Document

... A non-commission and scalable team-profit share model At the very core of the Group’s culture is our team-based profit-share model which means that unlike the majority of our competition we do not pay individual commission. This team-based profit-share approach ensures the needs of our clients and c ...

... A non-commission and scalable team-profit share model At the very core of the Group’s culture is our team-based profit-share model which means that unlike the majority of our competition we do not pay individual commission. This team-based profit-share approach ensures the needs of our clients and c ...

Do 3 - Together We Pass

... Describe the internal control measures which are normally incorporated in the use of cash registers for handling cash sales. 1. Internal control measures that normally exist when cash registers are used in the handling of cash sales (1) Cash registers must display the amount of the cash sales on a s ...

... Describe the internal control measures which are normally incorporated in the use of cash registers for handling cash sales. 1. Internal control measures that normally exist when cash registers are used in the handling of cash sales (1) Cash registers must display the amount of the cash sales on a s ...

chap.3 - HCC Learning Web

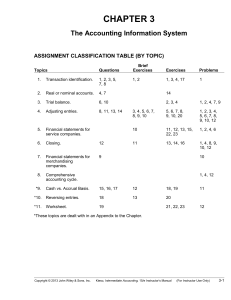

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

Leading Practice Examples of Audit Committee Reporting

... • Relative to domestic operations, the international business offices are small, with a staff of … Due to the cultural differences, country-specific regulations, and distance between international locations and corporate headquarters, the inherent risk level is increased. Audit Summary This review f ...

... • Relative to domestic operations, the international business offices are small, with a staff of … Due to the cultural differences, country-specific regulations, and distance between international locations and corporate headquarters, the inherent risk level is increased. Audit Summary This review f ...

PowerPoints Chapter 06

... – The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders and other creditors in making decisions in their capacity as capital providers. Information that is decisionuseful t ...

... – The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to present and potential equity investors, lenders and other creditors in making decisions in their capacity as capital providers. Information that is decisionuseful t ...

Download attachment

... GAAP. These different financial reporting frameworks in Canadian GAAP are identified in the CICA Handbook – Accounting as follows: • Part I — International Financial Reporting Standards (IFRSs) • Part II — Accounting standards for private enterprises • Part III — Accounting standards for not- ...

... GAAP. These different financial reporting frameworks in Canadian GAAP are identified in the CICA Handbook – Accounting as follows: • Part I — International Financial Reporting Standards (IFRSs) • Part II — Accounting standards for private enterprises • Part III — Accounting standards for not- ...

Guide to Certifications

... internal auditor (CIA), certified fraud examiner (CFE), certified information systems auditor (CISA), certified management accountant (CMA) and chartered accountant (CA) designations. Professional associations continue to create additional specialty certifications to help their members address the i ...

... internal auditor (CIA), certified fraud examiner (CFE), certified information systems auditor (CISA), certified management accountant (CMA) and chartered accountant (CA) designations. Professional associations continue to create additional specialty certifications to help their members address the i ...

(revised) compilation engagements

... a reported item in the financial information, and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. Where the financial information is prepared in a ...

... a reported item in the financial information, and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. Where the financial information is prepared in a ...

Free Sample

... A. Financial statements report quantitative economic information; they do not reflect qualitative economic variables. B. The cost principle requires assets to be recorded at their original cost; thus, the balance sheet does not generally reflect the fair values of most assets and liabilities. C. Net ...

... A. Financial statements report quantitative economic information; they do not reflect qualitative economic variables. B. The cost principle requires assets to be recorded at their original cost; thus, the balance sheet does not generally reflect the fair values of most assets and liabilities. C. Net ...

Yes, there is a big Difference between Audit on Profit Organizations

... verification of facts to ascertain that the cost of the product has been arrived at, in accordance with principles of cost accounting." An audit must adhere to generally accepted standards established by governing bodies. These standards assure third parties or external users that ...

... verification of facts to ascertain that the cost of the product has been arrived at, in accordance with principles of cost accounting." An audit must adhere to generally accepted standards established by governing bodies. These standards assure third parties or external users that ...

The Effect of Audit Firm Specialization on Earnings Management

... one determinant of audit quality (Gramling and Stone, 2001). So, it is necessary to study the role of industry specialization in improving audit quality to help the audit firms in applying industry specialization strategy. In addition, there is a growing emphasis in worldwide professional auditing s ...

... one determinant of audit quality (Gramling and Stone, 2001). So, it is necessary to study the role of industry specialization in improving audit quality to help the audit firms in applying industry specialization strategy. In addition, there is a growing emphasis in worldwide professional auditing s ...

annual report 2016

... supplier awareness and drawing attention to their Ovis status. The ongoing decline in prevalence reflects the commitment of suppliers to maintaining downward pressure on sheep measles at farm level. In addition, the support of processors in increasing the quality of data provided either specifically ...

... supplier awareness and drawing attention to their Ovis status. The ongoing decline in prevalence reflects the commitment of suppliers to maintaining downward pressure on sheep measles at farm level. In addition, the support of processors in increasing the quality of data provided either specifically ...

Staff Guidance for Auditors of SEC-Registered Brokers and

... Board, but they may be helpful to auditors in applying the standards of the PCAOB. They are available on the PCAOB website. ...

... Board, but they may be helpful to auditors in applying the standards of the PCAOB. They are available on the PCAOB website. ...

ActionAid International Financial Management Framework

... planned expenditure for the following year. Any plans showing reserves of more than one third of the following year‟s spend should only be approved in exceptional circumstances. Country Programmes whose committed giving income is less than 20% of their total income are exempt from this policy; their ...

... planned expenditure for the following year. Any plans showing reserves of more than one third of the following year‟s spend should only be approved in exceptional circumstances. Country Programmes whose committed giving income is less than 20% of their total income are exempt from this policy; their ...

Western Kentucky University Accountants’ Report and Financial Statements

... We have audited the accompanying basic financial statements of Western Kentucky University, a component unit of the Commonwealth of Kentucky, as of and for the years ended June 30, 2003 and 2002, as listed in the table of contents. These financial statements are the responsibility of the University’ ...

... We have audited the accompanying basic financial statements of Western Kentucky University, a component unit of the Commonwealth of Kentucky, as of and for the years ended June 30, 2003 and 2002, as listed in the table of contents. These financial statements are the responsibility of the University’ ...

Annual Audit - Atlantic City Municipal Utilities Authority

... 2014. The increase amounted to $302,489 and resulted primarily from an increase in Accounts Receivable. The increase in Accounts Receivable was primarily due to an unpaid balance of the City of Atlantic City amounting to approximately $240,000. Total Restricted Assets- Total Restricted Assets for 20 ...

... 2014. The increase amounted to $302,489 and resulted primarily from an increase in Accounts Receivable. The increase in Accounts Receivable was primarily due to an unpaid balance of the City of Atlantic City amounting to approximately $240,000. Total Restricted Assets- Total Restricted Assets for 20 ...

Notification 297/2015 dated 28th December, 2015 - Regarding the Internal Audit Manual (672 KB)

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

The Auditor`s Responsibility to Detect Fraud

... ACFE estimate that this 5 percent figure would translate to approximately $2.9 trillion as applied to the estimated 2009 gross world product (Crawford and Weirich, 2011). For instance, almost daily one can read about organisations that have been exploited in both the private and public sectors resu ...

... ACFE estimate that this 5 percent figure would translate to approximately $2.9 trillion as applied to the estimated 2009 gross world product (Crawford and Weirich, 2011). For instance, almost daily one can read about organisations that have been exploited in both the private and public sectors resu ...

Acc Plus Aut09

... their useful lives or amortisation rates used; (b) the amortisation methods adopted; (c) the gross carrying amount and accumulated amortisation at the start and end of the period; (d) the line item of the income statement in which the amortisation charge is included; (e) a reconciliation of the carr ...

... their useful lives or amortisation rates used; (b) the amortisation methods adopted; (c) the gross carrying amount and accumulated amortisation at the start and end of the period; (d) the line item of the income statement in which the amortisation charge is included; (e) a reconciliation of the carr ...

CHAPTER 1 – Principles of Accounting

... A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted accounting principles, and (b) to deter ...

... A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted accounting principles, and (b) to deter ...

public finance management act no. 1 of 1999

... 2. Object of this Act.— The object of this Act is to secure transparency, accountability, and sound management of the revenue, expenditure, assets and liabilities of the institutions to which this Act applies. 3. Institutions to which this Act applies.— (1) This Act, to the extent indicated in the A ...

... 2. Object of this Act.— The object of this Act is to secure transparency, accountability, and sound management of the revenue, expenditure, assets and liabilities of the institutions to which this Act applies. 3. Institutions to which this Act applies.— (1) This Act, to the extent indicated in the A ...

Chapter 5 Revenue

... of inventory purchased and sold thus providing a balance at any time. Using the same example of A. Wong, owner of Party Supplies, the following processing would occur for the purchase and sale of party hats. The recording using a perpetual inventory approach has highlighted the incorrect assumption ...

... of inventory purchased and sold thus providing a balance at any time. Using the same example of A. Wong, owner of Party Supplies, the following processing would occur for the purchase and sale of party hats. The recording using a perpetual inventory approach has highlighted the incorrect assumption ...

FASB: Status of Statement 5

... paragraph 8 and of the disclosure requirements in paragraphs 9-11. Some examples have been included in response to questions raised in letters of comment on the Exposure Draft. It should be recognized that no set of examples can encompass all possible contingencies or circumstances. Accordingly, acc ...

... paragraph 8 and of the disclosure requirements in paragraphs 9-11. Some examples have been included in response to questions raised in letters of comment on the Exposure Draft. It should be recognized that no set of examples can encompass all possible contingencies or circumstances. Accordingly, acc ...

FASB: Status of Statement 5

... paragraph 8 and of the disclosure requirements in paragraphs 9-11. Some examples have been included in response to questions raised in letters of comment on the Exposure Draft. It should be recognized that no set of examples can encompass all possible contingencies or circumstances. Accordingly, acc ...

... paragraph 8 and of the disclosure requirements in paragraphs 9-11. Some examples have been included in response to questions raised in letters of comment on the Exposure Draft. It should be recognized that no set of examples can encompass all possible contingencies or circumstances. Accordingly, acc ...

GAAP

... Moreover, the subjective judgments of senior management, accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could ...

... Moreover, the subjective judgments of senior management, accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could ...