unit eight accounting

... other capital goods. Then these capital goods can help produce more goods in the future. A nation also must locate and develop additional natural resources, create new technologies, train scientists, workers and business managers, who will direct future production. The knowledge of these people is k ...

... other capital goods. Then these capital goods can help produce more goods in the future. A nation also must locate and develop additional natural resources, create new technologies, train scientists, workers and business managers, who will direct future production. The knowledge of these people is k ...

2016 Audit Report - Houston Public Library Foundation

... An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud ...

... An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud ...

Preview Sample File

... foundation of the Conceptual Framework. If we know why we need to report then who needs to report can be determined and then what and how the information is to be reported follow. All the other statements are correct. (Pg 11) *a. The definition of reporting entity forms the foundation of the Concept ...

... foundation of the Conceptual Framework. If we know why we need to report then who needs to report can be determined and then what and how the information is to be reported follow. All the other statements are correct. (Pg 11) *a. The definition of reporting entity forms the foundation of the Concept ...

3 The Balance Sheet and Notes to the Financial

... How? When referring to debt or stock, be careful to note whose instrument it is. (After Chapters 13–15 this should hopefully be clear, but you need to see the distinction now!) If the debt is something the company must repay (including interest), it will be a liability to the company. If the stock i ...

... How? When referring to debt or stock, be careful to note whose instrument it is. (After Chapters 13–15 this should hopefully be clear, but you need to see the distinction now!) If the debt is something the company must repay (including interest), it will be a liability to the company. If the stock i ...

Financial Statements of a Company

... amount paid for them. While, preparing statement of profit and loss the revenue is included in the sales of the year in which the sale was undertaken even though the sale price may be received over a number of years. The assumption is known as realisation postulate. 4. Personal Judgements: Under mor ...

... amount paid for them. While, preparing statement of profit and loss the revenue is included in the sales of the year in which the sale was undertaken even though the sale price may be received over a number of years. The assumption is known as realisation postulate. 4. Personal Judgements: Under mor ...

Line 43a – Other Consulting and Contract

... descriptions is about two. The measures used as examples in the IRS instructions are outputs – clients served, publications issued – not outcomes, typically what is desired in performance reporting. While some government and foundation grantees are required to report on outcomes, the information is ...

... descriptions is about two. The measures used as examples in the IRS instructions are outputs – clients served, publications issued – not outcomes, typically what is desired in performance reporting. While some government and foundation grantees are required to report on outcomes, the information is ...

UNIVERSITY OF THE EAST – CALOOCAN CAMPUS

... This course is a continuation of Financial Accounting & Reporting Part I. It is designed to cover the financial accounting principles relative to recognition, measurement, valuation, and financial statement presentation of liabilities, shareholders’ equity, and special topics (leases, accounting for ...

... This course is a continuation of Financial Accounting & Reporting Part I. It is designed to cover the financial accounting principles relative to recognition, measurement, valuation, and financial statement presentation of liabilities, shareholders’ equity, and special topics (leases, accounting for ...

What Board Members Need to Know About Not-for

... sources, including support received for long-term purposes such as endowment gifts and capital project funding. The three net cash figures, when totaled, represent the change in cash from beginning to the end of the fiscal period represented in the Statement of Activities. When reviewing the Stateme ...

... sources, including support received for long-term purposes such as endowment gifts and capital project funding. The three net cash figures, when totaled, represent the change in cash from beginning to the end of the fiscal period represented in the Statement of Activities. When reviewing the Stateme ...

MANDATORY EMPHASIS PARAGRAPHS, CLARIFYING

... uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant matters that the auditor encounters during the audit within the actual body of audit report will increase the relevance of the audit report. While the Big 4 audit firms agree that the ide ...

... uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant matters that the auditor encounters during the audit within the actual body of audit report will increase the relevance of the audit report. While the Big 4 audit firms agree that the ide ...

Treasurer`s Guide - Methacton School District

... possible, and in accord with licensing criteria. All H/S will be required to report their financial position using a standardized excel file developed by the MCC. Bank Account Management (signature authority) - One bank account is usually sufficient for H/S business. TWO authorizing signatures on ...

... possible, and in accord with licensing criteria. All H/S will be required to report their financial position using a standardized excel file developed by the MCC. Bank Account Management (signature authority) - One bank account is usually sufficient for H/S business. TWO authorizing signatures on ...

What is Accounting?

... IFRS tends to be simpler in its accounting and disclosure requirements; some people say more “principles-based.” GAAP is more detailed; some people say it is more “rules-based.” This difference in approach has resulted in a debate about the merits of “principles-based” versus “rules-based” standards ...

... IFRS tends to be simpler in its accounting and disclosure requirements; some people say more “principles-based.” GAAP is more detailed; some people say it is more “rules-based.” This difference in approach has resulted in a debate about the merits of “principles-based” versus “rules-based” standards ...

Implementation Tool for Auditors

... Once the auditor has concluded that ROMM due to fraud in revenue recognition exists for all or only certain types of revenue and revenue transactions, the auditor is required to treat such risk as a significant risk and accordingly, to the extent not already done so, obtain an understanding of the c ...

... Once the auditor has concluded that ROMM due to fraud in revenue recognition exists for all or only certain types of revenue and revenue transactions, the auditor is required to treat such risk as a significant risk and accordingly, to the extent not already done so, obtain an understanding of the c ...

Internal Control Systems

... of procedures and records established to start, record, process and report entity transactions and maintain accountability for the related assets, liabilities and equity. What are Control Activities? Control activities are those policies and procedures that help ensure that management directives are ...

... of procedures and records established to start, record, process and report entity transactions and maintain accountability for the related assets, liabilities and equity. What are Control Activities? Control activities are those policies and procedures that help ensure that management directives are ...

Exam Name___________________________________ TRUE

... 76) Why is the response time more rapid for the Financial Standards Board (FASB) in the U.S. who issue Statements of Financial Accounting Standards (SFAS) than the CICA AcSB who take as much as two years to bring new Handbook Recommendations to fruition. 77) Compared to financial accounting, what a ...

... 76) Why is the response time more rapid for the Financial Standards Board (FASB) in the U.S. who issue Statements of Financial Accounting Standards (SFAS) than the CICA AcSB who take as much as two years to bring new Handbook Recommendations to fruition. 77) Compared to financial accounting, what a ...

FREE Sample Here

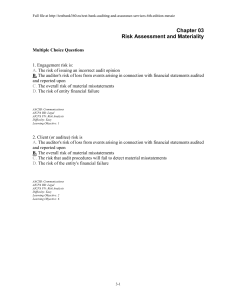

... 28. Which of the following circumstances most likely would cause an auditor to believe that material misstatements may exist in an entity's financial statements? A. Accounts receivable confirmation requests yield significantly fewer responses than expected B. Audit trails of computer-generated trans ...

... 28. Which of the following circumstances most likely would cause an auditor to believe that material misstatements may exist in an entity's financial statements? A. Accounts receivable confirmation requests yield significantly fewer responses than expected B. Audit trails of computer-generated trans ...

FREE Sample Here

... the chapter). Scott criticized the AAA monograph as having a too narrow view of accounting in that it addressed only accounting’s transaction function. Rather, he saw accounting as encompassing other important functions, such as managerial control and the protection of the interests of equity holder ...

... the chapter). Scott criticized the AAA monograph as having a too narrow view of accounting in that it addressed only accounting’s transaction function. Rather, he saw accounting as encompassing other important functions, such as managerial control and the protection of the interests of equity holder ...

Financial Accounting Standards Board (FASB)

... Reporting Standards (IFRS) if issued since 2001, and International Accounting Standards (IAS) if issued prior to 2001. In 2008 the SEC began allowing non-U.S. companies with shares trading on U.S. stock exchanges to issue their financial reports using IASB standards. (continued) ...

... Reporting Standards (IFRS) if issued since 2001, and International Accounting Standards (IAS) if issued prior to 2001. In 2008 the SEC began allowing non-U.S. companies with shares trading on U.S. stock exchanges to issue their financial reports using IASB standards. (continued) ...

Norwood Office Supplies (NOS) Case AC 432 – DeZoort Fall 2004

... file’s data. Exceptions may indicate the failure of a control. For example, an auditor may test a file of disbursements to determine whether all disbursements were allocated to appropriate cost centers. In this project, you will use ACL to perform tests on a client’s files to determine indirectly th ...

... file’s data. Exceptions may indicate the failure of a control. For example, an auditor may test a file of disbursements to determine whether all disbursements were allocated to appropriate cost centers. In this project, you will use ACL to perform tests on a client’s files to determine indirectly th ...

Chapter Twelve - Dr.Mahmood Asad

... a businessperson you will constantly be dealing in numbers. Thus, some basic information on how businesspeople can use accounting to better understand and control their businesses will be discussed. ...

... a businessperson you will constantly be dealing in numbers. Thus, some basic information on how businesspeople can use accounting to better understand and control their businesses will be discussed. ...

THE VALUE RELEVANCE OF MANAGERS` AND

... The PCAOB currently proposes that auditors communicate second-order information from auditors about material measurement uncertainty as critical auditing matters (hereafter, CAudMs) in audit reports (PCAOB 2016). When material measurement uncertainty exists, auditors can only obtain assurance over a ...

... The PCAOB currently proposes that auditors communicate second-order information from auditors about material measurement uncertainty as critical auditing matters (hereafter, CAudMs) in audit reports (PCAOB 2016). When material measurement uncertainty exists, auditors can only obtain assurance over a ...

draft examples of other notes disclosures

... by management based on the financial reporting provisions described in note 1 to the consolidated financial statements. Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements ...

... by management based on the financial reporting provisions described in note 1 to the consolidated financial statements. Management's Responsibility for the Consolidated Financial Statements Management is responsible for the preparation and fair presentation of these consolidated financial statements ...

Double-Entry Accounting

... accountants create individual T accounts to clarify the financial standing of the business. Some of these accounts include: Depreciation is a method of allocating the cost of a fixed asset over the useful life of the asset. Once fully depreciated, the value of the asset at the end of its useful li ...

... accountants create individual T accounts to clarify the financial standing of the business. Some of these accounts include: Depreciation is a method of allocating the cost of a fixed asset over the useful life of the asset. Once fully depreciated, the value of the asset at the end of its useful li ...

Accounting Theory Defined

... Identifies the economic resources (assets), the claims to those resources (liabilities), and the changes in those resources and ...

... Identifies the economic resources (assets), the claims to those resources (liabilities), and the changes in those resources and ...

Financial Instruments with Characteristics of Equity The ABI`s

... respectively, this will mean that the impact on the entity’s net income and performance will ultimately depend on the value of the instrument at the date of exercise or conversion even though these events might long have been certain to occur. Making the accounting depend on the arbitrary choice of ...

... respectively, this will mean that the impact on the entity’s net income and performance will ultimately depend on the value of the instrument at the date of exercise or conversion even though these events might long have been certain to occur. Making the accounting depend on the arbitrary choice of ...