Study Guide for Final

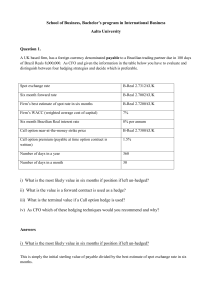

... detail? Does your answer to the previous question depend upon whether you have a long or short position? Explain. Why do speculators and hedgers have different position limits? How does open interest differ from volume? When a contract trades does the open interest increase, decrease, or not change? ...

... detail? Does your answer to the previous question depend upon whether you have a long or short position? Explain. Why do speculators and hedgers have different position limits? How does open interest differ from volume? When a contract trades does the open interest increase, decrease, or not change? ...

Review of Topics for Midterm 2

... Production decision rule: The seller will produce one more unit of a good or service if the price for which it can be sold exceeds or equals its marginal cost. A supply curve is a marginal cost curve. Producer surplus: The price of a good minus the opportunity cost of producing it. In other words, p ...

... Production decision rule: The seller will produce one more unit of a good or service if the price for which it can be sold exceeds or equals its marginal cost. A supply curve is a marginal cost curve. Producer surplus: The price of a good minus the opportunity cost of producing it. In other words, p ...

C14_Reilly1ce

... options because it allows security price changes to occur in distinct upward or downward movements • Prices can change continuously throughout time • Advantage of Black-Scholes approach is relatively simple, closed-form equation capable of valuing options accurately under a wide array of circumstanc ...

... options because it allows security price changes to occur in distinct upward or downward movements • Prices can change continuously throughout time • Advantage of Black-Scholes approach is relatively simple, closed-form equation capable of valuing options accurately under a wide array of circumstanc ...

Professor Banko`s Presentation

... • Short side is a PE firm with a short position on 50,000 shares sold @ $200 (ignoring rest of hedge). ...

... • Short side is a PE firm with a short position on 50,000 shares sold @ $200 (ignoring rest of hedge). ...

УДК 336.7 JEL Code G10 С.М. ДЕНЬГА (Полтавський університет

... Hedging was made possible thanks to the development of the markets in which these risks are redistributed among the participants. At the international and national markets is carried out exchange and OTC trading of different assets and instruments. But the hedge, unfortunately, have not yet used fir ...

... Hedging was made possible thanks to the development of the markets in which these risks are redistributed among the participants. At the international and national markets is carried out exchange and OTC trading of different assets and instruments. But the hedge, unfortunately, have not yet used fir ...

FORM 8-K - corporate

... On July 5, 2006, the compensation committee (the “Committee”) of the Board of Directors (the “Board”) of Guess?, Inc. (the “Company”) and the Board approved an amendment (the “Amendment”) to the Guess?, Inc. 2006 Non-Employee Directors’ Stock Grant and Stock Option Plan (the “Plan”) to change the in ...

... On July 5, 2006, the compensation committee (the “Committee”) of the Board of Directors (the “Board”) of Guess?, Inc. (the “Company”) and the Board approved an amendment (the “Amendment”) to the Guess?, Inc. 2006 Non-Employee Directors’ Stock Grant and Stock Option Plan (the “Plan”) to change the in ...