Chapter 5 The Time Value of Money

... company’s financial statements, not the company’s auditors. Auditors, such as Deloitte & Touche LLP (Deloitte), attest to whether or not the financial statements fairly represent the company’s financial position according to generally accepted accounting principles (GAAP). Companies reporting in the ...

... company’s financial statements, not the company’s auditors. Auditors, such as Deloitte & Touche LLP (Deloitte), attest to whether or not the financial statements fairly represent the company’s financial position according to generally accepted accounting principles (GAAP). Companies reporting in the ...

Audit Committee 18 September 2012

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...

NHC Financial Statements

... We have audited the accompanying financial statements of New Hope Clinic, Inc. (“New Hope”), a nonprofit organization, which comprise the statement of financial position as of December 31, 2013, and the related statements of activities, functional expenses, and cash flows, for the year then ended, a ...

... We have audited the accompanying financial statements of New Hope Clinic, Inc. (“New Hope”), a nonprofit organization, which comprise the statement of financial position as of December 31, 2013, and the related statements of activities, functional expenses, and cash flows, for the year then ended, a ...

Prior Year Adjustment (PYA)/Extraordinary Revenue

... Prior Year Adjustments (PYAs) are rare and shall only include adjustments meeting all of the following characteristics: (a) The value per occurrence must be in excess of $10,000 for CANEX and $ 2,000 for Base Fund/Messes etc; (b) They must be specifically identifiable with and directly related to th ...

... Prior Year Adjustments (PYAs) are rare and shall only include adjustments meeting all of the following characteristics: (a) The value per occurrence must be in excess of $10,000 for CANEX and $ 2,000 for Base Fund/Messes etc; (b) They must be specifically identifiable with and directly related to th ...

Financial Accounting and Accounting Standards

... Users and Uses of Financial Information Ethics In Financial Reporting Standards of conduct by which one’s actions are judged as right or wrong, honest or dishonest, fair or not fair, are Ethics. Recent financial scandals include: Enron, WorldCom, HealthSouth, AIG, and others. Congress passed Sarban ...

... Users and Uses of Financial Information Ethics In Financial Reporting Standards of conduct by which one’s actions are judged as right or wrong, honest or dishonest, fair or not fair, are Ethics. Recent financial scandals include: Enron, WorldCom, HealthSouth, AIG, and others. Congress passed Sarban ...

Amendments to Prospective Financial Statements

... When an entity presents historical general purpose financial statements for a period for which prospective financial statements have previously been presented, the comparative requirements in FRS-44 (PBE) New Zealand Additional Disclosures (paragraphs 11.1 and 11.2) are relevant. This Standard requi ...

... When an entity presents historical general purpose financial statements for a period for which prospective financial statements have previously been presented, the comparative requirements in FRS-44 (PBE) New Zealand Additional Disclosures (paragraphs 11.1 and 11.2) are relevant. This Standard requi ...

line management

... Ensure that aspects of work which may be subject to internal or external audit scrutiny are completed to a standard which will result in compliance. To work closely with the Finance Manager in using detailed costing models to enable support and academic staff to make effective decisions, including t ...

... Ensure that aspects of work which may be subject to internal or external audit scrutiny are completed to a standard which will result in compliance. To work closely with the Finance Manager in using detailed costing models to enable support and academic staff to make effective decisions, including t ...

Ch. 15 – Vocabulary Review accounting generally accepted

... profits of a business over a period of time. ...

... profits of a business over a period of time. ...

ISA 520 Analytical procedures

... The auditor may consider testing the operating effectiveness of controls, if any, over the entity’s preparation of information used by the auditor in performing substantive analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confid ...

... The auditor may consider testing the operating effectiveness of controls, if any, over the entity’s preparation of information used by the auditor in performing substantive analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confid ...

balance sheet or statement of financial position

... • Will cash flows be sufficient to service interest and principal payments to support the firm’s borrowing needs? • Does the company provide a good opportunity for employment, future advancement, and employee benefits? • How well does this company compete in its operating environment? • Is this firm ...

... • Will cash flows be sufficient to service interest and principal payments to support the firm’s borrowing needs? • Does the company provide a good opportunity for employment, future advancement, and employee benefits? • How well does this company compete in its operating environment? • Is this firm ...

Chapter 1

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. ...

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. ...

Hang Chi Holdings Limited 恒智控股有限公司

... and accounts, half-year report and quarterly reports, and to review significant financial reporting judgements contained in them. In reviewing these reports before submission to the Board, the Audit Committee shall focus particularly on: (a) any changes in accounting policies and practices; (b) ma ...

... and accounts, half-year report and quarterly reports, and to review significant financial reporting judgements contained in them. In reviewing these reports before submission to the Board, the Audit Committee shall focus particularly on: (a) any changes in accounting policies and practices; (b) ma ...

Financial Accounting and Accounting Standards

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. ...

... Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. ...

2011 Financials

... An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. I ...

... An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. I ...

Module 5 – Understanding the Basic Elements of School Board

... Specific Items – Financial Reporting (PS 2100 – PS 2700) – Sections dealing with financial statement items such as: PS 2100 Disclosure of accounting policies ...

... Specific Items – Financial Reporting (PS 2100 – PS 2700) – Sections dealing with financial statement items such as: PS 2100 Disclosure of accounting policies ...

Contrapartida

... detectar el fraude. Según señala el párrafo 3 de la Norma Internacional de Auditoría 240 - The auditor’s responsibilities relating to fraud in an audit of financial statements- “(…) Two types of intentional misstatements are relevant to the auditor – misstatements resulting from fraudulent financial ...

... detectar el fraude. Según señala el párrafo 3 de la Norma Internacional de Auditoría 240 - The auditor’s responsibilities relating to fraud in an audit of financial statements- “(…) Two types of intentional misstatements are relevant to the auditor – misstatements resulting from fraudulent financial ...

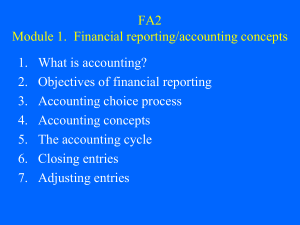

FA2 Module 1. Financial reporting/accounting concepts

... information about economic organizations (required by Canadian corporations legislation and securities commissions), but are only one of several, which include: •Other information in the annual report •Reports required by securities commissions •Reports/releases issued voluntarily ...

... information about economic organizations (required by Canadian corporations legislation and securities commissions), but are only one of several, which include: •Other information in the annual report •Reports required by securities commissions •Reports/releases issued voluntarily ...

LO 5 - Test Banks Shop

... Under current accounting standards, certain assets are valued at historical cost on all balance sheets until the company disposes of them since cost is objective, or verifiable by an outside observer Certain assets are valued on subsequent balance sheets at market value if the amount can be obje ...

... Under current accounting standards, certain assets are valued at historical cost on all balance sheets until the company disposes of them since cost is objective, or verifiable by an outside observer Certain assets are valued on subsequent balance sheets at market value if the amount can be obje ...

Define - kthsyr12acc

... change the way they calculate depreciation on their assets. Referring to an accounting principle, explain why the business should use the same method of calculating depreciation each year. IDENTIFY ...

... change the way they calculate depreciation on their assets. Referring to an accounting principle, explain why the business should use the same method of calculating depreciation each year. IDENTIFY ...

III Local audit of project accounts

... non-profit organisations" must be taken into consideration. If the contract partner's head office is outside Switzerland, the relevant national requirements or International Financial Reporting Standards IFRS must be applied. The object of the audit is the accounts. These are drawn up at the contrac ...

... non-profit organisations" must be taken into consideration. If the contract partner's head office is outside Switzerland, the relevant national requirements or International Financial Reporting Standards IFRS must be applied. The object of the audit is the accounts. These are drawn up at the contrac ...

Sample September / December 2015 answers

... Dali Co purchases many components from foreign suppliers and is therefore likely to be transacting and making payments in foreign currencies. According to IAS 21 The Effects of Changes in Foreign Exchange Rates, transactions should be initially recorded using the spot rate, and monetary items such a ...

... Dali Co purchases many components from foreign suppliers and is therefore likely to be transacting and making payments in foreign currencies. According to IAS 21 The Effects of Changes in Foreign Exchange Rates, transactions should be initially recorded using the spot rate, and monetary items such a ...

Auditors` Reports

... (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statemen ...

... (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statemen ...

Auditor`s Responsibility

... • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all known information bearing on fair pres ...

... • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all known information bearing on fair pres ...

Managing Financial Aspects of a Business

... What is accrual basis of accounting? What is cash basis? Effects of transactions and other events are recognised when they occur ( not when cash or cash equivalents received or paid) ...

... What is accrual basis of accounting? What is cash basis? Effects of transactions and other events are recognised when they occur ( not when cash or cash equivalents received or paid) ...

The Auditor - Whose Agent Is He Anyway

... Peasnell questions whether the auditing function would be a viable alternative for ‘organising and policing’ corporate disclosure. He describes how there are those who view external auditing as a largely useless legal imposition. He refers to Briston and Perks (1977), who suggest that both financial ...

... Peasnell questions whether the auditing function would be a viable alternative for ‘organising and policing’ corporate disclosure. He describes how there are those who view external auditing as a largely useless legal imposition. He refers to Briston and Perks (1977), who suggest that both financial ...