CPA PassMaster Questions–Auditing 4 Export Date: 10/30/08

... Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same; either both would be overstated (the most likely case) or both would be understated. Choice "b" is incorrect. Even the lack of effective internal cont ...

... Choice "a" is incorrect. If fictitious transactions in the revenue cycle are recorded, then the impact on revenues and receivables would be the same; either both would be overstated (the most likely case) or both would be understated. Choice "b" is incorrect. Even the lack of effective internal cont ...

Does the Big-4 Effect Exist when Reputation and

... when the characteristics of audit partners and auditees are held constant. When an audit partner switches her affiliation with an audit firm to a different firm, some auditees follow the partner (hereafter, the partner-auditee pair). Employing a unique dataset of individual auditors for a large samp ...

... when the characteristics of audit partners and auditees are held constant. When an audit partner switches her affiliation with an audit firm to a different firm, some auditees follow the partner (hereafter, the partner-auditee pair). Employing a unique dataset of individual auditors for a large samp ...

Defence Audit Guidelines_Final 25 March 2010

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

Returns to Buying Earnings and Book Value: Accounting for Growth

... incorrect, but that also goes against the grain of accounting principles. Lower book values create both short-term earnings and long-term growth so, to reconcile the observation that B/P predicts returns with the idea that growth is risky, it has to be that B/P bears on the identifying long-term gro ...

... incorrect, but that also goes against the grain of accounting principles. Lower book values create both short-term earnings and long-term growth so, to reconcile the observation that B/P predicts returns with the idea that growth is risky, it has to be that B/P bears on the identifying long-term gro ...

Substantive Tests of Transactions and Balances

... audit approach detailed in the audit program to ensure that the most efficient and effective combination of audit procedures is used. No matter what audit strategy is adopted, the auditor must undertake substantive tests and usually makes considerable use of direct tests of balances. In audits of th ...

... audit approach detailed in the audit program to ensure that the most efficient and effective combination of audit procedures is used. No matter what audit strategy is adopted, the auditor must undertake substantive tests and usually makes considerable use of direct tests of balances. In audits of th ...

Yes, there is a big Difference between Audit on Profit Organizations

... reporting. Due to the requirement of Section 404 of the Sarbanes Oxley Act of 2002 for management to also assess the effectiveness of their internal controls over financial reporting (as also required of the external auditor), internal auditors are utilized to make this assessment. Though internal a ...

... reporting. Due to the requirement of Section 404 of the Sarbanes Oxley Act of 2002 for management to also assess the effectiveness of their internal controls over financial reporting (as also required of the external auditor), internal auditors are utilized to make this assessment. Though internal a ...

MANDATORY EMPHASIS PARAGRAPHS, CLARIFYING

... ‘‘expectations gap’’ between the level of assurance expected and the actual level of assurance delivered by auditors (Asare and Wright 2012; Hogan et al. 2008; Low and Boo 2012; McEnroe and Martens 2001; Reffett et al. 2012). This expectation gap makes it difficult for auditors to know the level of ...

... ‘‘expectations gap’’ between the level of assurance expected and the actual level of assurance delivered by auditors (Asare and Wright 2012; Hogan et al. 2008; Low and Boo 2012; McEnroe and Martens 2001; Reffett et al. 2012). This expectation gap makes it difficult for auditors to know the level of ...

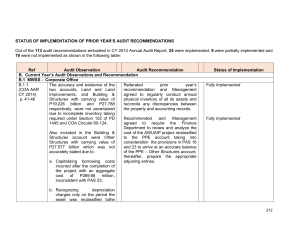

MWSS2015_Part3-Status_of_PY`s_Recomm

... B. Current Year’s Audit Observations and Recommendation B.1 MWSS - Corporate Office B.1.1 The accuracy and existence of the Reiterated prior year’s (COA AAR two accounts, Land and Land recommendation and Management CY 2014) Improvements, and Building & agreed to regularly conduct annual p. 41-46 Str ...

... B. Current Year’s Audit Observations and Recommendation B.1 MWSS - Corporate Office B.1.1 The accuracy and existence of the Reiterated prior year’s (COA AAR two accounts, Land and Land recommendation and Management CY 2014) Improvements, and Building & agreed to regularly conduct annual p. 41-46 Str ...

Detecting asset misappropriation: a framework for

... to examine areas related to asset misappropriation that had never been examined before and alert external auditors in Egypt to a type of fraud which was given less attention. The current study also proposed a framework for external auditors that might help them properly assess and respond to fraud r ...

... to examine areas related to asset misappropriation that had never been examined before and alert external auditors in Egypt to a type of fraud which was given less attention. The current study also proposed a framework for external auditors that might help them properly assess and respond to fraud r ...

Empirical evidence on liability caps and earnings management in

... goals are reducing the risk of a Big 4 firm collapse and encouraging middle-sized audit firms to offer their services to listed clients2. The Commission recommends that EU member states should limit auditors’ liability, but does not oblige them to take action. It also gives member states the freedom ...

... goals are reducing the risk of a Big 4 firm collapse and encouraging middle-sized audit firms to offer their services to listed clients2. The Commission recommends that EU member states should limit auditors’ liability, but does not oblige them to take action. It also gives member states the freedom ...

DCIS Score slide module

... • Additional research that provides confirmation and more experience in certain groups (e.g., higher risk DCIS and ER negative DCIS) • Identification of predictive genes for radiation sensitivity and/or resistance • Next Generation Sequencing to explore whether new genes might be identified that act ...

... • Additional research that provides confirmation and more experience in certain groups (e.g., higher risk DCIS and ER negative DCIS) • Identification of predictive genes for radiation sensitivity and/or resistance • Next Generation Sequencing to explore whether new genes might be identified that act ...

Lesson Preparation Project

... achieve some specific objective” There are two ways to think about earnings management: as an opportunistic behaviour by managers to maximize their utility and from an efficient contracting perspective. Issues arise in regards to earnings management due to the choice of accounting policies, discreti ...

... achieve some specific objective” There are two ways to think about earnings management: as an opportunistic behaviour by managers to maximize their utility and from an efficient contracting perspective. Issues arise in regards to earnings management due to the choice of accounting policies, discreti ...

Explicit solutions for dynamic portfolio choice in jump

... asset prices, there are only a few studies on asset allocation in the presence of jumps in both stock prices and state variables. Liu, Longstaff and Pan (2003) solve the optimal portfolio choice problem in closed form for a model where there is only one risky asset with jumps in both stock price and ...

... asset prices, there are only a few studies on asset allocation in the presence of jumps in both stock prices and state variables. Liu, Longstaff and Pan (2003) solve the optimal portfolio choice problem in closed form for a model where there is only one risky asset with jumps in both stock price and ...

Speculation and Risk Sharing with New Financial Assets Alp Simsek

... the implications of heterogenous beliefs for security design. For example, in their survey of the literature, Du¢ e and Rahi (1994) note that “one theme of the literature, going back at least to Working (1953) and evident in the Milgrom and Stokey (1982) no-trade theorem, is that an exchange would r ...

... the implications of heterogenous beliefs for security design. For example, in their survey of the literature, Du¢ e and Rahi (1994) note that “one theme of the literature, going back at least to Working (1953) and evident in the Milgrom and Stokey (1982) no-trade theorem, is that an exchange would r ...

BUSINESS RISK AND THE TRADEOFF THEORY OF

... borrowing (Stiglitz 1988). Understanding these market imperfections and how they affect the value of firms has been the focus of much research subsequent to Modigliani and Miller. The efforts ...

... borrowing (Stiglitz 1988). Understanding these market imperfections and how they affect the value of firms has been the focus of much research subsequent to Modigliani and Miller. The efforts ...

ActionAid International Financial Management Framework

... Streamline processes for recording financial events and reporting financial information ...

... Streamline processes for recording financial events and reporting financial information ...

Portfolio Value-at-Risk Using Regular Vine Copulas

... Risk is related to randomness and uncertainty. For example, insurance companies, home owners or investors all (to a different degree) face uncertainty in the future value of their products. We can analyze risk in the context of the risk type. The three biggest categories of financial risks are marke ...

... Risk is related to randomness and uncertainty. For example, insurance companies, home owners or investors all (to a different degree) face uncertainty in the future value of their products. We can analyze risk in the context of the risk type. The three biggest categories of financial risks are marke ...

User guide to Standing Direction 1

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

Notes 17 - Wharton Statistics

... From a Bayesian point of view, estimators that are limits of Bayes estimators are somewhat more desirable than generalized Bayes estimators (often estimators are both limit of Bayes estimators and generalized Bayes estimators as in Example 1). This is because, by construction, a limit of Bayes estim ...

... From a Bayesian point of view, estimators that are limits of Bayes estimators are somewhat more desirable than generalized Bayes estimators (often estimators are both limit of Bayes estimators and generalized Bayes estimators as in Example 1). This is because, by construction, a limit of Bayes estim ...

table of contents - Caritas University

... To achieve the above mission and goals, the management of the establishment must adopt measures to ensure that available resources are prudently used to obtain valve for money from resources allocated to them. Management in turn should generate operational data with which they evaluate the efficienc ...

... To achieve the above mission and goals, the management of the establishment must adopt measures to ensure that available resources are prudently used to obtain valve for money from resources allocated to them. Management in turn should generate operational data with which they evaluate the efficienc ...

EXSO EP _ W ISOLE GB

... the same, ensure safety of lone workers (lone working can make rescuing a person more difficult in case of accident) • Reminder • the need to identify all types of lone working • the need to assess risks ...

... the same, ensure safety of lone workers (lone working can make rescuing a person more difficult in case of accident) • Reminder • the need to identify all types of lone working • the need to assess risks ...

Auditor Liability and Professional Skepticism: A Look at Lehman

... conclude that each material financial statement assertion is supported. It is skepticism that drives auditors’ judgments regarding what, and how much, evidence will be needed to achieve this. Unlike accounting principles, which are prescriptive and mechanical in nature, auditing rules are essential ...

... conclude that each material financial statement assertion is supported. It is skepticism that drives auditors’ judgments regarding what, and how much, evidence will be needed to achieve this. Unlike accounting principles, which are prescriptive and mechanical in nature, auditing rules are essential ...

EFFECTS OF INTERNAL CONTROLS ON REVENUE COLLECTION

... 4.2.1.1 Accounting and Financial management system .................................................... 28 4.2.1.2 Management commitment on the operations of the system .................................. 28 ...

... 4.2.1.1 Accounting and Financial management system .................................................... 28 4.2.1.2 Management commitment on the operations of the system .................................. 28 ...

working program - Almaty Management University

... positions, and suggest new approaches; Reach compromise, correlate their opinions with the opinions of the team members; Aim or professional and personal development; Use information technologies in their professional work; Navigate information streams, and be able to face challenges of the audit; - ...

... positions, and suggest new approaches; Reach compromise, correlate their opinions with the opinions of the team members; Aim or professional and personal development; Use information technologies in their professional work; Navigate information streams, and be able to face challenges of the audit; - ...