Sample Study Guide - McGraw Hill Higher Education

... information is supported by unbiased evidence: more than someone's opinion. b. Revenue recognition principle—revenue is recognized (recorded) when earned. Proceeds need not be in cash. Revenue is measured by cash received plus the cash value of other items received. c. Matching principle—a company m ...

... information is supported by unbiased evidence: more than someone's opinion. b. Revenue recognition principle—revenue is recognized (recorded) when earned. Proceeds need not be in cash. Revenue is measured by cash received plus the cash value of other items received. c. Matching principle—a company m ...

Revised Guidance Statement GS 009: Auditing SMSFs

... Auditors of APRA regulated superannuation entities, particularly auditors of small APRA funds, may find this Guidance Statement useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under ...

... Auditors of APRA regulated superannuation entities, particularly auditors of small APRA funds, may find this Guidance Statement useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under ...

ASRE 2410 Review of a Financial Report Performed by the Independent Auditor of the Entity. The choice of ASRE 2400

... Auditing Standard on Review Engagements ASRE 2410 Review of a Financial Report Performed by the Independent Auditor of the Entity (as amended at 27 June 2011) is set out in paragraphs 1 to A60 and Appendices 1 to 4. This Auditing Standard on Review Engagements is to be read in conjunction with ASA 1 ...

... Auditing Standard on Review Engagements ASRE 2410 Review of a Financial Report Performed by the Independent Auditor of the Entity (as amended at 27 June 2011) is set out in paragraphs 1 to A60 and Appendices 1 to 4. This Auditing Standard on Review Engagements is to be read in conjunction with ASA 1 ...

ch02_sm_rankin

... should be included on the balance sheet. Also to be complete and so representationally faithful would argue that need to include all elements. Surely information about the assets and liabilities of an entity would be relevant to users. Improves comparability as does not distinguish on form or arb ...

... should be included on the balance sheet. Also to be complete and so representationally faithful would argue that need to include all elements. Surely information about the assets and liabilities of an entity would be relevant to users. Improves comparability as does not distinguish on form or arb ...

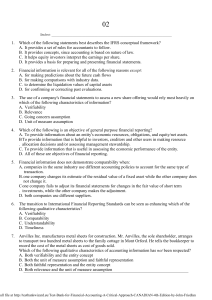

1. Which of the following statements best describes the IFRS

... A. To provide users with easy comparison with the industry. B. To provide users with a perspective on the economy. C. Because making comparisons using accounting information can be difficult and misleading. D. Because making comparisons significantly contributes to the interpretation of accounting i ...

... A. To provide users with easy comparison with the industry. B. To provide users with a perspective on the economy. C. Because making comparisons using accounting information can be difficult and misleading. D. Because making comparisons significantly contributes to the interpretation of accounting i ...

Aue2602 Summary

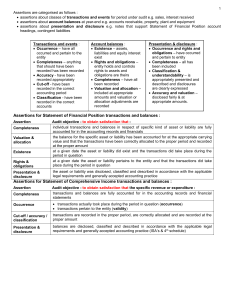

... rights to assets and obligations are theirs Completeness – have all been recorded Valuation and allocation – included at appropriate amounts and valuation or allocation adjustments are recorded ...

... rights to assets and obligations are theirs Completeness – have all been recorded Valuation and allocation – included at appropriate amounts and valuation or allocation adjustments are recorded ...

FREE Sample Here

... If total liabilities increased by $4000, then Learning Objective 1.10 Analyse the effects of business transactions on the basic accounting equation a. assets must have decreased by $4000. b. owner's equity must have increased by $4000. *c. assets must have increased by $4000, or owner's equity must ...

... If total liabilities increased by $4000, then Learning Objective 1.10 Analyse the effects of business transactions on the basic accounting equation a. assets must have decreased by $4000. b. owner's equity must have increased by $4000. *c. assets must have increased by $4000, or owner's equity must ...

The Impact Of Switching To International Financial Reporting

... Despite the commonness of some of the standards, multinational companies have begun the process of hiring global accountants and lawyers to research tax law, auditing practices, and legal instruments tied to the finances of businesses in countries they are operating in. The impacts of the internatio ...

... Despite the commonness of some of the standards, multinational companies have begun the process of hiring global accountants and lawyers to research tax law, auditing practices, and legal instruments tied to the finances of businesses in countries they are operating in. The impacts of the internatio ...

working program - Almaty Management University

... - to be able to adequately navigate various social situations; Work in team; to defend their positions, and suggest new approaches; Reach compromise, correlate their opinions with the opinions of the team members; Aim or professional and personal development; Use information technologies in their pr ...

... - to be able to adequately navigate various social situations; Work in team; to defend their positions, and suggest new approaches; Reach compromise, correlate their opinions with the opinions of the team members; Aim or professional and personal development; Use information technologies in their pr ...

6. Compliance audit of a real estate agent`s trust

... The nature, timing and extent of audit procedures will vary, depending on the following factors: • the services provided by the real estate agent and money received on trust as a result of these services; • the nature of the real estate agent’s business, i.e. whether the real estate agent is a sol ...

... The nature, timing and extent of audit procedures will vary, depending on the following factors: • the services provided by the real estate agent and money received on trust as a result of these services; • the nature of the real estate agent’s business, i.e. whether the real estate agent is a sol ...

A GUIDE TO STATUTORY AUDIT PROCEDURES ON EXPECTED

... may result in a high risk of material misstatement (…)”. Section 7 states that “when accounting estimates leave considerable room for judgement, the objectives pursued by the management who could, whether intentionally or otherwise, orient the choice of the assumptions on which these estimates are b ...

... may result in a high risk of material misstatement (…)”. Section 7 states that “when accounting estimates leave considerable room for judgement, the objectives pursued by the management who could, whether intentionally or otherwise, orient the choice of the assumptions on which these estimates are b ...

ACCOUNTING AND AUDITING LAW OF

... cash flows, changes in equity, and other financial and non-financial information that are of importance for external and internal users of financial reports, b) bookkeeping is a system that includes collecting, classification, records keeping and recapitulation of business transactions, as well as s ...

... cash flows, changes in equity, and other financial and non-financial information that are of importance for external and internal users of financial reports, b) bookkeeping is a system that includes collecting, classification, records keeping and recapitulation of business transactions, as well as s ...

What is Accounting? - masif-emba-fais-s12

... The Building Blocks of Accounting Cost Principle (Historical) – dictates that companies record assets at their cost. Issues: Reported at cost when purchased and also over the time the asset is held. Cost easily verified, whereas market value is often subjective. ...

... The Building Blocks of Accounting Cost Principle (Historical) – dictates that companies record assets at their cost. Issues: Reported at cost when purchased and also over the time the asset is held. Cost easily verified, whereas market value is often subjective. ...

The purposes of accounting

... accounting treatment available • Conforming to GAAP/IFRS does not mean that the information provided is good, but it is the start ...

... accounting treatment available • Conforming to GAAP/IFRS does not mean that the information provided is good, but it is the start ...

Guide to New Canadian Independence Standard

... engagement needs to be evaluated in reaching conclusions in the particular assurance engagement. Circumstances that may create a self-review threat include there being a person on the engagement team being, or having recently been, an employee of the assurance client in a position to exert direct an ...

... engagement needs to be evaluated in reaching conclusions in the particular assurance engagement. Circumstances that may create a self-review threat include there being a person on the engagement team being, or having recently been, an employee of the assurance client in a position to exert direct an ...

SIGNATURE THEATRE COMPANY, INC. FINANCIAL

... Company, Inc. (a not-for-profit corporation) as of June 30, 2011, and the related statements of activities and cash flows for the year then ended. These financial statements are the responsibility of the Organization’s management. Our responsibility is to express an opinion on these financial statem ...

... Company, Inc. (a not-for-profit corporation) as of June 30, 2011, and the related statements of activities and cash flows for the year then ended. These financial statements are the responsibility of the Organization’s management. Our responsibility is to express an opinion on these financial statem ...

FRANKLIN ELECTRIC CO., INC. AUDIT COMMITTEE CHARTER

... member shall have past employment experience in finance or accounting, requisite professional certification in accounting, or any other comparable experience or background which results in the individual’s financial sophistication, such as serving or having served as a chief executive officer, chief ...

... member shall have past employment experience in finance or accounting, requisite professional certification in accounting, or any other comparable experience or background which results in the individual’s financial sophistication, such as serving or having served as a chief executive officer, chief ...

Substantive Tests of Transactions and Balances

... financial position accounts. There might be other sources of cash receipts and cash disbursements, but they would be substantiated by direct tests of balances of the statement of financial position accounts affected. Substantive tests of balances of statement of financial position accounts are gener ...

... financial position accounts. There might be other sources of cash receipts and cash disbursements, but they would be substantiated by direct tests of balances of the statement of financial position accounts affected. Substantive tests of balances of statement of financial position accounts are gener ...

CHAPTER 15 Understanding Accounting and Financial

... The statement of owners’ equity shows the components of the change in owners’ equity from the end of the prior year to the end of the current year. ...

... The statement of owners’ equity shows the components of the change in owners’ equity from the end of the prior year to the end of the current year. ...

Chapter 1 - Pearson Schools and FE Colleges

... In response, in 1971, the UK accounting bodies formed the Accounting Standards Committee (ASC) who issued many accounting standards known as Statements of Standard Accounting Practice (SSAPs). In 1990 the accountancy bodies replaced the ASC with the Accounting Standards Board (ASB) who issued furth ...

... In response, in 1971, the UK accounting bodies formed the Accounting Standards Committee (ASC) who issued many accounting standards known as Statements of Standard Accounting Practice (SSAPs). In 1990 the accountancy bodies replaced the ASC with the Accounting Standards Board (ASB) who issued furth ...

tides two rivers fund

... conformity with accounting principles generally accepted in the United States of America applicable to not-for-profit organizations. TTRF presents information regarding its net assets and activities based on the existence or absence of donor-imposed restrictions. Accordingly, net assets of TTRF and ...

... conformity with accounting principles generally accepted in the United States of America applicable to not-for-profit organizations. TTRF presents information regarding its net assets and activities based on the existence or absence of donor-imposed restrictions. Accordingly, net assets of TTRF and ...

Key Accounting Issues for Nonprofits

... unconditional promises to give, are recognized as revenues in the period received at their fair values. Contributions made, including unconditional promises to give, are recognized as expenses in the period made at their fair values. Conditional promises to give, whether received or made, are recogn ...

... unconditional promises to give, are recognized as revenues in the period received at their fair values. Contributions made, including unconditional promises to give, are recognized as expenses in the period made at their fair values. Conditional promises to give, whether received or made, are recogn ...

FREE Sample Here - Find the cheapest test bank for your

... 5. Which of the following statements is not true? a. A qualified opinion or an adverse opinion may bring into question the reliability of the financial statements. b. A disclaimer of opinion indicates that one should not look to the auditor's report as an indication of the reliability of the stateme ...

... 5. Which of the following statements is not true? a. A qualified opinion or an adverse opinion may bring into question the reliability of the financial statements. b. A disclaimer of opinion indicates that one should not look to the auditor's report as an indication of the reliability of the stateme ...

Competency area - Chartered Institute of Internal Auditors

... is applied in every audit assignment so that information is kept confidential, audit work is only undertaken where the auditor is competent to do so, conflicts of interest are disclosed, and the auditor acts objectively in all situations, ensuring that where ethical conflicts do occur they are discu ...

... is applied in every audit assignment so that information is kept confidential, audit work is only undertaken where the auditor is competent to do so, conflicts of interest are disclosed, and the auditor acts objectively in all situations, ensuring that where ethical conflicts do occur they are discu ...

Empirical evidence on liability caps and earnings management in

... third party. From a purely financial standpoint, liability risk can be seen as the expected value of damages to be paid. In the audit fee model by Simunic (1980) the expected damages are a function of audit effort5. The assumption is that the auditor responds to increased expected liability costs by ...

... third party. From a purely financial standpoint, liability risk can be seen as the expected value of damages to be paid. In the audit fee model by Simunic (1980) the expected damages are a function of audit effort5. The assumption is that the auditor responds to increased expected liability costs by ...