Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

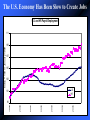

Presentation to the Tidewater Builders Association By John W. Whaley Deputy Executive Director, Economics Hampton Roads Planning District Commission February 2006 Topics • Economic Indicators • 2006 Forecast • Defense Issues • Impact of Housing Project • Housing Economics • Forecasting Permits • Impact of Construction Industry Economic Indicators The U.S. Economy The U.S. Economy Continued to Grow in 2005 Annual Percent Change in Real Gross Domestic Product 8 6 Average = 3.5% 4 2 0 -2 2005 2003 2001 1999 1997 1995 1993 1991 1989 1987 1985 1983 1981 1979 1977 1975 1973 1971 1969 1967 1965 1963 1961 1959 -4 The Hampton Roads Economy Regional Employment Continued to Grow but at a Slower Rate Twelve-Month Percent Change in Hampton Roads Civilian Employment 3% 2% 1% 0% -1% 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 -2% 1991 Twelve-Month Percent Change 4% The U.S. Economy Has Been Slow to Create Jobs U.S. and HR Payroll Employment 111 107 105 103 U.S. HR 101 2005 2004 2003 2002 2001 2000 99 1999 Index = 100 in January 1999 109 The Taxable Sales Growth Rate Slowed Hampton Roads Deseasonalized Taxable Sales $1,700,000,000 $1,600,000,000 $1,400,000,000 $1,300,000,000 $1,200,000,000 2005 2004 2003 2002 2001 $1,100,000,000 2000 Taxable Sales $1,500,000,000 Auto Sales Have Weakened Seasonally Adjusted Auto Sales in Hampton Roads 11,000 10,000 8,000 7,000 6,000 5,000 4,000 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 3,000 1986 Number of Vehicles 9,000 The Number of Homes Sold in Hampton Roads Has Begun to Decline Number of Homes Sold in Hampton Roads 2,800 2,600 2,200 2,000 1,800 1,600 1,400 1,200 2005 2004 2003 2002 2001 2000 1999 1,000 1998 Monthly Home Sales 2,400 Residential Construction Has Slowed Deseasonalized Value of HR Single Family Housing Permits $130,000,000 $110,000,000 $70,000,000 $50,000,000 $30,000,000 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 $10,000,000 1988 Dollars $90,000,000 Home Prices In Hampton Roads Have Increased Faster than Inflation Since 2001 A Comparison: Home Prices in Hampton Roads and Inflation CPI and Home Prices Indexed to 100 in 1998 250 230 210 190 170 CPI Average Home Price 150 130 110 90 1998 1999 2000 2001 2002 2003 2004 2005 HR Home Prices Have Outpaced the U.S. Increase for the Past Two Years Four Quarter Percent Change in Home Prices 30 Average: U.S. = 5.0% HR = 5.2% 25 U.S. HR 15 10 5 0 There have been 63 four-quarter changes in HR home prices since 1990 - only two exhibited a decline 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 -5 1990 Percent Change 20 The Average Selling Price of Area Housing Increased Because ….. • Demand Was Strong • Low Mortgage Rates • Military Pay Increases • Innovative Financing • Homes of Higher Value Were Constructed • The Supply of Housing Was Slow to Respond to the Increase in Demand The Pace of New Home Construction Has Not Responded to the Increase in Home Prices The Number of Hampton Roads Residential Building Permits 25,000 15,000 10,000 5,000 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 1983 1982 1981 1980 0 1979 Number of Building Permits 20,000 The Increase in Housing Values Has Driven Up the Regional Cost of Living ACCRA Cost of Living Index: Composite and Housing Cost of Living (100 = U.S. Metro Average) 105 1999 2004 100 95 90 85 80 Composite Index Forecast The Economy Will Slow Modestly in 2006 Due to …… • Higher Interest Rates • Slower Growth in Home Equity • High Energy Costs • High Consumer Debt • Less Residential Construction • Less Stimulus from the Defense Department 2006 Forecast History Long-Term 2005 Average* (Year to Date) 2006 HRPDC ODU U.S. Real GDP 3.2% 3.5% 3.1% 3.3% NA NA 3.2% 4.3% 4.4% 5.0% NA NA Real GDP 3.1% NA 2.8% 3.0% Civilian Employment 2.5% 1.6% 1.3% 1.0% Retail Sales 4.2% 9.8% 4.7% 5.0% Auto and Truck Sales 1.2% 4.2% 2.0% NA Value of Residential Building Permits 4.9% 5.2% -6.0% 1.5% Unemployment Rate 4.5% 4.2% 3.9% 4.0% Hotel Receipts 4.1% 4.9% NA 4.9% Short Government Rates Long Government Rates Hampton Roads * Length of average varies depending on the availability of data and the relevance of historic periods Defense Sector Challenges #1 Defense Spending Has “Peaked” Annualized Defense Outlays 320 Billions of Constant 1982-1984 Dollars 300 280 260 240 220 200 180 #2 Potential Relocation of Carriers • Carrier John F. Kennedy may be retired • Norfolk-based carrier could replace the JFK in Mayport • Norfolk-based Carrier George Washington will be sent to Japan in 2008 (or elsewhere in the Pacific depending on distance to Taiwan) • Cost of losing a carrier is large • Carrier without air wing: $225 million GRP • Carrier battle group and air wing: $980 million GRP #3 BRAC Impacts • Base Realignment and Closure Commissions decide on the future of domestic bases • Current BRAC recommendations have been accepted by the President and Congress On-Base Employment Will Decline by Nearly 2,400 Jobs If Oceana Remains Open Direct Employment Impact of BRAC 2005 on Hampton Roads (Excluding Oceana) 1,500 Net Impact = 2,355 Jobs Lost 1,000 500 0 -500 -1,000 -1,500 -2,000 -2,500 -3,000 Fort Monroe Portsmouth Navy Medical Center Norfolk Naval Station Yorktown NWS Oceana Open Little Creek AB Fort Eustis Langley AFB Norfolk NSA -4,000 Norfolk Naval Shipyard -3,500 How Will BRAC Impact the Regional Economy? • Used REMI Model • Nation’s most powerful regional economic model • Assumption • Direct effects were allocated across five years • Ten percent of the direct effect in 2007 – 22.5 percent in each of the years from 2008 to 2011 BRAC Impacts will be Large The Employment Impact of BRAC 2005 on Hampton Roads 0 -5000 -10000 -15000 -20000 -25000 Oceana Remains Open Oceana Closes -30000 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 When Will Impacts be Felt? (Builddown/Carriers/BRAC) • 2006: slight impact • 2007: modest impacts • 2008 – 2011: largest impacts Two Scenarios 2008 - 2011 Best Case Worst Case Lose 2400 on-base jobs Lose 2400 on-base jobs Slower increase in defense spending Lose one/two carriers Close Oceana Large cuts in defense spending Impact of New Communities Impact of New Subdivision: Population and Employment Impact of Constructing a Residential Subdivision of 1000 New Homes: Population and Employment 3500 3000 2000 Total Employment Population 1500 1000 500 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 0 2005 Units 2500 Impact of New Subdivision: Employment by Sector New Residential Subdivision with 1000 New Homes: Jobs Created 1,400 Construction Retail trade Services Government Other 1,200 800 600 400 200 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 0 2005 Jobs 1,000 Impact of a New Subdivision: City Gross Regional Product $90,000,000 $80,000,000 $70,000,000 $60,000,000 $50,000,000 $40,000,000 $30,000,000 $20,000,000 $10,000,000 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 $0 2005 Gross City Product in Constant 2000 Dollars Impact of Constructing a Residential Subdivision of 1000 New Homes: Gross City Product Housing Economics The Change in Interest Rates and the Pace of Local Economic Growth are Important Predictors of Residential Construction in HR Predicting HR Home Building (Building Expressed by the Annual Number of Residential Building Permits Issued) 7,000 6,000 Number of Building Permits 6,000 5,000 4,000 3,000 2,500 2,000 1,000 0 -1,000 Rs = 0.8 -2,000 Baseline Demand -1,400 Percentage Points of Change in Mortgage Rates Percentage Points of Change in Total Employment (Military Included) Forecasting Example Scenario One One percent increase in mortgage rates One percent increase in HR employment Calculation Replacement Demand = 6,000 units Mortgage Effect = +1 x -1,400 = -1,400 units Employment Effect = +1 x 2,500 = +2,500 units Forecast = 6,000 + (-1,400) + 2,500 = 7,100 units Scenario Two No change in mortgage rate Two percent change in HR employment Calculation Replacement Demand = 6,000 units Mortgage Effect = 0 Employment Effect = +2 x 2,500 = +5,000 units Forecast = 6,000 + 5,000 = 11,000 units Impact of the HR Construction Industry Output $7.6 Billion Gross Regional Product $3.9 Billion Jobs 80,000 The End