An Expanded Study on the Stock Market Temperature

... Finland while the highest temperature was 35.00°C in Athens, Greece. For most cities, the ...

... Finland while the highest temperature was 35.00°C in Athens, Greece. For most cities, the ...

Cross-Sectional Dispersion and Expected Returns

... to be robust across multiple forecasting horizons (see Guo and Savickas, 2008, for evidence on the G7 countries). Other studies provide supporting evidence of a significant relationship between dispersion and the returns of value and momentum premia (Angelidis et al., 2015; Bhootra, 2011; Connolly ...

... to be robust across multiple forecasting horizons (see Guo and Savickas, 2008, for evidence on the G7 countries). Other studies provide supporting evidence of a significant relationship between dispersion and the returns of value and momentum premia (Angelidis et al., 2015; Bhootra, 2011; Connolly ...

Chapter 13 Equity Valuation Multiple Choice Questions 1. The

... expected holding period is three times as long as Bill's. C. Shelly should be willing to pay the most for the stock because she will hold it the longest and hence will get the most dividends. D. All three should be willing to pay the same amount for the stock regardless of their holding period. ...

... expected holding period is three times as long as Bill's. C. Shelly should be willing to pay the most for the stock because she will hold it the longest and hence will get the most dividends. D. All three should be willing to pay the same amount for the stock regardless of their holding period. ...

Chapter 018 Dividends and Dividend Policy

... a. The chief financial officer of a corporation determines whether or not a dividend will be paid. b. A dividend is not a liability of a firm until it has been declared. c. If a firm has paid regular quarterly dividends in the past it is legally obligated to continue doing so. d. Cash dividends alwa ...

... a. The chief financial officer of a corporation determines whether or not a dividend will be paid. b. A dividend is not a liability of a firm until it has been declared. c. If a firm has paid regular quarterly dividends in the past it is legally obligated to continue doing so. d. Cash dividends alwa ...

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE

... CHAPTER 6 B-13 10. In general, viatical settlements are ethical. In the case of a viatical settlement, it is simply an exchange of cash today for payment in the future, although the payment depends on the death of the seller. The purchaser of the life insurance policy is bearing the risk that the i ...

... CHAPTER 6 B-13 10. In general, viatical settlements are ethical. In the case of a viatical settlement, it is simply an exchange of cash today for payment in the future, although the payment depends on the death of the seller. The purchaser of the life insurance policy is bearing the risk that the i ...

a century of stock market liquidity and trading

... example, if agents face large transaction costs at certain times, realized equity returns might be considerably lower than the gross equity returns implicit in stock index values. If frictions are substantial, asset price behavior that might initially appear anomalous could be well within transactio ...

... example, if agents face large transaction costs at certain times, realized equity returns might be considerably lower than the gross equity returns implicit in stock index values. If frictions are substantial, asset price behavior that might initially appear anomalous could be well within transactio ...

Institutional Investment Constraints and Stock Prices

... Lewellen (2011)). Such “benchmark investing” behavior contradicts predictions of neoclassic models: institutional investors are usually viewed as being better informed than individual investors. Thus, they should overweight stocks that have positive news and underweight stocks with negative news. Ho ...

... Lewellen (2011)). Such “benchmark investing” behavior contradicts predictions of neoclassic models: institutional investors are usually viewed as being better informed than individual investors. Thus, they should overweight stocks that have positive news and underweight stocks with negative news. Ho ...

Chapter 21 Glossary

... bargain-purchase option An option that allows a lessee to purchase the leased property for a price that is significantly lower than the property’s expected fair value at the date the option becomes exercisable. At the inception of the lease, the difference between the option price and the expected f ...

... bargain-purchase option An option that allows a lessee to purchase the leased property for a price that is significantly lower than the property’s expected fair value at the date the option becomes exercisable. At the inception of the lease, the difference between the option price and the expected f ...

An Overview of Fee Structures in Real Estate Funds and Their

... management fees may not only sustain the manager’s business platform but they may also provide significant profits. With regard to these investment management fees, investors need to understand both the static effects of such fees on returns and the behavioral effects of such fees – particularly inc ...

... management fees may not only sustain the manager’s business platform but they may also provide significant profits. With regard to these investment management fees, investors need to understand both the static effects of such fees on returns and the behavioral effects of such fees – particularly inc ...

Ineffi cient Investment Waves - The University of Chicago Booth

... Cash can be stored safely, exchanged for consumption goods, or used to build new capital at a constant proportional cost. Capital can also be liquidated for a relatively smaller constant proportional bene…t in terms of cash. Thus, aggregate cash holdings represent non-…nancial …rms’ liquid …nancial ...

... Cash can be stored safely, exchanged for consumption goods, or used to build new capital at a constant proportional cost. Capital can also be liquidated for a relatively smaller constant proportional bene…t in terms of cash. Thus, aggregate cash holdings represent non-…nancial …rms’ liquid …nancial ...

ACCT 2301 PP Ch 7

... Sales on Credit and Accounts Receivable Subsidiary Ledger On July 16, Barton, Co. sells $950 of merchandise on credit to Webster Co., and $1,000 of merchandise on account to Matrix, Inc. DR ...

... Sales on Credit and Accounts Receivable Subsidiary Ledger On July 16, Barton, Co. sells $950 of merchandise on credit to Webster Co., and $1,000 of merchandise on account to Matrix, Inc. DR ...

Successful Activist Board Engagement

... fund created positive abnormal returns (alpha) for all shareholders during short term event windows and for a five year period ex post the activist joining the target firm board. Additionally, those target firms increased certain operating performance measures that are commonly used by financial eco ...

... fund created positive abnormal returns (alpha) for all shareholders during short term event windows and for a five year period ex post the activist joining the target firm board. Additionally, those target firms increased certain operating performance measures that are commonly used by financial eco ...

prospectus - Cullen Funds

... Like all investments, investing in the High Dividend Fund involves risks, including the risk that you may lose part or all of the money you invest. General Stock Risks. The High Dividend Fund’s major risks are those of investing in the stock market, which can mean that the Fund may experience sudden ...

... Like all investments, investing in the High Dividend Fund involves risks, including the risk that you may lose part or all of the money you invest. General Stock Risks. The High Dividend Fund’s major risks are those of investing in the stock market, which can mean that the Fund may experience sudden ...

NBER WORKING PAPER SERIES THE EQUITY PREMIUM IN RETROSPECT Rajnish Mehra

... and Prescott (1985), we reported arithmetic averages, since the best available evidence indicated that stock returns were uncorrelated over time. When this is the case, the expected future value of a $1 investment is obtained by compounding the arithmetic average of the sample return, which is the c ...

... and Prescott (1985), we reported arithmetic averages, since the best available evidence indicated that stock returns were uncorrelated over time. When this is the case, the expected future value of a $1 investment is obtained by compounding the arithmetic average of the sample return, which is the c ...

The securities described in this prospectus are offered

... Using borrowed money to finance the purchase of securities involves greater risk than a purchase using cash resources only. If you borrow money to purchase securities, your responsibility to repay the loan and pay interest as required under its terms remains the same even if the securities decrease ...

... Using borrowed money to finance the purchase of securities involves greater risk than a purchase using cash resources only. If you borrow money to purchase securities, your responsibility to repay the loan and pay interest as required under its terms remains the same even if the securities decrease ...

Slices - personal.kent.edu

... Beginning Accounts Receivable = $30 Average collection period = 30 days Purchases from suppliers = 50% of current quarter’s estimated sales, at the beginning of each quarter Accounts payable period = 45 days Wages, taxes and other expenses = 25% of sales Interest and dividends = $5 million per quart ...

... Beginning Accounts Receivable = $30 Average collection period = 30 days Purchases from suppliers = 50% of current quarter’s estimated sales, at the beginning of each quarter Accounts payable period = 45 days Wages, taxes and other expenses = 25% of sales Interest and dividends = $5 million per quart ...

Finding Smart Beta in the Factor Zoo_pdf

... zoo.1 While the concept is entertaining, the proliferation of factors is deeply troubling. The sheer number of factors suggests that it’s better to have more factors than less, but how can investors determine how to use factors in their equity portfolios? The options are endless, particularly given ...

... zoo.1 While the concept is entertaining, the proliferation of factors is deeply troubling. The sheer number of factors suggests that it’s better to have more factors than less, but how can investors determine how to use factors in their equity portfolios? The options are endless, particularly given ...

Alternative risk premia investing: from theory to practice

... For illustrative purposes only. The two series are based on a developed markets (G10 currencies) carry strategy. The strategy is riskweighted, where a long (short) position is held in a currency whose risk-free rate differential vs. the USD risk-free rate is higher (lower) than the median. The risk ...

... For illustrative purposes only. The two series are based on a developed markets (G10 currencies) carry strategy. The strategy is riskweighted, where a long (short) position is held in a currency whose risk-free rate differential vs. the USD risk-free rate is higher (lower) than the median. The risk ...

The Impact of Skewness and Fat Tails on the Asset Allocation Decision

... Many assets’ return distributions are asymmetrical. In other words, the distribution is skewed to the left (or occasionally the right) of the mean (expected) value. In addition, most asset return distributions are more leptokurtic, or fatter tailed, than are normal distributions. The normal distribu ...

... Many assets’ return distributions are asymmetrical. In other words, the distribution is skewed to the left (or occasionally the right) of the mean (expected) value. In addition, most asset return distributions are more leptokurtic, or fatter tailed, than are normal distributions. The normal distribu ...

USD strength hits a roadblock

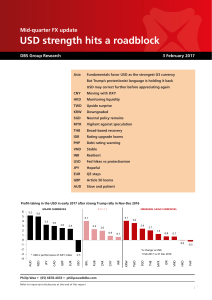

... headwinds from the global USD fairly well. The DXY Index is our reference for the global USD below. Currencies of high growth economies – PHP, IDR, VND and INR – were notably resilient when DXY rallied strongly in Nov-Dec 2016. They were, however, less willing to appreciate when DXY retreated in ear ...

... headwinds from the global USD fairly well. The DXY Index is our reference for the global USD below. Currencies of high growth economies – PHP, IDR, VND and INR – were notably resilient when DXY rallied strongly in Nov-Dec 2016. They were, however, less willing to appreciate when DXY retreated in ear ...

Returning Cash to the Owners: Dividend Policy

... Assume that you run a phone company, and that you have historically paid large dividends. You are now planning to enter the telecommunications and media markets. Which of the following paths are you most likely to follow? Courageously announce to your stockholders that you plan to cut dividends and ...

... Assume that you run a phone company, and that you have historically paid large dividends. You are now planning to enter the telecommunications and media markets. Which of the following paths are you most likely to follow? Courageously announce to your stockholders that you plan to cut dividends and ...

The Effectiveness of Sell Discipline Strategies in Institutional Portfolios

... help an investment manager avoid their own cognitive biases, and reap higher returns. The contributions from behavioral finance are important in that they in part explain the results of the Faugère et al. study. During a bear market, where most investors are facing losses, the valuation sell discipl ...

... help an investment manager avoid their own cognitive biases, and reap higher returns. The contributions from behavioral finance are important in that they in part explain the results of the Faugère et al. study. During a bear market, where most investors are facing losses, the valuation sell discipl ...

RP 2011-45 - Department of Economics and Business Economics

... the empirical (solid lines) and normal (dash-dots) threshold correlations are striking. For example, while the unconditional correlation between the market and size factor in Table 1 indicates near independence under the bivariate normality assumption, the threshold correlation in the top-right pane ...

... the empirical (solid lines) and normal (dash-dots) threshold correlations are striking. For example, while the unconditional correlation between the market and size factor in Table 1 indicates near independence under the bivariate normality assumption, the threshold correlation in the top-right pane ...