The Art and Science of Economics

... At a price of $4, you demand 4 Subways, Brittany 2, and Chris none: the market demand at a price of $4 equals 6 When the price is $2, your quantity demanded is 6, Brittany’s is 4, and Chris’s is 2: market demand = 12 The market demand shows the total quantity demanded per period by all consumers ...

... At a price of $4, you demand 4 Subways, Brittany 2, and Chris none: the market demand at a price of $4 equals 6 When the price is $2, your quantity demanded is 6, Brittany’s is 4, and Chris’s is 2: market demand = 12 The market demand shows the total quantity demanded per period by all consumers ...

Developing a Marketing Plan

... Observations: Recording the actions of consumers rather than ask them questions ...

... Observations: Recording the actions of consumers rather than ask them questions ...

ECONOMICS

... When a firm’s average-total-cost curve continually declines, the firm has what is called a natural monopoly. In this case, when production is divided among more firms, each firm produces less, and average total cost rises. As a result, a single firm can produce any given amount at the least cost © 2 ...

... When a firm’s average-total-cost curve continually declines, the firm has what is called a natural monopoly. In this case, when production is divided among more firms, each firm produces less, and average total cost rises. As a result, a single firm can produce any given amount at the least cost © 2 ...

McGraw-Hill/Irwin - Cal State LA

... Selling price - Variable cost B.E. in units x Selling price ...

... Selling price - Variable cost B.E. in units x Selling price ...

Perfect Competition

... The perfectly competitive firm is said to be a price-taker, because it takes the market price as given and has no control over the price. Why?... ...

... The perfectly competitive firm is said to be a price-taker, because it takes the market price as given and has no control over the price. Why?... ...

Supply and Demand PowerPoint - Iredell

... – As price falls, quantity supplied falls – Quantity demanded and price move in same direction – P ...

... – As price falls, quantity supplied falls – Quantity demanded and price move in same direction – P ...

Ch05 my ppt

... The benefit of an activity equals the highest price we’d be willing to pay to pursue it (i.e., the reservation price). As the cost of an activity rises and exceeds the reservation price, less of the activity will be pursued. ...

... The benefit of an activity equals the highest price we’d be willing to pay to pursue it (i.e., the reservation price). As the cost of an activity rises and exceeds the reservation price, less of the activity will be pursued. ...

SWOT Analysis

... good at (has competitive advantage in). It may be a characteristic that gives it enhanced competitiveness. ...

... good at (has competitive advantage in). It may be a characteristic that gives it enhanced competitiveness. ...

An Overview of Marketing - Appalachian State University

... Pure subsistence economy - each family produces everything it consumes and no marketing exchanges take place. What is a market? A market is a group of sellers and buyers who get together to exchange goods and services for something of value. Middlemen aid in this exchange process by increasing conta ...

... Pure subsistence economy - each family produces everything it consumes and no marketing exchanges take place. What is a market? A market is a group of sellers and buyers who get together to exchange goods and services for something of value. Middlemen aid in this exchange process by increasing conta ...

See graph - personal.kent.edu

... Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and .60 of it goes to the government in tax), a decrease of $0.20. Since consumer price chang ...

... Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and .60 of it goes to the government in tax), a decrease of $0.20. Since consumer price chang ...

CHAPTER

... The price-leadership strategy prevails in oligopolistic situations and is the practice by which one or a very few firms initiate price changes, with one or more of the other firms in the industry following suit. Price leadership is found most often in industries where products are similar; therefore ...

... The price-leadership strategy prevails in oligopolistic situations and is the practice by which one or a very few firms initiate price changes, with one or more of the other firms in the industry following suit. Price leadership is found most often in industries where products are similar; therefore ...

Five Generic Competitive Strategies

... somewhat subtle to the untrained eye. Admittedly, there is some degree of overlap. However, they are significant in strategic planning as they relate to the ability of the organization to gain a competitive advantage. They offer product and brand distinction in terms of price, value, quality, and pe ...

... somewhat subtle to the untrained eye. Admittedly, there is some degree of overlap. However, they are significant in strategic planning as they relate to the ability of the organization to gain a competitive advantage. They offer product and brand distinction in terms of price, value, quality, and pe ...

CASE FAIR OSTER

... In January 2013, a one-way ticket from New York to San Diego, California cost about $500 on one of the major airlines. Alternatively, you could buy a Standby ticket for $50 and wait around JFK airport hoping for a seat to San Diego. Why would an airline offer a $50 seat for this flight? The answer h ...

... In January 2013, a one-way ticket from New York to San Diego, California cost about $500 on one of the major airlines. Alternatively, you could buy a Standby ticket for $50 and wait around JFK airport hoping for a seat to San Diego. Why would an airline offer a $50 seat for this flight? The answer h ...

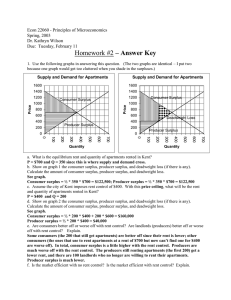

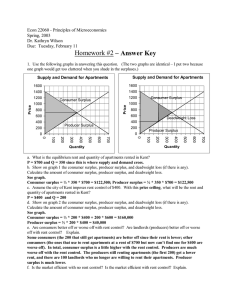

Homework #2 – Answer Key

... Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and .60 of it goes to the government in tax), a decrease of $0.20. Since consumer price chang ...

... Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and .60 of it goes to the government in tax), a decrease of $0.20. Since consumer price chang ...

Demand Curve

... responsive are consumers to an increase or decrease of price?” That responsiveness is ELASTICITY. ...

... responsive are consumers to an increase or decrease of price?” That responsiveness is ELASTICITY. ...