784 4.160 4.487 The factor of 3.605 equates to an interest rate of 12% Appendix Accounting Tools: Using Excel for Problems Involving Interest Calculations Using Excel Functions Many functions built into Excel, including PV and FV calculations Click on the PASTE function (fx) of the Excel toolbar or the Insert command FV Function in Excel Example: Find the FV of a 10% note payable for $2,000, due in 2 years and compounded annually Answer: $2,420 PV Function in Excel Example: How much should you invest now at 10% (compounded annually) in order to have $2,000 in 2 years? Answer: $1,653 (rounded) End of Chapter 9