Value-at-Risk and Extreme Returns

... some cases even infinite. As a result, the highest realizations lead to poor estimates of the tails, which may invalidate HS as a method for stress testing. In addition, it is not possible to do out-of-sample prediction with HS, i.e. predict losses that occur less frequently than are covered by the ...

... some cases even infinite. As a result, the highest realizations lead to poor estimates of the tails, which may invalidate HS as a method for stress testing. In addition, it is not possible to do out-of-sample prediction with HS, i.e. predict losses that occur less frequently than are covered by the ...

The Impact of Costs and Returns on the Investment

... among large Swiss pension funds. Public, corporate, and industry-wide/multiemployer pension funds participated in the survey. The report reveals that portfolio diversification is the main decision criteria for Swiss pension fund managers when structuring their portfolios. The riskreturn-relation is ...

... among large Swiss pension funds. Public, corporate, and industry-wide/multiemployer pension funds participated in the survey. The report reveals that portfolio diversification is the main decision criteria for Swiss pension fund managers when structuring their portfolios. The riskreturn-relation is ...

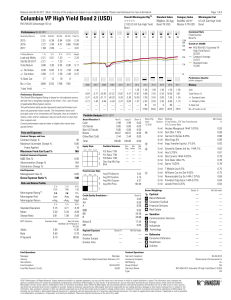

Long-term Capital Market Return Assumptions

... Investors and advisors around the world have come to rely on our assumptions to guide their strategic asset allocation and set realistic expectations for risks and returns over a 10- to 15-year time frame. The assumptions encompass more than 50 asset and strategy classes and are available in 10 base ...

... Investors and advisors around the world have come to rely on our assumptions to guide their strategic asset allocation and set realistic expectations for risks and returns over a 10- to 15-year time frame. The assumptions encompass more than 50 asset and strategy classes and are available in 10 base ...

NBER WORKING PAPER SERIES ASSET LIQUIDITY AND INTERNATIONAL PORTFOLIO CHOICE Athanasios Geromichalos

... home bias, and asset markets are incomplete. However, in this setting, domestic asset flows are also high, thus yielding equally high turnover rates of domestic assets. Unlike the consumption-based models of home bias above, Amadi and Bergin (2008) offer an explanation for the coexistence of asset h ...

... home bias, and asset markets are incomplete. However, in this setting, domestic asset flows are also high, thus yielding equally high turnover rates of domestic assets. Unlike the consumption-based models of home bias above, Amadi and Bergin (2008) offer an explanation for the coexistence of asset h ...

Margin-based Asset Pricing and Deviations from the Law of One Price

... greater than that of a low-margin security with the same cash flows—e.g., proxied by a CDS. This is because of the high shadow cost of capital of the risktolerant investor. When the risk-tolerant investor’s margin constraint binds, he is willing to accept a lower yield spread on a CDS, since it uses ...

... greater than that of a low-margin security with the same cash flows—e.g., proxied by a CDS. This is because of the high shadow cost of capital of the risktolerant investor. When the risk-tolerant investor’s margin constraint binds, he is willing to accept a lower yield spread on a CDS, since it uses ...

Ashmore Emerging Markets Liquid Investment Portfolio Ashmore

... of appreciation following intervention by the People's Bank of China (PBoC). The economy responded positively to targeted monetary easing as the Q2 2014 GDP accelerated from 7.4% to 7.5%. The PBoC announced a further CNY 1trn in collateralised credit lines for priority sectors, to be supplied via th ...

... of appreciation following intervention by the People's Bank of China (PBoC). The economy responded positively to targeted monetary easing as the Q2 2014 GDP accelerated from 7.4% to 7.5%. The PBoC announced a further CNY 1trn in collateralised credit lines for priority sectors, to be supplied via th ...

An Empirical Assessment of Models of the Value Premium*

... Cooper (2006) makes the same link between profitability and B/M. If a firm has been hit by adverse profitability shocks, this firm’s B/M ratio is high because its market value falls while its book value remains fairly constant due to irreversibility. Such a firm is sensitive to aggregate shocks, an ...

... Cooper (2006) makes the same link between profitability and B/M. If a firm has been hit by adverse profitability shocks, this firm’s B/M ratio is high because its market value falls while its book value remains fairly constant due to irreversibility. Such a firm is sensitive to aggregate shocks, an ...

Is 22 a Measure of Market Ineffi ciency?!

... U.S. and a set of international countries including those originally analyzed by MYY. In analyzing the U.S. stock returns, we …rst sort stocks into di¤erent R2 quintiles and then compare the pro…ts from pursuing a momentum strategy within each of the R2 quintiles. The momentum strategy involves buyi ...

... U.S. and a set of international countries including those originally analyzed by MYY. In analyzing the U.S. stock returns, we …rst sort stocks into di¤erent R2 quintiles and then compare the pro…ts from pursuing a momentum strategy within each of the R2 quintiles. The momentum strategy involves buyi ...

Endogenous risk in a DSGE model with capital-constrained …nancial intermediaries Hans Dewachter

... describe the …nancial and real decisions of the various economic agents within the context of occasionallybinding constraints that separate distressed states from normal times. This global solution procedure imposes in practice, however, strong limitations on the size of the state vector; in most ca ...

... describe the …nancial and real decisions of the various economic agents within the context of occasionallybinding constraints that separate distressed states from normal times. This global solution procedure imposes in practice, however, strong limitations on the size of the state vector; in most ca ...

duration gap in the context of a bank`s strategic

... rates. Duration matching represents a powerful tool in minimizing the risk of changing interest rates. It is an important tool utilized by the decision-makers in risk management issues. However, currently there are many illustrations that provide overly simplified definitions of portfolio duration a ...

... rates. Duration matching represents a powerful tool in minimizing the risk of changing interest rates. It is an important tool utilized by the decision-makers in risk management issues. However, currently there are many illustrations that provide overly simplified definitions of portfolio duration a ...

Teaching Spreadsheet Simulation

... students to learn and be able to do, after your class is over; in other classes, internships, future jobs? How can simulation coverage help accomplish these goals? Cases: Engage students in the business problem, let them discover relevance of simulation. Student-Developed Projects: Students gain bet ...

... students to learn and be able to do, after your class is over; in other classes, internships, future jobs? How can simulation coverage help accomplish these goals? Cases: Engage students in the business problem, let them discover relevance of simulation. Student-Developed Projects: Students gain bet ...

The Clustering of Extreme Movements: Stock Prices

... enough) to permit an investor to make abnormal returns after paying transactions costs. Therefore, the evidence against the random walk hypothesis is not inconsistent with the practical implications of EMH. Another predictable pattern in the behavior of stock prices is the subject of this paper. Wor ...

... enough) to permit an investor to make abnormal returns after paying transactions costs. Therefore, the evidence against the random walk hypothesis is not inconsistent with the practical implications of EMH. Another predictable pattern in the behavior of stock prices is the subject of this paper. Wor ...

ESSAYS ON DETERMINANTS OF FINANCIAL BEHAVIOR OF

... This thesis investigates the role of individual-specific factors in individuals’ financial behavior. The main focus of the analysis is on two characteristics of individuals: risk attitude and gender. Although these two factors are believed to be important determinants of financial behavior, a review ...

... This thesis investigates the role of individual-specific factors in individuals’ financial behavior. The main focus of the analysis is on two characteristics of individuals: risk attitude and gender. Although these two factors are believed to be important determinants of financial behavior, a review ...

JOIM - CSInvesting

... We investigate the pricing of …nancially distressed stocks in two steps: First, we present a model predicting …nancial distress. Second, we consider the historical performance of investing in distressed stock portfolios. Our proposed measure of …nancial distress is the probability of failure. Follow ...

... We investigate the pricing of …nancially distressed stocks in two steps: First, we present a model predicting …nancial distress. Second, we consider the historical performance of investing in distressed stock portfolios. Our proposed measure of …nancial distress is the probability of failure. Follow ...

Client Investing Guide

... Part of conducting a suitability assessment involves assessing the degree to which you are financially able to bear investment risk, consistent with your objectives. In other words, assessing the extent to which a decline in the value of your portfolio would have a detrimental effect on your standar ...

... Part of conducting a suitability assessment involves assessing the degree to which you are financially able to bear investment risk, consistent with your objectives. In other words, assessing the extent to which a decline in the value of your portfolio would have a detrimental effect on your standar ...

informe de política monetaria

... indicator be included in monetary policy models? In particular, should it be explicitly included in the reaction function? Or, should the central bank react only indirectly through reacting to its effects on inflation and output gap? ...

... indicator be included in monetary policy models? In particular, should it be explicitly included in the reaction function? Or, should the central bank react only indirectly through reacting to its effects on inflation and output gap? ...