Short Duration Income Y Share Fund Fact Sheet

... sensitive the fund is to shifts in interest rates. Standard deviation measures how widely a set of values varies from the mean. It is a historical measure of the variability of return earned by an investment portfolio over a 3-year period. Consider these risks before investing: Putnam Short Duration ...

... sensitive the fund is to shifts in interest rates. Standard deviation measures how widely a set of values varies from the mean. It is a historical measure of the variability of return earned by an investment portfolio over a 3-year period. Consider these risks before investing: Putnam Short Duration ...

How predictable is the future?

... unusually strong or weak outcomes into perpetuity). Those of us believing in long term regression to the mean have found elements of the recent market environment challenging. As we have consistently bemoaned, central bankers, politicians and regulators have been assiduously aiming to prevent the pr ...

... unusually strong or weak outcomes into perpetuity). Those of us believing in long term regression to the mean have found elements of the recent market environment challenging. As we have consistently bemoaned, central bankers, politicians and regulators have been assiduously aiming to prevent the pr ...

Evaluating the Dynamic Nature of Market Risk by Todd Hubbs, Todd

... agricultural risk. Some of these factors, many of which are economy wide shocks, are virtually by definition not constant over time. It is important for entities operating within the agricultural sector to identify, assess, and monitor risks linked to commodities over time. Such understanding of th ...

... agricultural risk. Some of these factors, many of which are economy wide shocks, are virtually by definition not constant over time. It is important for entities operating within the agricultural sector to identify, assess, and monitor risks linked to commodities over time. Such understanding of th ...

Risk Management - Spears School of Business

... • Unlike return, variance of a portfolio is also related to correlations. So if these correlations different from ONE, then there can be some risk saving! ...

... • Unlike return, variance of a portfolio is also related to correlations. So if these correlations different from ONE, then there can be some risk saving! ...

Extending Factor Models of Equity Risk to Credit Risk, Default Correlation, and Corporate Sustainability

... th t cause higher equity valuations We propose “revenue weighted” expected average life as a measure of systemic stress on an economy By revenue weighting we capture the stress in the real economy Avoids bias of cap weighting since failing firm’s have small market capitalization and don’t count as m ...

... th t cause higher equity valuations We propose “revenue weighted” expected average life as a measure of systemic stress on an economy By revenue weighting we capture the stress in the real economy Avoids bias of cap weighting since failing firm’s have small market capitalization and don’t count as m ...

- Liontrust

... 3. Long-term capital growth that is at least in line with inflation Your investment should provide a good and increasing level of income in real terms while also preserving the value of your capital over time. If a fund can consistently deliver these objectives over the long term, there is a good ch ...

... 3. Long-term capital growth that is at least in line with inflation Your investment should provide a good and increasing level of income in real terms while also preserving the value of your capital over time. If a fund can consistently deliver these objectives over the long term, there is a good ch ...

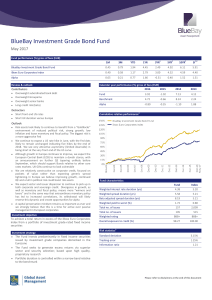

BlueBay Investment Grade Bond Fund

... Returns for periods of less than 1 year have not been annualised in accordance with current industry standard reporting practices. 4. The Fund AUM is stated on a T+1 basis and includes non-fee earning assets. 5. CDS long exposure means sold protection and CDS short exposure means brought protection. ...

... Returns for periods of less than 1 year have not been annualised in accordance with current industry standard reporting practices. 4. The Fund AUM is stated on a T+1 basis and includes non-fee earning assets. 5. CDS long exposure means sold protection and CDS short exposure means brought protection. ...

Lecture 02 - Basics of Investing I

... – Aggregate value of combining several stocks together and intended to represent entire or portion of the stock market ...

... – Aggregate value of combining several stocks together and intended to represent entire or portion of the stock market ...

Vanguard Energy Index Fund

... Connect with Vanguard ® > vanguard.com Plain talk about risk An investment in the fund could lose money over short or even long periods. You should expect the fund’s share price and total return to fluctuate within a wide range, like the fluctuations of the overall stock market. The fund’s performan ...

... Connect with Vanguard ® > vanguard.com Plain talk about risk An investment in the fund could lose money over short or even long periods. You should expect the fund’s share price and total return to fluctuate within a wide range, like the fluctuations of the overall stock market. The fund’s performan ...

estimating systematic risk: the choice of return

... estimate the WACC, the financial manager must calculate the after-tax cost of debt, the cost of preferred stock, and the cost of equity. The most difficult component to calculate is the cost of equity. One method to calculate the cost of equity is the Capital Asset Pricing Model (CAPM), which is exa ...

... estimate the WACC, the financial manager must calculate the after-tax cost of debt, the cost of preferred stock, and the cost of equity. The most difficult component to calculate is the cost of equity. One method to calculate the cost of equity is the Capital Asset Pricing Model (CAPM), which is exa ...

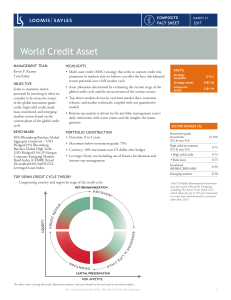

The Wrong 20

... • Cheap (expensive) stocks tend to have surprisingly high (low) realized returns • Cheap (expensive) stocks tend to have low (high) volatility, because little (much) is expected of them • Investors may expect higher returns from expensive stocks but they may be repeatedly surprised by disappointing ...

... • Cheap (expensive) stocks tend to have surprisingly high (low) realized returns • Cheap (expensive) stocks tend to have low (high) volatility, because little (much) is expected of them • Investors may expect higher returns from expensive stocks but they may be repeatedly surprised by disappointing ...

IPKW - PowerShares International BuyBack Achievers Portfolio fact

... that lessens the impact of large outliers and increases the impact of small ones. Weighted Average Return on Equity is net income divided by net worth.Weighted Market Capitalization is the sum of each underlying securities’ market value. The 30-Day SEC Yield is based on a 30-day period and is comput ...

... that lessens the impact of large outliers and increases the impact of small ones. Weighted Average Return on Equity is net income divided by net worth.Weighted Market Capitalization is the sum of each underlying securities’ market value. The 30-Day SEC Yield is based on a 30-day period and is comput ...

Equity Risk, Credit Risk, Default Correlation, and Corporate Sustainability

... • Low equity valuations and high leverage equate to short life expectancy – Higher leverage can be sustained with higher growth rates that cause higher equity valuations We propose “revenue weighted” expected average life as a measure of systemic stress on an economy – By revenue weighting we captur ...

... • Low equity valuations and high leverage equate to short life expectancy – Higher leverage can be sustained with higher growth rates that cause higher equity valuations We propose “revenue weighted” expected average life as a measure of systemic stress on an economy – By revenue weighting we captur ...

Everything You Wanted to Know about Asset Management for

... Relate changes in expected life to subsequent rating changes Relate expected life values that are outliers within their rating category to subsequent rating changes Adjust credit risk expectations for bond issuers and financial counterparties in our fixed income risk model ...

... Relate changes in expected life to subsequent rating changes Relate expected life values that are outliers within their rating category to subsequent rating changes Adjust credit risk expectations for bond issuers and financial counterparties in our fixed income risk model ...

Extending Factor Models of Equity Risk to Credit Risk and Default Correlation

... Obviously, if the market thinks public companies are not going to be around very long, the economy is in a bad way ...

... Obviously, if the market thinks public companies are not going to be around very long, the economy is in a bad way ...

Harbor Mid Cap Value Fund

... Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which ...

... Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which ...

Strategy RIsk and the Central Paradox for Active Management

... “tracking error”, which describes the expectation of times-series standard deviation of benchmark relative returns. This is useful for index fund management, where the expectation of the mean for benchmark relative return is fixed at zero. The active management case is problematic, as tracking error ...

... “tracking error”, which describes the expectation of times-series standard deviation of benchmark relative returns. This is useful for index fund management, where the expectation of the mean for benchmark relative return is fixed at zero. The active management case is problematic, as tracking error ...

1. You were hired as a consultant to Keys Company, and you were

... Things will generally even out over time, and, therefore, the firm’s risk should remain constant over time. d. The company’s overall WACC should decrease over time because its stock price should be increasing. e. The CEO’s recommendation would maximize the firm’s intrinsic value. The company will ta ...

... Things will generally even out over time, and, therefore, the firm’s risk should remain constant over time. d. The company’s overall WACC should decrease over time because its stock price should be increasing. e. The CEO’s recommendation would maximize the firm’s intrinsic value. The company will ta ...

intermediate-financial-management-10th-edition

... the market risk of a stock (beta), and it specifies the relationship between risk as measured by beta and the required rate of return on a stock. Its principal developers (Sharpe and Markowitz) won the Nobel Prize in 1990 for their work. The key assumptions are spelled out in Chapter 3, but they inc ...

... the market risk of a stock (beta), and it specifies the relationship between risk as measured by beta and the required rate of return on a stock. Its principal developers (Sharpe and Markowitz) won the Nobel Prize in 1990 for their work. The key assumptions are spelled out in Chapter 3, but they inc ...

Ch 24 Perf measurement 2/e

... The IRR (i.e., the dollar-weighted return) can not be ranked relative to either the geometric average return (i.e., the time-weighted return) or the arithmetic average return. Under some conditions, the IRR is greater than each of the other two averages, and similarly, under other conditions, the IR ...

... The IRR (i.e., the dollar-weighted return) can not be ranked relative to either the geometric average return (i.e., the time-weighted return) or the arithmetic average return. Under some conditions, the IRR is greater than each of the other two averages, and similarly, under other conditions, the IR ...

AZIONARIO TREND LUNGO PERIODO (LU0089650302) a Sub

... responsible for awarding the remuneration and benefits, including the composition of the remuneration committee, are available on http://www. mdo-manco.com/remuneration-policy, a paper copy will be made available free of charge upon request. Luxembourg's taxation regime may have an impact on the per ...

... responsible for awarding the remuneration and benefits, including the composition of the remuneration committee, are available on http://www. mdo-manco.com/remuneration-policy, a paper copy will be made available free of charge upon request. Luxembourg's taxation regime may have an impact on the per ...

Download attachment

... If we use the single reinsurance premium method described above, the formula can be written as follows: Mathematical reserve at time interval t ...

... If we use the single reinsurance premium method described above, the formula can be written as follows: Mathematical reserve at time interval t ...

ab large cap growth fund

... 3 Sharpe Ratio is a measure of the fund’s return relative to the investment risk it has taken. A higher Sharpe Ratio means the fund’s returns have been better given the level of risk the fund has taken. 4 Standard Deviation is a measure of the dispersion of a portfolio’s return from its mean. The mo ...

... 3 Sharpe Ratio is a measure of the fund’s return relative to the investment risk it has taken. A higher Sharpe Ratio means the fund’s returns have been better given the level of risk the fund has taken. 4 Standard Deviation is a measure of the dispersion of a portfolio’s return from its mean. The mo ...

Corporate Finance What - Hong Kong Securities and Investment

... – Many of those entering investment banking are young and highly ambitious; they have a work hard, play hard attitude. – Graduates looking to go into corporate finance, debt capital, or equity capital will need to be high academic achievers, capable of processing large amounts of information in a sh ...

... – Many of those entering investment banking are young and highly ambitious; they have a work hard, play hard attitude. – Graduates looking to go into corporate finance, debt capital, or equity capital will need to be high academic achievers, capable of processing large amounts of information in a sh ...

Beta (finance)

In finance, the beta (β) of an investment is a measure of the risk arising from exposure to general market movements as opposed to idiosyncratic factors. The market portfolio of all investable assets has a beta of exactly 1. A beta below 1 can indicate either an investment with lower volatility than the market, or a volatile investment whose price movements are not highly correlated with the market. An example of the first is a treasury bill: the price does not go up or down a lot, so it has a low beta. An example of the second is gold. The price of gold does go up and down a lot, but not in the same direction or at the same time as the market.A beta greater than one generally means that the asset both is volatile and tends to move up and down with the market. An example is a stock in a big technology company. Negative betas are possible for investments that tend to go down when the market goes up, and vice versa. There are few fundamental investments with consistent and significant negative betas, but some derivatives like equity put options can have large negative betas.Beta is important because it measures the risk of an investment that cannot be reduced by diversification. It does not measure the risk of an investment held on a stand-alone basis, but the amount of risk the investment adds to an already-diversified portfolio. In the capital asset pricing model, beta risk is the only kind of risk for which investors should receive an expected return higher than the risk-free rate of interest.The definition above covers only theoretical beta. The term is used in many related ways in finance. For example, the betas commonly quoted in mutual fund analyses generally measure the risk of the fund arising from exposure to a benchmark for the fund, rather than from exposure to the entire market portfolio. Thus they measure the amount of risk the fund adds to a diversified portfolio of funds of the same type, rather than to a portfolio diversified among all fund types.Beta decay refers to the tendency for a company with a high beta coefficient (β > 1) to have its beta coefficient decline to the market beta. It is an example of regression toward the mean.