What are Wants and Needs?

... A market economy is market in which buyers and sellers come together to answer the three economic questions. The United States is an example of a market economy. They answer the three economic questions by observing supply and demand. Supply is when sellers determine how much of a particular good or ...

... A market economy is market in which buyers and sellers come together to answer the three economic questions. The United States is an example of a market economy. They answer the three economic questions by observing supply and demand. Supply is when sellers determine how much of a particular good or ...

4. The model of Perfect Competition

... Price at which products are sold Quantity of products sold Profit levels Economic efficiency ...

... Price at which products are sold Quantity of products sold Profit levels Economic efficiency ...

Supply and Demand Notes combined File

... • Create your own supply and demand curve. Be sure to label each as D1 and S1. Label your equilibrium as E1. From there show a scenario where there would be an increase in demand. Label your new demand as D2 and your new equilibrium as E2. From there show an increase in supply. Label the new supply ...

... • Create your own supply and demand curve. Be sure to label each as D1 and S1. Label your equilibrium as E1. From there show a scenario where there would be an increase in demand. Label your new demand as D2 and your new equilibrium as E2. From there show an increase in supply. Label the new supply ...

Aim: What is the law of supply and demand?

... Aim: What is the law of supply and demand? Do Now: Handout ...

... Aim: What is the law of supply and demand? Do Now: Handout ...

Short Response Questions

... an increase in the supply of fresh strawberries in the northern areas of the United States in the warmer months when the berries are harvested in the northern areas. This causes a rightward shift in the supply curve and causes the price to fall and the quantity sold to ...

... an increase in the supply of fresh strawberries in the northern areas of the United States in the warmer months when the berries are harvested in the northern areas. This causes a rightward shift in the supply curve and causes the price to fall and the quantity sold to ...

Econ 101: Microeconomics

... and Kuwait A significant decrease in the oil industry’s productive capacity caused a shift in the supply curve to the left ...

... and Kuwait A significant decrease in the oil industry’s productive capacity caused a shift in the supply curve to the left ...

1 - Wku

... DVD players demanded and supplied be? What is happening as a result of this price ceiling? c. Explain what will happen if the price ceiling is abolished. Be specific. What will happen to the quantity of DVD players demanded and supplied? To the price of DVD players? Why? d. Graph the supply and dema ...

... DVD players demanded and supplied be? What is happening as a result of this price ceiling? c. Explain what will happen if the price ceiling is abolished. Be specific. What will happen to the quantity of DVD players demanded and supplied? To the price of DVD players? Why? d. Graph the supply and dema ...

Markets: Supply & Demand I - University of Wisconsin

... Let’s Graph it University of Wisconsin-Eau Claire ...

... Let’s Graph it University of Wisconsin-Eau Claire ...

Midterm 2

... Using the table above, and assuming that the market price is $4 and that $1 equal 1 util, answer the following (24 points): A. B. C. D. ...

... Using the table above, and assuming that the market price is $4 and that $1 equal 1 util, answer the following (24 points): A. B. C. D. ...

Basic Economic Concepts Review of Key Concepts, Skills and Graphs

... 6. A production possibilities curve can be used to illustrate scarcity, choice, and opportunity cost graphically. 7. The production possibilities curve represents the point at which an economy is most efficiently producing. 8. Points A, B, and C represent efficient use of resources. 9. Point x repre ...

... 6. A production possibilities curve can be used to illustrate scarcity, choice, and opportunity cost graphically. 7. The production possibilities curve represents the point at which an economy is most efficiently producing. 8. Points A, B, and C represent efficient use of resources. 9. Point x repre ...

Economic equilibrium

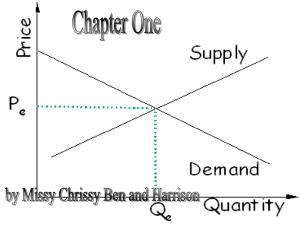

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.