What is a Freight Forward?

... Match your forward position with your forward opinion – are you happy? – if not, FIX IT! – can still Time Charter (out or in) or do Contracts, but also FFAs ...

... Match your forward position with your forward opinion – are you happy? – if not, FIX IT! – can still Time Charter (out or in) or do Contracts, but also FFAs ...

Pension fund equity investment

... The conceptual basis is that risk is always relative to the liabilities, When the liabilities are of long duration the relative risk differs from that when the liabilities are at call, The difference arises from the auto-correlation of share returns, This factor is neglected in the simple financial ...

... The conceptual basis is that risk is always relative to the liabilities, When the liabilities are of long duration the relative risk differs from that when the liabilities are at call, The difference arises from the auto-correlation of share returns, This factor is neglected in the simple financial ...

Q1 Thoughts on the Market

... We have continued to witness less correlation among global markets, which we saw starting in 2014. During 2014, U.S. investors saw more muted returns because of the inclusion of international stocks – the exact opposite was witnessed during the first quarter of 2015 where international stocks helped ...

... We have continued to witness less correlation among global markets, which we saw starting in 2014. During 2014, U.S. investors saw more muted returns because of the inclusion of international stocks – the exact opposite was witnessed during the first quarter of 2015 where international stocks helped ...

The Case for Middle Market Lending

... low. Investors in traditional fixed income have three basic options: Wait out the low rates and accept lower returns in the meantime; take more interest rate risk; take more credit risk in liquid markets. In this low interest rate environment, which option offers the best balance of risk and potenti ...

... low. Investors in traditional fixed income have three basic options: Wait out the low rates and accept lower returns in the meantime; take more interest rate risk; take more credit risk in liquid markets. In this low interest rate environment, which option offers the best balance of risk and potenti ...

Presentation - Kerns Capital Management, Inc.

... and political uncertainty; and derivative securities, which may carry market, credit, and liquidity risks. The Fund may also engage in short selling activities, which are more risky than "long" positions because the potential loss on a short sell is unlimited. The Fund may use leveraging and/or hedg ...

... and political uncertainty; and derivative securities, which may carry market, credit, and liquidity risks. The Fund may also engage in short selling activities, which are more risky than "long" positions because the potential loss on a short sell is unlimited. The Fund may use leveraging and/or hedg ...

Kaufmann Large Cap Fund - Investor Fact Sheet

... The holdings percentages are based on net assets at the close of business on 3/31/17 and may not necessarily reflect adjustments that are routinely made when presenting net assets for formal financial statement purposes. Because this is a managed portfolio, the investment mix will change. Total retu ...

... The holdings percentages are based on net assets at the close of business on 3/31/17 and may not necessarily reflect adjustments that are routinely made when presenting net assets for formal financial statement purposes. Because this is a managed portfolio, the investment mix will change. Total retu ...

De-risking pension funds across the board

... longevity risk transfer markets. Since 2007, more than $280 billion in pension risk transfer transactions have occurred in the US, UK and Canada. The Netherlands is also a vibrant market. Key trends driving growth in these countries today and expected to continue in 2017, include: customisation of l ...

... longevity risk transfer markets. Since 2007, more than $280 billion in pension risk transfer transactions have occurred in the US, UK and Canada. The Netherlands is also a vibrant market. Key trends driving growth in these countries today and expected to continue in 2017, include: customisation of l ...

OnePath Diversified Fixed Interest

... The appointment of each new, underlying investment manager becomes effective on or around 1 April 2012. We will conduct a transition of the underlying securities (assets) to each new, underlying investment manager. This transition will be conducted over a period of time such that each new manager’s ...

... The appointment of each new, underlying investment manager becomes effective on or around 1 April 2012. We will conduct a transition of the underlying securities (assets) to each new, underlying investment manager. This transition will be conducted over a period of time such that each new manager’s ...

Chapter 9 Behavioral Finance and Technical Analysis

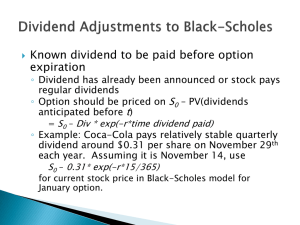

... – The prices of growth stocks may be consistently bid too high due to investor overconfidence. – Investors/analysts may extrapolate recent earnings (and dividend) growth too far into the future and thereby inflate stock prices, forcing poor returns eventually on growth portfolios. – At any given tim ...

... – The prices of growth stocks may be consistently bid too high due to investor overconfidence. – Investors/analysts may extrapolate recent earnings (and dividend) growth too far into the future and thereby inflate stock prices, forcing poor returns eventually on growth portfolios. – At any given tim ...

The constant asset allocation comparison

... Jeremy Grantham (Pearlman and Dahl, 2009) has argued that markets are inefficient and investors can improve risk adjusted returns by engaging in strategic asset allocation, changing the style mix in response to valuation changes. GMO offers a mutual fund which is free to change its composition of as ...

... Jeremy Grantham (Pearlman and Dahl, 2009) has argued that markets are inefficient and investors can improve risk adjusted returns by engaging in strategic asset allocation, changing the style mix in response to valuation changes. GMO offers a mutual fund which is free to change its composition of as ...

OCBSFFund1qtr2014 copy

... Collective Investment Schemes in Securities (CIS) are generally medium to long term investments. The value of participatory interests (units) may go down as well as up and past performance is not necessarily a guide to the future. Different classes of units apply to some of the Oasis Funds, which ar ...

... Collective Investment Schemes in Securities (CIS) are generally medium to long term investments. The value of participatory interests (units) may go down as well as up and past performance is not necessarily a guide to the future. Different classes of units apply to some of the Oasis Funds, which ar ...

Diversification Structure is the Strategy

... your timing right have far less influence over the long term. This is an approach based on science, not guesswork. Your key decision is how to combine these asset classes in a diversified portfolio, based on your own risk appetite and goals. ...

... your timing right have far less influence over the long term. This is an approach based on science, not guesswork. Your key decision is how to combine these asset classes in a diversified portfolio, based on your own risk appetite and goals. ...

Markowitz and the Expanding Definition of Risk: Applications of Multi

... Equation (2.11) defines the Security Market Line (SML), which describes the linear relationship between the security’s return and its systematic risk, as measured by beta. Let us estimate beta coefficients to be used in the Capital Asset Pricing Model (CAPM) to determine the rate of return on equity ...

... Equation (2.11) defines the Security Market Line (SML), which describes the linear relationship between the security’s return and its systematic risk, as measured by beta. Let us estimate beta coefficients to be used in the Capital Asset Pricing Model (CAPM) to determine the rate of return on equity ...

Handling Market Volatility

... access your funds) may be the right strategy for you if your investment goals are short term and you'll need the money soon, or if you're growing close to reaching a long-term goal such as retirement. But if you still have years to invest, keep in mind that stocks have historically outperformed stab ...

... access your funds) may be the right strategy for you if your investment goals are short term and you'll need the money soon, or if you're growing close to reaching a long-term goal such as retirement. But if you still have years to invest, keep in mind that stocks have historically outperformed stab ...

The GreaT DebaTe: Income vs . ToTal reTurn

... higher-quality bonds have low correlation to one another, so that bonds generally offer positive returns when stocks are falling and broad bond indexes have fairly low volatility. It is well documented that current yield on high-quality bonds is an excellent predictor of future expected return.4 Whe ...

... higher-quality bonds have low correlation to one another, so that bonds generally offer positive returns when stocks are falling and broad bond indexes have fairly low volatility. It is well documented that current yield on high-quality bonds is an excellent predictor of future expected return.4 Whe ...

Revisiting the low volatility anomaly

... to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase ...

... to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase ...

Momentum-Value in Options

... budget and operational platform in place to meet this demand, can supply options and take advantage of the excess spread between implied and realized volatility. Part of the spread might be explained by stochastic volatility and jumps in the underlying asset, part of the spread coming from the inves ...

... budget and operational platform in place to meet this demand, can supply options and take advantage of the excess spread between implied and realized volatility. Part of the spread might be explained by stochastic volatility and jumps in the underlying asset, part of the spread coming from the inves ...

December 30, 2011

... The Dow Jones Industrial Average closed at 18,312.39 on May 19th. Since then, the Blue Chip Index has clearly started a downward trend marked by a series of waves lower and higher. Each wave lower closed lower than its previous low and each wave higher failed to surpass its previous high. It closed ...

... The Dow Jones Industrial Average closed at 18,312.39 on May 19th. Since then, the Blue Chip Index has clearly started a downward trend marked by a series of waves lower and higher. Each wave lower closed lower than its previous low and each wave higher failed to surpass its previous high. It closed ...

MAY 2010. FINAL doc - Institute of Bankers in Malawi

... The expected rate of return is the rate expected to be realised from an investment and is calculated by multiplying the probabilities of occurrence by their associated outcomes. The required rate of return is the minimum return an investor would require from an investment, given the riskiness of the ...

... The expected rate of return is the rate expected to be realised from an investment and is calculated by multiplying the probabilities of occurrence by their associated outcomes. The required rate of return is the minimum return an investor would require from an investment, given the riskiness of the ...

4th Quarter 2013 Investor Newsletter

... spread has averaged 1.6%, which is largely consistent with reduced inflation expectations going forward. So, where are we today? At the end ...

... spread has averaged 1.6%, which is largely consistent with reduced inflation expectations going forward. So, where are we today? At the end ...

Option Price and Portfolio Simulation

... expiration t years from now. Discount the cash flow value back to time 0 by multiplying by e-rt to calculate the current value of the option. Select the current value of the option as the output variable to determine its mean price and other ...

... expiration t years from now. Discount the cash flow value back to time 0 by multiplying by e-rt to calculate the current value of the option. Select the current value of the option as the output variable to determine its mean price and other ...

Sanlam Investment Management Value Fund Class A1

... long term (greater than 5 years). It is designed to substantially outperform the markets and therefore carries a long-term investment horizon (5 years and upwards). The portfolio will be diversified across all major asset classes with significant exposure to equities, and may include offshore equiti ...

... long term (greater than 5 years). It is designed to substantially outperform the markets and therefore carries a long-term investment horizon (5 years and upwards). The portfolio will be diversified across all major asset classes with significant exposure to equities, and may include offshore equiti ...

Proposal on stock prediction return of Pakistan

... ratio will be low when stocks are overpriced; they predict low future returns as prices return to fundamentals. The other theory is of rational pricing which says that the ratio track time variation in discount variations i.e. the ratio will be low when discounts are low and high when discounts rate ...

... ratio will be low when stocks are overpriced; they predict low future returns as prices return to fundamentals. The other theory is of rational pricing which says that the ratio track time variation in discount variations i.e. the ratio will be low when discounts are low and high when discounts rate ...

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

... performance is merely “neutral” (i.e., has zero excess return), then we conclude that the manager has on average made good stock picks. Stock selection must be the source of the positive excess returns. Timing ability is indicated by the curvature of the plotted line. Lines that become steeper as yo ...

... performance is merely “neutral” (i.e., has zero excess return), then we conclude that the manager has on average made good stock picks. Stock selection must be the source of the positive excess returns. Timing ability is indicated by the curvature of the plotted line. Lines that become steeper as yo ...

MARKETS - Man Group

... instruments composing any one index. Certain information is based on data provided by third-party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. Unless stated otherwise this information is communicated by Fina ...

... instruments composing any one index. Certain information is based on data provided by third-party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. Unless stated otherwise this information is communicated by Fina ...

Beta (finance)

In finance, the beta (β) of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not go up or down a lot, so it has a low beta. An example of the second is gold. The price of gold does go up and down a lot, but not in the same direction or at the same time as the market.A beta greater than one generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like equity put options can have large negative betas.Beta is important because it measures the risk of an investment that cannot be reduced by diversification. It does not measure the risk of an investment held on a stand-alone basis, but the amount of risk the investment adds to an already-diversified portfolio. In the capital asset pricing model, beta risk is the only kind of risk for which investors should receive an expected return higher than the risk-free rate of interest.The definition above covers only theoretical beta. The term is used in many related ways in finance. For example, the betas commonly quoted in mutual fund analyses generally measure the risk of the fund arising from exposure to a benchmark for the fund, rather than from exposure to the entire market portfolio. Thus they measure the amount of risk the fund adds to a diversified portfolio of funds of the same type, rather than to a portfolio diversified among all fund types.Beta decay refers to the tendency for a company with a high beta coefficient (β > 1) to have its beta coefficient decline to the market beta. It is an example of regression toward the mean.